This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And when conditions are this uncertain, it often makes sense to dive deeper into the factors driving the economy to better understand the risks – and opportunities – that clients may face. What's driving many of the economic conditions today are higher interest rates resulting from the Fed's efforts to fight inflation.

Yet, by taking a measured look at factors driving economic activity and influencing behavior, advisors can help clients face risks they can't control and (hopefully) position themselves to take advantage of opportunities as they develop. Meanwhile, a smorgasbord of potential risks threatens economic growth's "soft landing" narrative.

An assumed rate of return is needed, for example, to illustrate how much a client might need to save for retirement, how much savings they'll have when they do retire, and how long their savings will last after they stop working. The good news, however, is that there are ways for advisors to address the current issue of high U.S.

The sentiment is especially poignant when it comes to economic forecasting, as it's nearly impossible to get an accurate picture of the current state of the economy at any given moment. Moreover, historically extreme valuations in a small handful of mega-cap stocks that account for about 30% of the market weight in the S&P 500 (i.e.,

Also in industry news this week: The latest Social Security trustees report offered a slightly rosier picture for the health of the various Social Security trust funds thanks to improved economic conditions, though they warned that time is running out for legislators to take action to ensure the system will be able to pay out full benefits beyond the (..)

Finance Goldman Sachs ($GS) want to sell HNW clients a piece of a sports franchise. frontofficesports.com) Why seed stage valuations haven't dropped as much as you would think. politico.com) Why market economics doesn't necessarily work in health care. econofact.org) The economic schedule for the coming week.

In this guest post, Larry Swedroe, head of financial and economic research at Buckingham Strategic Wealth, discusses why many investors tend to fall prey to recency bias, and explains why global diversification – and keeping short- and long-term results in the right perspective – remains a prudent strategy. and global investments.

From there, we have several articles on practice management: A new report shows that RIA profitability and AUM soared in 2021, buoyed by a strong stock market and new client growth. How advisors can approach working with ultra-wealthy clients, who are increasingly focused on building dynastic wealth. Read More.

Eric is the Founder and CEO of Beyond Your Hammock, an independent RIA based in Boston, Massachusetts, that oversees $47 million in assets under management for more than 80 client households.

I have been fairly vocal that inflation has peaked , the Fed has already overtightened, and they run the risk of doing too much economic damage fighting a demon that has already been exorcised. But my job is not to give the Fed policy advice, it is instead to provide clients with insight and investment advice. 50% chance ).

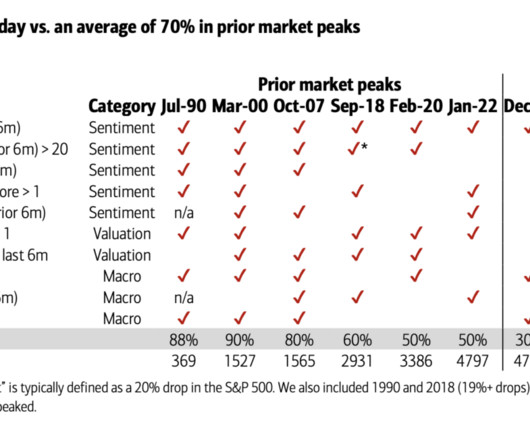

In response to repeated inquiries from BofA clients, Savita looked at numerous indicators that collectively suggest markets are topping. The table above shows the major market peaks going back to 1990.

despite beating earnings expectations, showing high valuation pressure. Economic Update: Retail Sales: Weaker than expected in January. Economic Surprise Index: Declined over the last 4-5 weeks from high levels. Opinions expressed by Zoe Financial are based on economic or market conditions at the time this material was written.

kitces.com) Daniel Crosby talks with Melina Palmer is founder and CEO of The Brainy Business, which provides behavioral economics consulting to businesses of all sizes from around the world. investmentnews.com) Advisers What is happening with RIA valuations? riabiz.com) DFA is a case study in being slow to recognize industry shifts.

Founding owners of financial advisory firms often spend much of their time focusing on the short-term aspects of running their business, from providing high-quality client service to pursuing client growth. metrics like revenue, profit, impact, clients, or team size), and a timeline for when the goals should be achieved.

My back-to-work morning train WFH reads: • The Problem with Valuation. I have an issue with valuation models in general. Because basically all the valuation metrics tell the same story—U.S. An aging population that values its free time set the stage for economic stagnation. But its success is hard to replicate. (

(vulture.com) The co-working business is diversifying its client base. wsj.com) How a seed investor approaches valuation discussions. axios.com) The economic schedule for the coming week. axios.com) How the Apple Watch saved the luxury watch industry. om.co) Twitter really hates paying its bills.

Market Valuations : Multiples are no longer considered cheap. Economic Updates: Payroll data: 227k new jobs added, above 220k expected. If earnings continue to grow steadily, inflation decelerates, and economic growth is maintained, the market could rally further with no immediate signs of a recession.

Here are 3 valuation scenarios to address that curiosity. Focus Financial Partners, the largest investor in the independent space, is being taken private at a $7B valuation. Prolific RIA acquirer CI Financial recently monetized a stake in their business at a $5B valuation. Those are some eye-popping numbers.

As a result, its often incumbent upon the retiring advisor to either accept a discounted valuation for the book and/or show a great deal of flexibility in how their next gen ultimately takes the reigns of the business. So, what can advisors do to ensure a successful client transition from one generation to the next? But is that fair?

Will the Federal Reserve continue to lower interest rates, supporting valuations? Zoe Financial is not an accounting firm- clients and prospective clients should consult with their tax professional regarding their specific tax situation. Actual economic or market events may turn out differently than anticipated.

Fueled by optimism, the scent of economic recovery was in the air. Read more : Up the Stairs, Down the Shaft: The Tale of a Tumbling Market Economic indicators were trying to give us the thumbs up, and consumer confidence was inching higher. As we’ve written before, all the economic experts and doom and gloom crowd got it wrong.

Estates Estate Planning in this Economic Climate Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Between inflation, increasing interest rates, federal changes to monetary policies, and global conflict, many factors are putting a strain on the current economic situation. Create a Trust .

A bachelor’s in economics from Northwestern and then an MBA from University of Chicago. And so I kind of leveraged that when I went to Morningstar because they’re very focused on quality, the whole concept of economic moats, but also about buying companies when they’re trading at a discount to intrinsic value.

The firm that he’s built is one of those very quiet, very successful entities that without a whole lot of media coverage, without a whole lot of fanfare, just amassed an enormous amount of capital because they’ve done so well for their clients over time. John was one of our managers that we had, you know, our clients invest in.

What I mean by that is that we’re currently navigating the economic bust portion of the cycle where inflation is a falling risk and credit deflation risk arises, in large part, because the Fed has reacted so quickly to bring inflation in. But to understand the bust you really need to understand the boom.

Some recent softening in economic data, coupled with signals from the bond market, may be indicating that Fed policymakers’ concerted inflation fight may be closer to the end than the beginning. We should also have slowing corporate earnings growth and greater economic uncertainty to contend with, some formidable seas to navigate.

The rule of thumb is two quarters of negative GDP defines a recession, but the official definition by the National Bureau of Economic Research is broader than that. Market-based interest rates those not controlled by the Fed—have come down quite a bit, supporting stock valuations. economy contracted for the second straight quarter.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Since 1995, there are four rather distinct periods during which forward earnings estimates for the S&P 500 Index declined, tied to a specific event and/or economic downturn. by year-end.

Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. The good news is there’s nothing in the economic data that suggests we’re on the verge of a labor-market-induced inflation surge. Following the huge 11.2% This newsletter was written and produced by CWM, LLC.

Your Client List As a financial services professional, you’ve probably spent years building up your book of business. This client list plays a significant role in the value of your business. Brand Identity Have you been working with clients as an individual financial professional?

Many of these businesses, and many of the things that move on rails are just captive volumes that can’t economically move via truck or via plane. Note: Clients of Fortune Financial Advisors, LLC own shares of Union Pacific, CSX, and NSC.

Barry Ritholtz : So let’s break that into two halves, starting with valuation. Explain why P/E isn’t the best way to measure valuation. Jim O’Shaugnessy : Momentum is really interesting because academics hate it because there is underlying economic reason why it should make sense – but it does.

Inflation is currently at 40 year highs with increasing signs of slowing economic growth. We’re currently seeing one of the largest disparities in valuations between growth and value stocks which in our opinion presents a very appealing opportunity for dividend seeking investors.

But after many years of economic recovery, we finally have reached a point where defensive allocations once again provide a reasonable yield. But beyond the economic cycle’s age, several factors suggest that a more defensive mindset is worth considering: Valuations are elevated. has been steady and consistent.

But after many years of economic recovery, we finally have reached a point where defensive allocations once again provide a reasonable yield. We still believe that equities offer healthy opportunity, and the fact that the current economic expansion is simply “old” has never been a sufficient reason for us to lose confidence in it.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S. equity exposure.

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? Or is it a convenient way to measure the relative economic value created between our starting and end points? What does this actually mean?

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? Or is it a convenient way to measure the relative economic value created between our starting and end points? What does this actually mean?

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Over the long term, that stance has paid off. is not particularly notable. stocks since the middle of 2004.

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Over the long term, that stance has paid off. is not particularly notable. stocks since the middle of 2004.

In many clients’ portfolios we have eliminated our overweight position in U.S. The economic expansion is weak and inflation is still below the central bank’s 2% target. equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations.

All the sectors went up with major sectoral growth seen in auto (up 22%), realty (up 33%), and consumer durables (up 13%) on the back of an improving economic outlook. The recent rally in the market has made the valuations more expensive compared to historical standards. Valuations across all sectors do not offer any margin of safety.

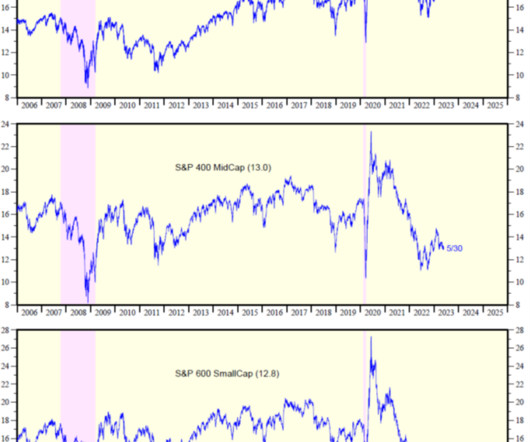

First of all, smaller companies are more cyclically sensitive to an economic slowdown, and do not have the ability to cut costs to the same extent as the behemoth companies. The majority of stocks have factored in a slowdown (or mild recession) and this is why valuations for small-cap and mid-cap stocks are near multi-decade lows (12.8x

An excellent case study for this idea is Japan, a country that many investors wrote off long ago—but one that managers have successfully mined for return opportunities during the country’s extended economic struggles. Unbridled optimism ushered in an economic bubble of historic proportions. valuation). in local terms and 1.6%

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content