This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

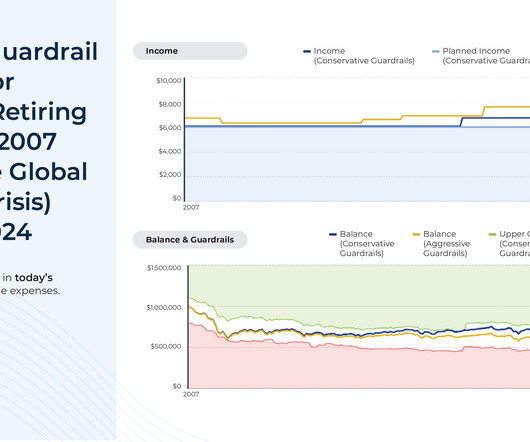

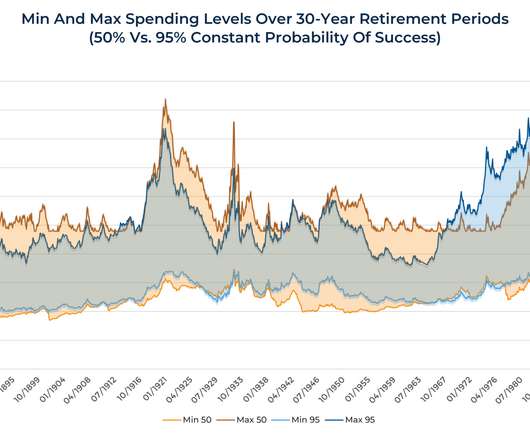

Monte Carlo simulations have become a central method of conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs. However, the results of these simulations generally don't account for potential adjustments that could be made along the way (e.g.,

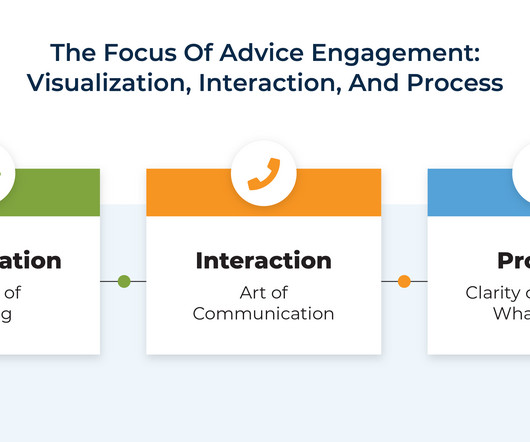

Financialplanning is both an art and a science. While an advisor needs technical financialplanning knowledge to create and implement plans for clients, soft skills that involve effective communication and relationship building are also crucial to both relate to prospects and clients and to understand their needs.

Financialplanning is both an art and a science. While an advisor needs technical financialplanning knowledge to create and implement plans for clients, soft skills that involve effective communication and relationship building are also crucial to both relate to prospects and clients and to understand their needs.

Just a few decades ago, giving financial advice was largely a manual process – printing lengthy financialplans, processing physical checks, and managing paper files. Many client concerns are deeply personal, requiring empathy, trust, and a nuanced understanding of complex emotional and financial situations.

Eric is the Chief Financial Advisor and Co-Owner of Econologics Financial Advisors, an independent RIA based in Largo, Florida, that generates more than $4M of revenue while working with nearly 300 client households.

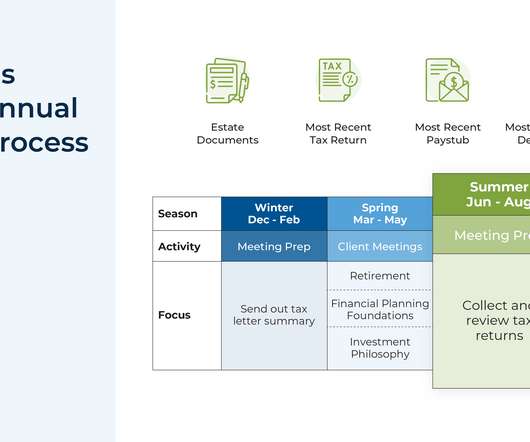

A common service model for many financial advisory firms is to schedule annual client meetings throughout the year where the advisor meets with each client in the month they started working with the firm, and conducts a comprehensive review of all planning topics for the client.

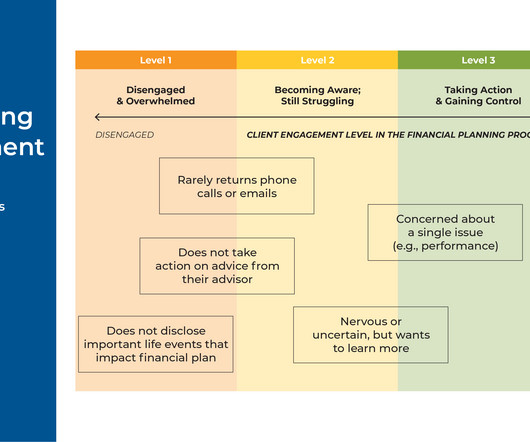

Financial advisors will sometimes talk about ‘bad’ clients who don’t act on the advice being provided. Advice Engagement is a framework that can help advisors address the challenge of motivating clients. by ensuring that clients receive information in a way that is useful for them); education (e.g.,

The increasing popularity of financialplanning has led to a growing awareness of how important managing finances and planning for the future can be. For most financial advisors today, a website is a critical tool that allows them to market their services and communicate their fees to potential clients.

Financialplans play an important role for both clients and advisors, as they not only help clients gain a clear perspective of their current financial position, but also provide advisors with a systematic way to organize their analyses and communicate their recommendations to the client.

When a financial advisory firm owner first starts their business, much of their time is spent on finding clients that they can serve. But as they (hopefully) onboard more clients and get busier with servicing those clients, they will also find that they eventually start to run short on time.

Monte Carlo simulations have become the dominant method for conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs.

Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. They also suggest how advisors with unsustainably low fees can shift their mindset, embrace their value, and realign their pricing to reflect both the tangible and intangible value they actually provide to clients.

For many financial advisors, financialplanning advice traditionally focuses on optimization: tax-efficient, continually rebalanced portfolios are often designed to maximize a client's wealth throughout retirement. Then, by assessing the bottom-line impact of reaching their goal on their financialplan (e.g.,

In recent years, politically charged topics have become the forefront of news and media, and with the rise of access to digitally distributed media, it has become commonplace for clients to have concerns about the possible impact of political events on their portfolios.

There's an old joke in the financialplanning industry that the ideal client is "anyone with a pulse". However, as their firms mature, advisors often notice a divide manifesting between newer clients paying higher fees and 'legacy clients' from the early days paying discounted rates.

For financial advisors, an ongoing client service model often means finding ways to keep clients engaged and progressing toward their goals outside of the 1 or 2 typical client review meetings each year.

So for advisors, it may be worth exploring whether there is anything to be learned from Ramsey's approach to financial advice – even if they may disagree on the details, advisors may find in Ramsey's advice a new and perhaps better way to communicate with (and motivate) clients. Read More.

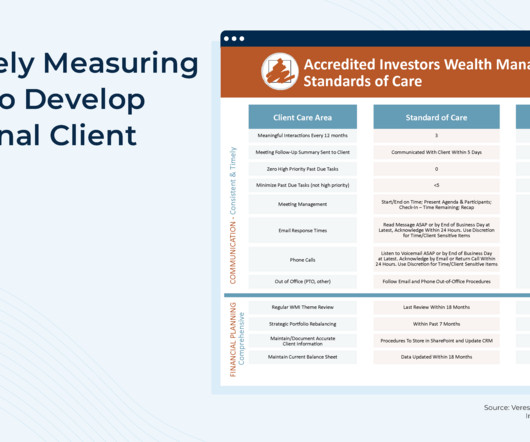

Most financial advisors strive to provide excellent client care and prioritize a systematic process to maintain regular communication with their clients both on a scheduled (e.g., Suddenly, the question of, "What does it mean to provide the best care for clients at this firm as a team?"

For many financial advisors, keeping an open line of communication with clients is a key component of building trust, understanding the client’s values, and developing a meaningful plan to help them reach their financial goals.

About a decade or so ago, one of the most pressing issues facing the financial advice industry was the threat of an imminent deluge of advisor retirements coupled with a paucity of succession plans to transition clients to the next generation.

As comprehensive financialplanning has become more widely adopted, many financial advisors have felt pressure to find new ways to differentiate themselves by demonstrating their unique value to clients.

Establishing successful client relationships as a financial advisor relies on good communication skills not just to present information persuasively and with confidence, but also to establish client rapport that allows meaningful and engaging relationships to be built.

For many financial advicers, helping long-time clients identify and progress toward their goals eventually transitions into conversations around the best ways to enjoy the fruits of their labor once they reach them. And by ensuring that their clients are equipped with (and know how to follow!) Read More.

Traditionally, financialplanning meetings have been held face-to-face in an advisor's office, and over the years, a body of research has emerged showing that how the advisor's office is laid out can have a significant impact on how clients perceive the advisor, their mood during the meeting, and even their resulting financialplanning decisions.

One of the benefits of owning a financialplanning business is an advisor’s ability to control their work schedule. But some advisors who choose to take more time off from their schedules might be concerned that prospects and clients will consider them to be less committed to serving their planning needs than other advisors.

After advisors do all of the work of bringing on a new client (Marketing! And while all may appear well on the surface – the client rarely contacts the advisor with problems but they show up for every annual meeting – they may actually be feeling quite disengaged with the financialplanning services being provided.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

Many clients seek financial advisors for their expertise and their abilities to guide them through financial decisions. However, for some clients, the ambiguity that inevitably arises from uncertain outcomes can be very distressing, especially when it comes to investments during volatile times.

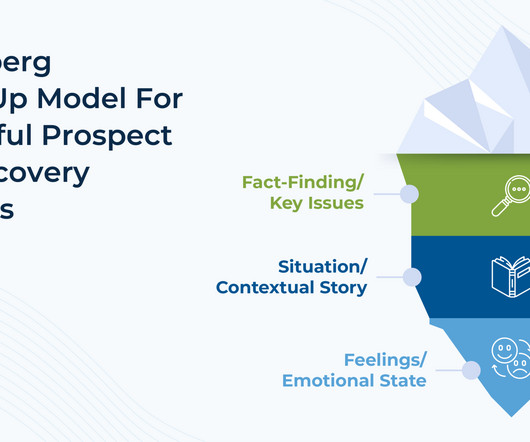

The need for financial professionals to ask prospects and clients questions has a long history in the industry. One of the best ways to accomplish that goal is not to ask better questions, but to also ask engaging follow-up questions that build trust and rapport with clients. as judgmental.

Financial advisors create value for clients not only by giving good advice, but also by ensuring that the advice they give is actually implemented. In this guest post, Derek Hagen, financial behavior expert and founder of financial therapy and life planning firm Money Health Solutions, explains why change (e.g.,

Welcome back to the 346th episode of the Financial Advisor Success Podcast ! Jim is the founder of MainStreet FinancialPlanning, an hourly, fee-only financialplanning firm, and also created Procrastination Junction, a coaching program for fee-only financial advisors looking to improve their sales skills.

Measuring a client's tolerance for risk is an essential (and required!) step when onboarding a new client, as making any sort of recommendation is impossible without first understanding how comfortable clients may be when their portfolios inevitably experience volatility. And while few (if any!)

Instead, advisors can take a more direct approach in introducing the next steps to becoming a client during a discovery meeting to keep the momentum going and potentially increase the chances that the prospect will become a client.

When it comes to politically charged discussions, financial advisors generally try to stay neutral and focus on providing clients with objective financial advice. This can make it increasingly difficult for the advisor to work with these clients.

Meaningful communication is crucial to building strong, durable relationships, and asking effective questions is an essential part of facilitating impactful conversations. More often, initial outreach from a prospect occurs because there's some urgent issue they need help with.

When financialplanningclients think about their future, they might imagine a relaxing retirement, world travel, or other pleasant experiences. And using this perspective, advisors can add value for clients by helping them prioritize their goals and explore whether their current behaviors match their desired outcomes.

Prospective clients often approach a financial advisor because they have a problem. Perhaps they are approaching retirement and do not know whether their current path is financially sustainable, or maybe they have a complicated equity compensation problem to sort through.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

The traditional way that most financialplanning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client'sfinancial strategy that was delivered either on a one-time basis or updated annually.

With inflation running hot, a potential recession looming, and both stock and bond markets seeing significant drops so far this year, there is no shortage of potential stressors for financialplanningclients. But to an angry client, these quick answers could feel dismissive or combative, potentially escalating the situation.

riabiz.com) Creative Planning is exploring its custody options. riabiz.com) Archive Intel has entered the adviser communications archiving space. blogs.cfainstitute.org) How life events affect retirement planning. investmentecosystem.com) Reflections on eight years of running a financialplanning practice.

While strategic advice is crucial, advisors also face the challenge of presenting the strategies to clients in context, explaining different financialplanning concepts, and showing clients how to implement these strategies (as well as pointing out any long-term consequences).

The practice of asking questions has always been an integral part of the financialplanning process. In the early days of the advicer industry, those questions almost exclusively dealt with facts around a client's or prospect's financial situation to determine (ultimately) what products the adviser should recommend.

And while there are many factors that help owners determine whether their firm is making enough money to profitably sustain itself, one common variable that can help them adjust their net revenue is the fee they charge to clients for financialplanning services. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content