This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

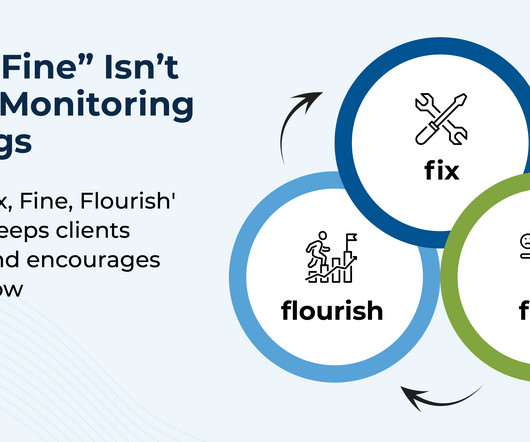

When a client first begins working with an advisor, the relationship is often marked with a flurry of onboarding tasks, immediate issues to resolve, and long-term planning goals to establish. And as clients come into monitoring meetings, they may increasingly describe their situation as "fine", with no pressing issues to address.

One of the key steps in the financial planning process is presenting the plan to the client, which has traditionally been done as part of a single 'plan presentation' meeting that takes place once the advisor has gathered and analyzed all of the client's data.

Advisors must decide how to present themselves, respond to questions, explain complex issues in an engaging way, and propose and explain their long-term proposition. The introductory meeting is a high-stakes moment for both advisors and prospects, often nerve-wracking for both sides. Read More.

The typical prospecting process involves multiple meetings, and a fairly common response for advisors to hear after giving their 'pitch' is that the client needs some extra time to think about it. I can only onboard 3 clients in a given quarter. Read More.

Over the past decade, a growing number of advisors have expanded into offering comprehensive financial planning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Today, the industry has evolved further, with a growing emphasis on aligning financial decisions with clients' personal priorities and life goals.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that while overall financial advisor headcount remains relatively flat, the RIA channel continues to gain share in terms of both headcount (as brokers break away to start their own independent firms and aspiring advisors seek (..)

Cristina is the CEO of Mana Financial Life Design, an RIA based in Los Angeles, California (but works virtually with clients nationwide), that oversees approximately $70 million in assets under management for 119 client households. Read More.

Mann, MBA, CFP I find that so many of my clients, regardless of income, have no idea how much money they are saving. First, I would ask clients how much they were saving each year for retirement. Then I would present the plan to the client. By Jennifer P.

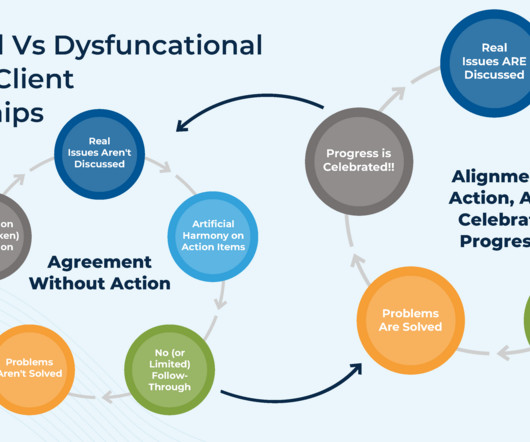

In the modern era of financial advice, the advicer/client relationship is tightly centered on trust. Then, because the client isn't "bought in" to the recommendations, they simply don't act on what the advisor recommends.

A significant challenge for financial advisors is translating complex financial concepts into terms clients can easily digest. For many, presentations serve as an effective medium for closing the gap between what advisors know and what clients can understand.

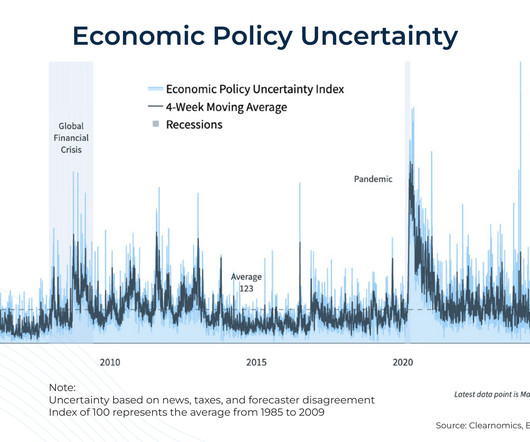

Recent swings have been driven by economic policy shifts, persistent inflation concerns, and geopolitical uncertainty – all of which may unnerve even the steadiest of clients. During turbulent periods like these, advisors play a critical role in helping clients maintain perspective and stay grounded.

When financial planning clients think about their future, they might imagine a relaxing retirement, world travel, or other pleasant experiences. And using this perspective, advisors can add value for clients by helping them prioritize their goals and explore whether their current behaviors match their desired outcomes.

Establishing successful client relationships as a financial advisor relies on good communication skills not just to present information persuasively and with confidence, but also to establish client rapport that allows meaningful and engaging relationships to be built.

Danielle is the owner of Wealth By Design, a hybrid advisory firm based in Glenwood Springs, Colorado, that oversees about $35 million in assets under advisement for 35 client households.

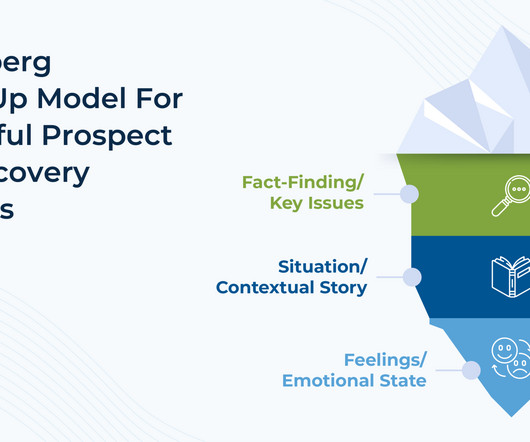

The need for financial professionals to ask prospects and clients questions has a long history in the industry. One of the best ways to accomplish that goal is not to ask better questions, but to also ask engaging follow-up questions that build trust and rapport with clients. as judgmental.

In recent years, politically charged topics have become the forefront of news and media, and with the rise of access to digitally distributed media, it has become commonplace for clients to have concerns about the possible impact of political events on their portfolios.

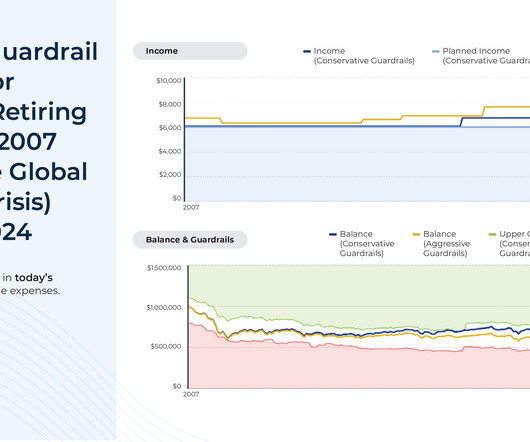

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. the Great Depression or the Global Financial Crisis), showing clients when and to what degree spending cuts would have been necessary.

When it comes to helping clients clarify their most important financial planning goals and priorities, many advisors may find it difficult to facilitate the insightful conversations necessary to guide clients through an exploration of these values.

Traditionally, financial planning meetings have been held face-to-face in an advisor's office, and over the years, a body of research has emerged showing that how the advisor's office is laid out can have a significant impact on how clients perceive the advisor, their mood during the meeting, and even their resulting financial planning decisions.

Suzanne is a Senior Financial Advisor at Meridian Wealth Management, an RIA based in Lexington, Kentucky, where she oversees approximately $110 million in assets under management for nearly 150 client households.

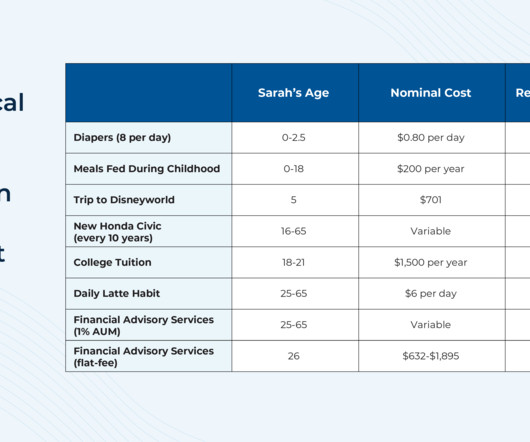

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

Tax-loss harvesting – i.e., selling investments at a loss to capture a tax deduction while re-investing the proceeds to maintain market exposure – is a popular strategy for financial advisors to increase their clients’ after-tax investment returns. Read More.

While strategic advice is crucial, advisors also face the challenge of presenting the strategies to clients in context, explaining different financial planning concepts, and showing clients how to implement these strategies (as well as pointing out any long-term consequences).

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Click to download Financial Disasters Yesterday was kind of a fun day: Sure, it was a dark, damp, dreary February morn when I showed up at the Brooklyn Bridge Marriot, but it was also the first time I did a new presentation in front of a live audience since before the pandemic. Of the 35 slides, 30 were brand new.

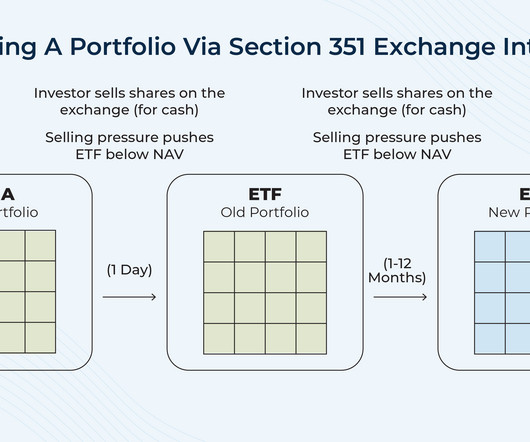

For financial advisors, Section 351 exchanges present a potential solution for clients with high embedded gains, such as those who through the use of tax-loss harvesting have lowered their portfolios' basis to the point where it's no longer possible to harvest any losses to offset the gains realized in reallocating the portfolio.

Niching offers several advantages, allowing advisors to be more specific in their marketing, more targeted in their prospecting calls, and more efficient in their processes (since clients within a similar niche are likely to have similar problems, especially in niches of profession).

Jeff is the Owner and Founder of Cypress Financial Planning, an independent RIA based in Haddon Heights, New Jersey, that oversees $275 million in assets under management for 380 client households.

The need to address longevity risk has become increasingly important, allowing financial advisors to add even more value for their clients by ensuring that their financial needs are met throughout retirement. Ultimately, the key point is that a properly drafted POA is an essential part of every estate plan. Read More.

In the early days of the advicer industry, those questions almost exclusively dealt with facts around a client's or prospect's financial situation to determine (ultimately) what products the adviser should recommend. Instead, meetings (especially initial meetings) happen because there's some 'presenting problem'.

As a financial professional, you have probably noted how different clients react to the presentation of their financial plans. Or perhaps they like it when you show them charts and graphics while others like to have a physical interaction with the information you are presenting.

The chief brand officer of Elements discusses how they provides advisors a way to capture vital client data to present a holistic picture of their financial life.

Thor is the Owner of McIlrath & Eck, an independent RIA based in Arlington, Washington, that oversees more than $610 million in assets under management for 970 client households.

From gradually raising the RMD age to 75 to expanding opportunities to make Roth-style contributions, to increasing the annual limit for Qualified Charitable Distributions, this legislation will likely impact nearly all financial planning clients! How ‘regifting’ can help save money and reduce waste.

For instance, the financial advice industry has seen many changes to regulations (for both advisors and their clients), advisor business models, and the advisor technology landscape. represent our past and present industry's reactive focus on coming up with solutions to address client problems, Financial Advice 3.0

Anh is the Founder and Managing Partner for SageMint Wealth, a corporate LPL-affiliated RIA based in Orange, California, that oversees nearly $325 million for 195 client households.

With another strong year in the markets, most advisory firms are near or at record highs for their revenue, their numbers of clients, and the headcounts of their teams. Which is surprising to some, given that a decade ago, the emergence of so-called "robo-advisors" was supposed to displace human financial advisors and compress advisory fees.

Podcasts Michael Kitces talks with Thor McIlrath of McIlrath & Eck about rotating client coverage. standarddeviationspod.com) Charles Schwab Charles Schwab ($SCHW) clients with $1 million in assets now are automatically enrolled in one of its private wealth management programs.

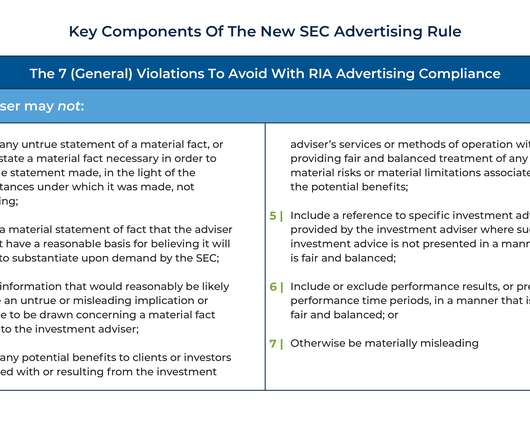

For investment advisers looking to attract prospective clients, advertising the performance of their investment strategies would be a logical way to market their services (at least if they had strong historical returns!). Two final prohibitions under the Marketing Rule include restrictions on the use of predecessor performance (e.g.,

Also in industry news this week: Edward Jones, which added more new CFP professionals than any other firm last year, announced that it is planning to offer financial planning services nationwide, highlighting the value for RIAs and other firms of differentiating themselves amidst increased competition not only for clients, but also for advisor talent (..)

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content