This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We start with several articles on retirementplanning: Why considering a client'sretirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

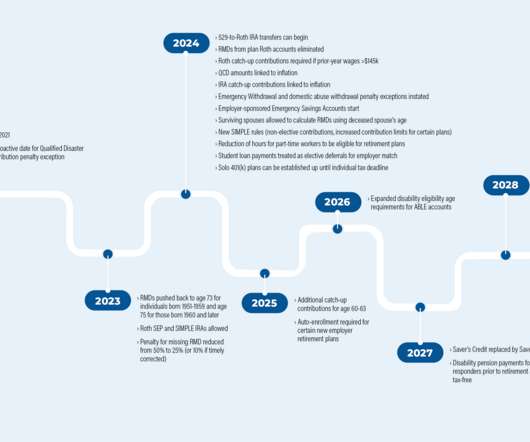

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 Read More.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 Read More.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Podcasts Brendan Frazier on how your clients change will inevitably over time. citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end taxplanning guide. citywire.com) Choreo is buying the wealth management business of BDO USA.

As a result, the list of states where a typical (or even higher-income) retiree would pay very little or even zero tax might be much larger than what might be assumed based on the top marginal rates alone. Every state in the U.S.,

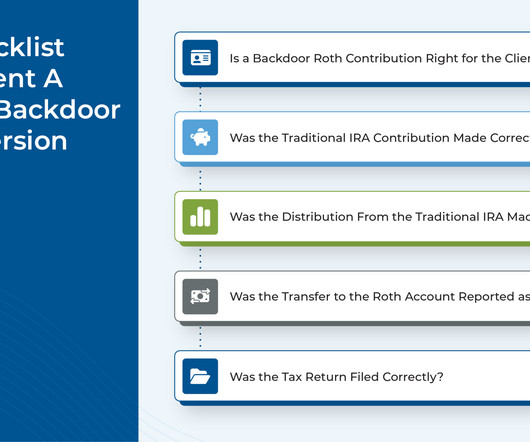

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. The backdoor Roth strategy can be valuable for clients whose high income levels preclude them from making regular contributions to a Roth IRA. Read More.

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Asset diversification is an essential component of effective taxplanning.

(investmentnews.com) On the importance of taxplanning in the first few years of retirement. nber.org) Advisers Stellar client care requires the right metrics. papers.ssrn.com) Four steps to create a digital estate plan. thinkadvisor.com) Why participation in employer-sponsored retirementplans is so important.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Develop a risk management plan to implement strategies that minimize or eliminate risks, and protect your business with appropriate insurance coverage, such as liability, property and business interruption insurance. Get Help with TaxPlanningTaxplanning is a critical component of financial management.

One strategy is to accumulate deductions that a client would normally take over 2 years into a single year. For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Don’t forget about the net investment income tax (NIIT), which is an additional 3.8%

The start of a new year presents opportunities for clients to make positive changes for their financial futures. According to a recent Advisor Authority survey, powered by the Nationwide Retirement Institute®, only 20% of non-retired investors have confidence in their retirementplans despite market volatility.

Gaining a better understanding of this audience can help you connect with and identify potential clients and uncover their needs and wants in a way that benefits you both. Mass Affluent Clients and the Advice They Crave. Generally, a mass affluent client has investable assets between $100,000 and $1 million.

You cannot sell the securities within the retirementplan, then move cash to a brokerage account and purchase the same shares at that point. While within a taxable brokerage account, both dividends and capital gains generally receive favorable tax treatment. This would negate the NUA benefit.

If you are looking for opportunities to grow your business, expanding your services to clients at all stages of the financial planning lifecycle creates new opportunities for you to reach those households in search of professional advice. Starting Out clients are typically focused on beginning to build wealth.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

This is the time to do comprehensive financial planning: retirementplanning, investment planning, taxplanning and estate planning. Help her focus on immediate needs, pay bills, monitor cash flow and review her investment portfolio.

Explore how to reach potential clients by using educational content and CRM systems. It helps them connect with clients and grow their business. You will find tips to improve your online presence, attract more clients, and create successful campaigns. Clients now want financial advice online.

Further, both examples ignore other sources of income, such as wages, pre-taxretirement account distributions, dividends, etc., that could increase the tax due from the surtax. Considering taxplanning strategies to reduce the impact of the new MA surtax. But for others, there might be some strategies to consider.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

This moves your taxable income to the next tax year, potentially lowering your tax bill for 2025. For self-employed individuals : Consider delaying invoicing or billing clients so that payments are received beyond the current tax year. Timing RMDs : Begin taking RMDs by April 1 of the year after you turn 73.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

A fee-only advisor is a financial professional who charges clients a transparent and agreed-upon fee for their services. RetirementPlanning: A fiduciary and fee-only advisor can help you create a retirementplan that takes into account your retirement objectives and current financial situation.

Key Highlights Content marketing helps financial advisors stand out and earn trust from potential clients. When advisors share valuable content for a specific target audience, they can attract new clients and boost their online presence. Content marketing is a great strategic approach to find potential clients.

Thukral explained that this advanced CFP course would help you become a certified financial planner and gain the skills needed to provide sound financial advice to your clients. A new framework helps CFPs better to serve clients, and provide them with the best possible advice. He discussed his insights.

A key first step is creating a clear, written contract with each client, explicitly stating your status as a freelancer or independent contractor. Legally, your clients are only legally required to issue a 1099-NEC for payments exceeding $600. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Some advisors specialize in high-net-worth planning and can direct clients to the unique advantages and opportunities that come with being an HNWI. The most effective financial plan is the one that puts your needs and desires at the forefront. Income TaxPlanning. RetirementPlanning.

Let’s unveil the roles of these dedicated experts, who tirelessly weave strategies to illuminate the path towards their clients’ financial aspirations. Embarking on this journey ensures not only professional growth but also the trust and confidence of clients. Educating Clients: Knowledge is power.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

This has led to the constant lookout for Investment Advisors who are trained to offer clients the right advice and direction concerning investments based upon investment goals, the length of the investment, and the risk appetite. If you are planning your career in this direction, it is the right time to take the plunge in this trade.

CRM stands for Customer Relationship Management and is a technology used to manage your advisory’s relationships and interactions with clients. CRM for financial advisors tracks, manages, and analyzes the interactions you have with clients, prospects, referrals, and strategic partners. The average advisor serves 156 clients.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Certified Financial Planner (CFP) CFPs are professionals who have completed rigorous education, passed a comprehensive exam and have substantial experience in financial planning.

A CRT may be partially tax-deductible right away. iii] Another advantage of charitable giving, particularly assets that have appreciated significantly, is reducing the size of your overall taxable estate for estate taxplanning. If your estate is subject to estate tax after you die, your wealth could take a 40 percent hit.

Our Wealth Advisor, Franklin “Franko” Gay , is passionate about helping others achieve their personal goals by utilizing strategic financial and taxplanning in their day-to-day lives. In summary, shoring up your financials in the decade or less before retirement can be a daunting task when you feel you have a shortfall in assets.

You might be getting likes and comments, but the goal is to turn those interactions into new leads and clients. A few small changes can turn your social media into a client-generating machine. Joe Dowdall isnt just posting on social mediahes using it as a tool to educate, engage, and convert prospects into clients.

To stand out in the competitive world of financial planning, you need more than just excellent financial services or agency support. To attract and retain clients, mastering the art of financial planning marketing is crucial. Highlight how your distinct qualities benefit your clients.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content