This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Financialadvicers often market their comprehensive financial services as a way to differentiate themselves from other advisory firms and to stand out in the broader landscape of financialadvice. While advisors may make educated guesses about client preferences, this approach has its limits.

is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree. "How much can I spend in retirement?"

How much to charge for financialadvice is rarely a decision made lightly. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning.

I help clients in retirement by doing X, Y, and Z."). However, not all prospects have immediate financial concerns. While these individuals may genuinely be interested in financialadvice, they might also feel ambivalent about the timing, relevance, or ultimate value of working with an advisor. Read More.

Which suggests firms that can meet clients' evolving needs as they advance up the wealth spectrum (e.g., Which suggests firms that can meet clients' evolving needs as they advance up the wealth spectrum (e.g.,

Which could prove to be a boon for the financialadvice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

The possibilities at the intersection of AI and financialadvice are exciting – faster processes, better connections, less time on ‘busy work’ – but also come with uncertainty about the future of the field. What might the field of financialadvice even look like in 10 years? Read More.

Fran is the CEO of Toler Financial Group, an RIA based in Silver Spring, Maryland, that oversees nearly $200 million in assets under management for 280 client households. My guest on today's podcast is Fran Toler.

New financial advisors often start with below-market fees – sometimes to build confidence that prospects will actually pay, other times to attract clients quickly and establish a base. And while new clients often come in at higher fees, early clients may still be paying well below the firm's current rates.

For instance, the financialadvice industry has seen many changes to regulations (for both advisors and their clients), advisor business models, and the advisor technology landscape. The changing patterns in how financialadvice is delivered can be compared to the similar trends seen in the evolution of medicine.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that CFP Board CEO Kevin Keller this week announced his plans to retire and step down from his position at the end of April next year.

Podcasts Daniel Crosby talks with Michael Kitces about automation and the future of financialadvice. kitces.com) Brendan Frazier talks with Samantha Lamas and Danielle Labotka about why clients hire and fire their financial advisers. wsj.com) Advisers How to speak to clients in a way that they understand.

Financial advisors have a fiduciary obligation to act in their clients' best interests, and at the same time are prohibited by state and SEC rules from making misleading statements or omissions about their advisory business.

downtownjoshbrown.com) How indexing has made for a better financialadvice industry. morningstar.com) The biz Creative Planning was able to retain some 60% of the United Capital assets. riabiz.com) XY Planning Network is launching a new in-house RIA, XYPN Sapphire. citywire.com) A lot of RIAs are in that in-between stage.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the "Social Security Fairness Act" was signed into law this week, eliminating the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) provisions, which previously reduced the Social Security benefits (..)

The requirements to run a successful, growing advisory firm are often less about doing the technical work with clients and more about marketing value to get prospects in the door in the first place. comprehensive, planning-centric, fee-based advisors) versus 'bad guy' (e.g.,

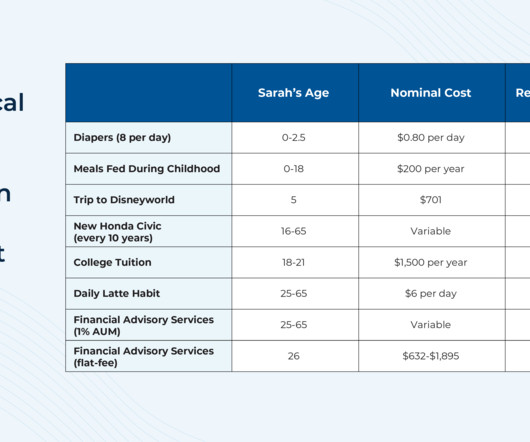

While the financialadvice industry has transformed in many ways over the past several decades, one aspect that has remained relatively constant is the use of the Assets Under Management (AUM) fee model as a common way for many advisors to get paid. So too does the impact of the infamous daily latte.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

One of the main goals of financial advisors who market themselves is to build a foundation of trust with their prospective clients so that they feel comfortable in discussing often-sensitive financial topics and ultimately acting on the advisor's recommendations.

As financialplanning has evolved over the years, better tools have become available to help advisors maximize their impact with more clients by increasing their efficiency. robo-advisors) might someday replace human advisors, there are still many elements of financialplanning that benefit from engagement with a human advisor.

When it comes to politically charged discussions, financial advisors generally try to stay neutral and focus on providing clients with objective financialadvice. This can make it increasingly difficult for the advisor to work with these clients.

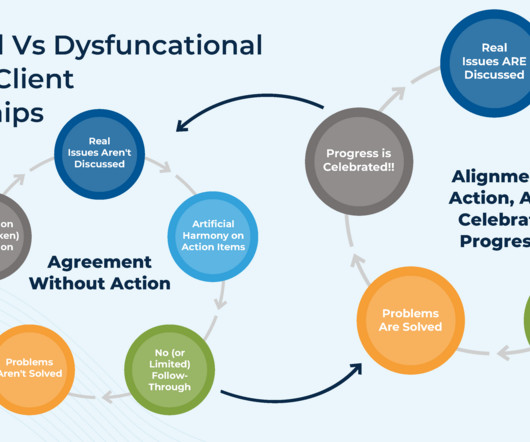

In the modern era of financialadvice, the advicer/client relationship is tightly centered on trust. Then, because the client isn't "bought in" to the recommendations, they simply don't act on what the advisor recommends.

It's not news that financialadvice will increasingly be grounded in psychology and therapy—but how an advisor builds a business around those client demands is still evolving, according to speakers at the Future Proof wealth festival.

Brenda is a financial planner with Objective Financial Partners, an advice-only advisory firm based in Ontario, Canada, that works with clients on project-based financialplans, and also offers outsourced paraplanning to other Canadian advisory firms. My guest on today's podcast is Brenda Hiscock.

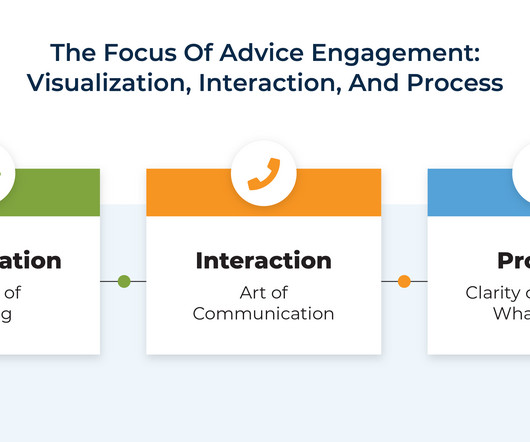

The traditional way that most financialplanning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client'sfinancial strategy that was delivered either on a one-time basis or updated annually.

There are many financial advisors who take issue with the financialadvice offered by popular personal finance personalities such as Dave Ramsey. Though many potentially valid criticisms of this process tend to concern technical details (e.g., Read More.

Podcasts Christine Benz and Amy Arnott talk with Preston Cherry, author of a new book "Wealth in the Key of Life: Finding Your Financial Harmony." morningstar.com) Carl Richards and Michael Kitces on whether a client should take time before coming on as a client. How to do better for clients.

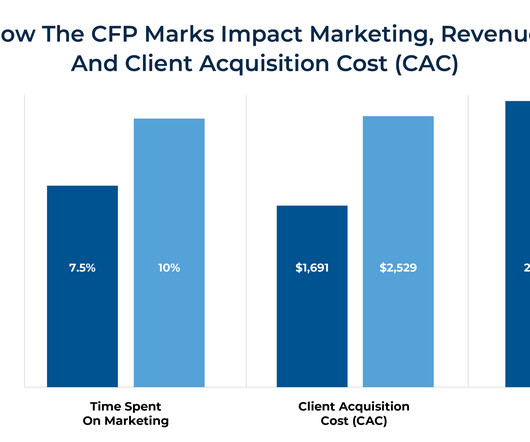

According to the 2022 Kitces Research study, “How Financial Planners Actually Market Their Services”, advisors without the CFP marks typically spend more of their time on marketing activities relative to CFP practitioners (allowing them to spend more time on higher-value tasks).

For many financialadvicers, helping long-time clients identify and progress toward their goals eventually transitions into conversations around the best ways to enjoy the fruits of their labor once they reach them. And by ensuring that their clients are equipped with (and know how to follow!) Read More.

Andrew is the founder of Tenpath Financial Group and Planning Across the Spectrum, a hybrid firm based in Farmington, Connecticut that oversees $100 million in assets under management for 100 client households.

riabiz.com) Creative Planning is exploring its custody options. blogs.cfainstitute.org) How life events affect retirement planning. papers.ssrn.com) Advisers There is an tension inherent in the practice of financialadvice. papers.ssrn.com) Advisers There is an tension inherent in the practice of financialadvice.

Initial outreach to a financialadvicer rarely (if ever) results from a prospective client waking up in the middle of the night in a cold sweat because they just figured out that they're in desperate need of a comprehensive financialplan.

With another strong year in the markets, most advisory firms are near or at record highs for their revenue, their numbers of clients, and the headcounts of their teams. Which is surprising to some, given that a decade ago, the emergence of so-called "robo-advisors" was supposed to displace human financial advisors and compress advisory fees.

Podcasts Michael Kitces talks financial wellness with Zack Hubbard. Zack is the Director of FinancialPlanning and Participant Engagement of Greenspring Advisors. youtube.com) Brendan Frazier talks with Michael Kitces about mastering the human side of financialadvice.

frazerrice.com) Creative Planning TPG just bought a big stake in Creative Planning. thinkadvisor.com) Creative Planning shows 'institutional investors are placing a premium on integrated wealth management businesses relative to aggregators.' citywire.com) How to help clients understand the state of Social Security.

Welcome back to the 346th episode of the Financial Advisor Success Podcast ! Jim is the founder of MainStreet FinancialPlanning, an hourly, fee-only financialplanning firm, and also created Procrastination Junction, a coaching program for fee-only financial advisors looking to improve their sales skills.

While some RIA owners might be tempted to prioritize moving quickly to the more enjoyable work of providing financialadvice, neglecting to thoughtfully draft and update an operating agreement can lead to mismatched expectations, legal risks, and costly disputes.

While some RIA owners might be tempted to prioritize moving quickly to the more enjoyable work of providing financialadvice, neglecting to thoughtfully draft and update an operating agreement can lead to mismatched expectations, legal risks, and costly disputes.

Niching offers several advantages, allowing advisors to be more specific in their marketing, more targeted in their prospecting calls, and more efficient in their processes (since clients within a similar niche are likely to have similar problems, especially in niches of profession).

Podcasts Brendan Frazier talks with Jake Northrup of Experience Your Wealth about how he infuses the human side to help clients live their ideal life. podcasts.apple.com) Michael Kitces talks with Sarah-Catherine Gutierrez, founder of Aptus Financial, about operating as a flat-fee advice-only firm.

(riabiz.com) Why women are still struggling to make progress in the world of financialadvice. riaintel.com) HNW clients want additional services. city-journal.org) Delayed Social Security claiming requires an explicit bridge plan. kitces.com) Client's lives are growing more complex. It hasn't happened.

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-only financialplanning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet FinancialPlanning.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the shift in financialadvice from pure investment management to comprehensive financialplanning continues, with more individuals becoming CFP professionals than CFAs in the past few years as consumers increasing the diversity (..)

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content