This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While state and Federal regulations clearly outline recordkeeping requirements for areas like financials, advertisements, and trading records, there is a notable gap when it comes to documenting the delivery of services – especially financialplanning services – necessary to justify the fees charged for those services.

Over the past decade, a growing number of advisors have expanded into offering comprehensive financialplanning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financialplanning.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financialplanning (as well as consulting with over 15,000 clients on student loan debt).

Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. They also suggest how advisors with unsustainably low fees can shift their mindset, embrace their value, and realign their pricing to reflect both the tangible and intangible value they actually provide to clients.

The former TDAI and Altruist executive has been in stealth mode building Wing, a digital financialplanning app meant to help next-gen clients build personalized, goals-based plans, and advisors capture money in motion.

There's an old joke in the financialplanning industry that the ideal client is "anyone with a pulse". However, as their firms mature, advisors often notice a divide manifesting between newer clients paying higher fees and 'legacy clients' from the early days paying discounted rates.

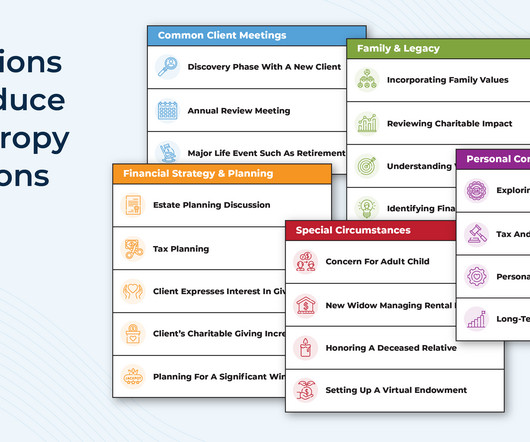

Yet, despite the important role that charitable giving can play, studies show that many advisors hesitate to bring up the topic with clients. Advisors may worry about overstepping boundaries or feel uncertain about a client's interest in philanthropy. These statements often stem from clients' life stories and core values.,

Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. My guest on today's podcast is Seth Scott.

Anjali is the Founder of FIT Advisors, an RIA based in Torrance, California (but works virtually with clients nationwide) and oversees $65 million in assets under management for 45 client households.

Sebastian is the President of Guerra Wealth Advisors, a hybrid advisory firm based in Miami, Florida, with nearly $15M of revenue and almost 60 team members, supporting over 1,700 client households.

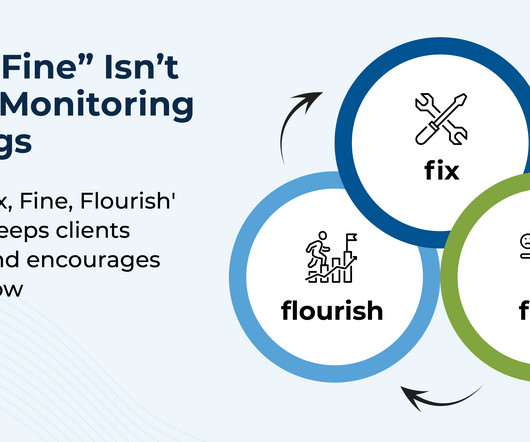

When a client first begins working with an advisor, the relationship is often marked with a flurry of onboarding tasks, immediate issues to resolve, and long-term planning goals to establish. And as clients come into monitoring meetings, they may increasingly describe their situation as "fine", with no pressing issues to address.

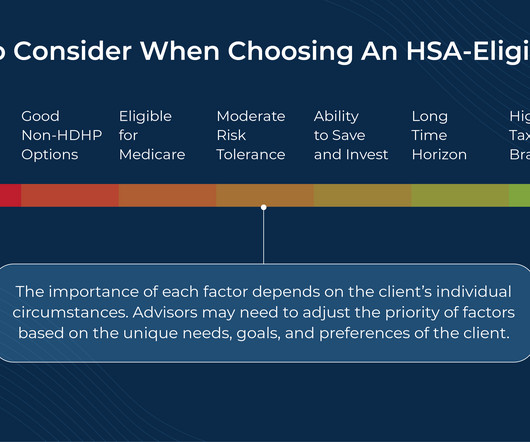

Health Savings Accounts (HSAs) have become an increasingly popular tool for financial advisors and their clients due in part to the 'triple tax savings' they offer: tax-deductible contributions, tax-free growth, and non-taxable distributions for qualifying expenses. Read More.

I help clients in retirement by doing X, Y, and Z."). However, not all prospects have immediate financial concerns. While these individuals may genuinely be interested in financial advice, they might also feel ambivalent about the timing, relevance, or ultimate value of working with an advisor.

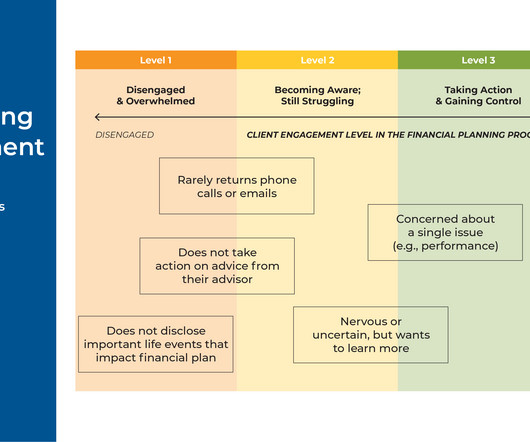

Financial advisors will sometimes talk about ‘bad’ clients who don’t act on the advice being provided. Advice Engagement is a framework that can help advisors address the challenge of motivating clients. by ensuring that clients receive information in a way that is useful for them); education (e.g.,

Cristina is the CEO of Mana Financial Life Design, an RIA based in Los Angeles, California (but works virtually with clients nationwide), that oversees approximately $70 million in assets under management for 119 client households.

podcasts.apple.com) The biz Fidelity's move to sweep client cash into FCASH, making more work for RIAs. riabiz.com) Morgan Stanley's ($MS) wealth management division apparently prioritized assets over vetting clients. riabiz.com) Why wealth managers need to do more to support client charitable giving. thinkadvisor.com)

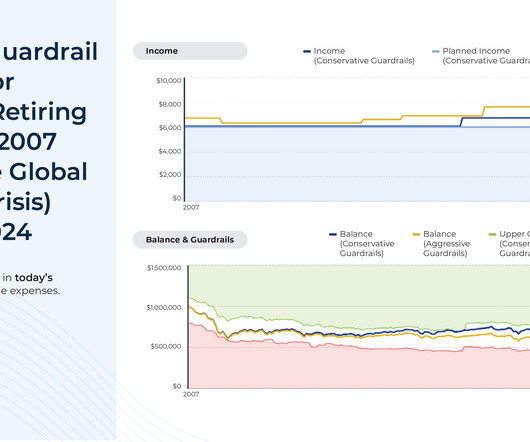

is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree. "How much can I spend in retirement?"

Eric is the Chief Financial Advisor and Co-Owner of Econologics Financial Advisors, an independent RIA based in Largo, Florida, that generates more than $4M of revenue while working with nearly 300 client households.

citywire.com) What's behind the surge in client churn at RIAs? riabiz.com) Risk tolerance Determining a client's risk tolerance is more complicated than having them fill out a questionnaire. advisorperspectives.com) Advisers A plan for onboarding client service associates. signaturefd-3437664.hs-sites.com)

In the early days of financialplanning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Financialplans play an important role for both clients and advisors, as they not only help clients gain a clear perspective of their current financial position, but also provide advisors with a systematic way to organize their analyses and communicate their recommendations to the client.

The increasing popularity of financialplanning has led to a growing awareness of how important managing finances and planning for the future can be. For most financial advisors today, a website is a critical tool that allows them to market their services and communicate their fees to potential clients.

When a financial advisory firm owner first starts their business, much of their time is spent on finding clients that they can serve. But as they (hopefully) onboard more clients and get busier with servicing those clients, they will also find that they eventually start to run short on time.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a report from Cerulli Associates found that, amidst an industry-wide trend towards comprehensive financialplanning and away from pure transaction-based investment management, asset-based fees currently represent 72.4%

Many financial advisors take pride in the comprehensive nature of the advice they provide to clients and use the variety of services offered as a point of differentiation between themselves and other types of advisors. in the form of an associate planner or paraplanner) or engaging outsourced planning service providers.

Together, these proposed changes (which are currently open for public comment) suggest CFP Board is seeking to ensure that those with the marks not only have sufficient education and experience upon receiving them, but also maintain and sharpen their skills over the course of their careers.

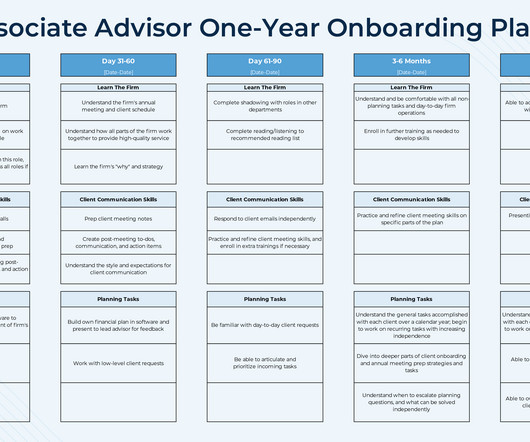

For smaller firms – especially those with little to no experience onboarding new advisors – creating a well-paced financialplan can feel daunting. First, clarity: both the advisor and manager should be able to clearly define the core financialplanning skills that a new hire is expected to develop in their first year.

Mann, MBA, CFP I find that so many of my clients, regardless of income, have no idea how much money they are saving. Early in my career, this created quite the challenge in developing a proper plan. First, I would ask clients how much they were saving each year for retirement. Then I would present the plan to the client.

By Antoinette Tuscano, MDRT senior content specialist You can be an outstanding financial advisor; however, youre still out of business without clients. In these top videos posted on MDRTs YouTube channel in 2024, learn how MDRT members communicate and work with clients.

After advisors do all of the work of bringing on a new client (Marketing! And while all may appear well on the surface – the client rarely contacts the advisor with problems but they show up for every annual meeting – they may actually be feeling quite disengaged with the financialplanning services being provided.

Danielle is the owner of Wealth By Design, a hybrid advisory firm based in Glenwood Springs, Colorado, that oversees about $35 million in assets under advisement for 35 client households.

To sustain firm growth, financial advisors often face a dilemma: to focus on what originally drew them to the profession – like financialplanning – they often must first do an extensive amount of business development. From there, advisors may need to consider whom to outsource to.

Since the emergence of Artificial Intelligence (AI) in the mainstream technological landscape, conversations about which areas of the financialplanning industry would be most likely impacted by AI have proliferated. ” – can guide ChatGPT toward more tailored results. Read More.

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households.

Financial advisors create value for clients not only by giving good advice, but also by ensuring that the advice they give is actually implemented. In this guest post, Derek Hagen, financial behavior expert and founder of financial therapy and life planning firm Money Health Solutions, explains why change (e.g.,

Measuring a client's tolerance for risk is an essential (and required!) step when onboarding a new client, as making any sort of recommendation is impossible without first understanding how comfortable clients may be when their portfolios inevitably experience volatility. And while few (if any!)

For many financial advisors, financialplanning advice traditionally focuses on optimization: tax-efficient, continually rebalanced portfolios are often designed to maximize a client's wealth throughout retirement. Then, by assessing the bottom-line impact of reaching their goal on their financialplan (e.g.,

One of the key steps in the financialplanning process is presenting the plan to the client, which has traditionally been done as part of a single 'plan presentation' meeting that takes place once the advisor has gathered and analyzed all of the client's data.

Monte Carlo simulations have become a central method of conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs. However, the results of these simulations generally don't account for potential adjustments that could be made along the way (e.g.,

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financialplanning to add-ons like tax preparation).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content