This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

"How much can I spend in retirement?" is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirementplan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree.

These services may range from 'standard' offerings like retirementplanning to less traditional areas like credit card consulting. In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients.

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. My guest on today's podcast is Seth Scott.

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that at a time when brokerage firms' cash sweep programs come under increased scrutiny (and as the Federal Reserve has cut interest rates), Charles Schwab (the largest RIA custodian) continues to slash sweep rates for client (..)

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirementplanning.

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that according to a recent study by DeVoe & Company, only 42% of RIAs surveyed have written succession plans and either have begun to implement them or have already done so.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that CFP Board CEO Kevin Keller this week announced his plans to retire and step down from his position at the end of April next year.

Also in industry news this week: While RIA M&A deal flow hit record levels in 2024 (both in terms of volume and the speed of completing them), firm valuations saw relatively modest gains In its latest annual regulatory oversight report, FINRA joined the SEC in flagging the potential risks to firm and client data from the use of third-party vendors (..)

(kitces.com) Estate planning Estate plans are a big lift for everyone, including advisers themselves. kindnessfp.com) Why clients need to organize their digital assets for estate planning purposes. riabiz.com) This money manager's ETF business was built on entertaining clients. abnormalreturns.com)

A new WMIQ study on retirementplanning, conducted in collaboration with annuity provider Midland Advisory, found more than 3/4 of potential clients feel it’s important for advisors to be fiduciaries and nearly 2/3 prioritize retirement expertise.

While it may take a while for the adjustments to take place, advisors can still help their clientsplan for the effect of WEP and GPO's repeal by estimating how much the client will be receiving in Social Security benefits once the new law is implemented. will be top of mind for clients affected by the WEP and GPO.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. Talk to us today.

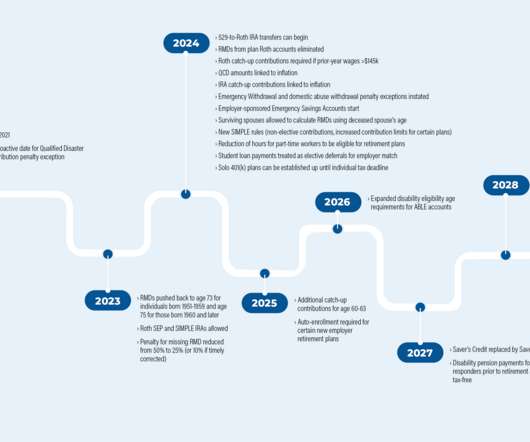

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 Read More.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 Read More.

Vestwell conducted the fourth-annual “Retirement Trends Report” in fall 2022 and received responses from almost 1,300 savers, 500 financial advisors and 250 small businesses.

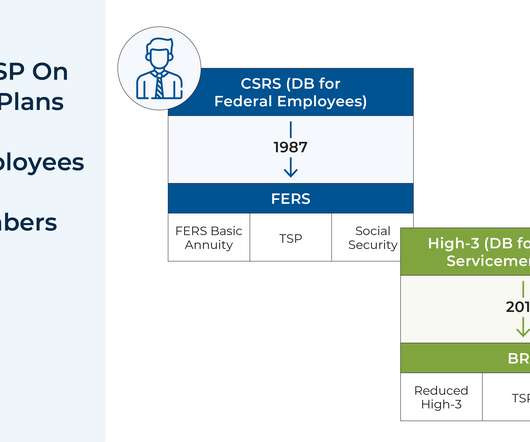

Seasoned financial advisors have likely worked with clients with a wide variety of workplace retirement accounts, which can vary in terms of their investment offerings, fees, and other characteristics. But given that the U.S. But given that the U.S. While many features of the TSP (e.g., While many features of the TSP (e.g.,

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

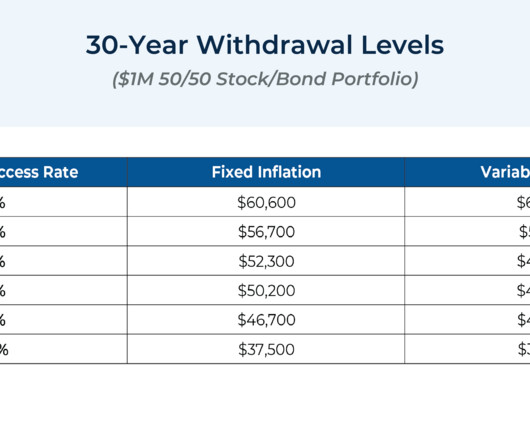

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

However, when these aspirations are delayed or blocked by senior advisory firm partners who choose to delay their retirementplans, it can leave younger advisors frustrated and in a place of uncertainty about their futures with their firm.

morningstar.com) Carl Richards and Michael Kitces on whether a client should take time before coming on as a client. How to do better for clients. kitces.com) Working with UNHW clients is more complex. citywire.com) Your (potential) clients are looking online for financial advice.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

riabiz.com) Creative Planning is exploring its custody options. blogs.cfainstitute.org) How life events affect retirementplanning. investmentecosystem.com) Reflections on eight years of running a financial planning practice. wealthmanagement.com) Why 4% retirement withdrawal rates are still a thing.

Collaborations with Salesforce, PureFacts and Pontera will add retirementplanning, billing and client onboarding capabilities to the multi-custodial platform announced this week at INSITE.

Retirementplanning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA.

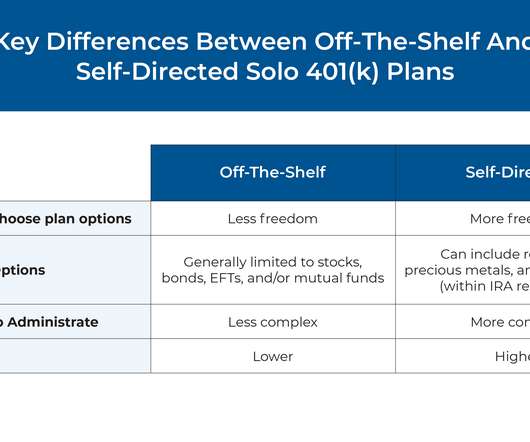

Among the several different types of retirementplans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. Read More.

Liz is the co-owner of Pleasant Wealth, a hybrid advisory firm based in Canton, Ohio that oversees $146 million in assets under management for 522 client households.

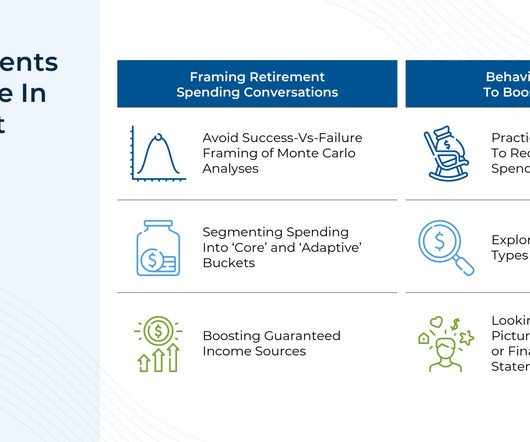

Retirement is often framed as one's "golden years", a time to enjoy the fruits of several decades of hard work. And for many retirees who have planned accordingly, this transition is not a problem as they might spend generously on travel, hobbies, or other pursuits. On the behavioral side, clients could 'practice' retirement (e.g.,

He did this research on behalf of Equitable to look at how to improve the efficient frontier, enhance risk-adjusted returns and help advisors – and their clients – make the most of their assets through their retirement.

investmentnews.com) RetirementRetirementplanning is challenging because we simply don't know how long someone will live. kitces.com) Retirement spending is by its nature dynamic. thinkadvisor.com) Advisers Four things clients value in advisers. morningstar.com) These clients have more than one adviser.

One of the key elements in retirement income planning is understanding the role of Social Security. Many clients may view Social Security simply as an income source, but savvy advisors recognize its potential as a unique asset that can significantly shape a well-rounded retirement strategy.

Enjoy the current installment of "Weekend Reading For Financial Planners"– this week's edition kicks off with the news that a recent analysis from Morningstar suggests that the Department of Labor's (DoL's) new Retirement Security Rule (aka Fiduciary Rule 2.0)

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content