This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

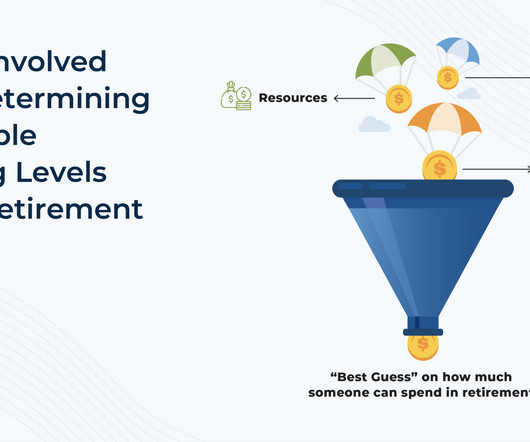

"How much can I spend in retirement?" is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree.

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

These services may range from 'standard' offerings like retirement planning to less traditional areas like credit card consulting. In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients.

Yet, despite the important role that charitable giving can play, studies show that many advisors hesitate to bring up the topic with clients. Advisors may worry about overstepping boundaries or feel uncertain about a client's interest in philanthropy. These statements often stem from clients' life stories and core values.,

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financial planning (as well as consulting with over 15,000 clients on student loan debt).

Over the past decade, a growing number of advisors have expanded into offering comprehensive financial planning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

While it may take a while for the adjustments to take place, advisors can still help their clients plan for the effect of WEP and GPO's repeal by estimating how much the client will be receiving in Social Security benefits once the new law is implemented. will be top of mind for clients affected by the WEP and GPO. Read More.

artofmanliness.com) Ben Carlson talks about the state of the retirement savings market with Shawn O'Brien, Director of Retirement at Cerulli Associates. citywire.com) What's behind the surge in client churn at RIAs? advisorperspectives.com) Does risk tolerance change in retirement?

Which suggests that, amidst ongoing debate over fiduciary-related regulations, an advisor's status as a fiduciary could both lead to greater client trust (both in their individual advisor relationship and perhaps in the financial advice industry as a whole) and, ultimately, higher client retention rates.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that at a time when brokerage firms' cash sweep programs come under increased scrutiny (and as the Federal Reserve has cut interest rates), Charles Schwab (the largest RIA custodian) continues to slash sweep rates for client (..)

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

Some prospects approach an advisor with an immediate 'problem to be solved', such as a fast-approaching retirement date. I help clients in retirement by doing X, Y, and Z."). These situations often narrow the focus of the prospecting conversation, giving the advisor a clear opportunity to affirm their value (e.g., "I

Over the past few decades, advicers have used Monte Carlo analysis tools to communicate to clients if their assets and planned level of spending were sufficient for them to realize their goals while (critically) not running out of money in retirement.

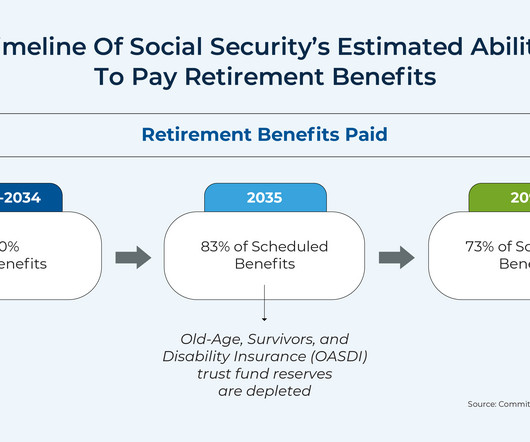

In this environment, financial advisors have the opportunity to add value for their clients not only by giving a clear explanation about the current status of Social Security and the potential legislative changes that could improve its solvency, but also by modeling what (realistic) changes would mean for their clients' financial plans.

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Mann, MBA, CFP I find that so many of my clients, regardless of income, have no idea how much money they are saving. First, I would ask clients how much they were saving each year for retirement. Then I would present the plan to the client. Early in my career, this created quite the challenge in developing a proper plan.

Accumulation-phase planning software won't cut it for solving your clients' complex retirement income puzzles, but there are dedicated applications that can.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Also in industry news this week: While RIA M&A deal flow hit record levels in 2024 (both in terms of volume and the speed of completing them), firm valuations saw relatively modest gains In its latest annual regulatory oversight report, FINRA joined the SEC in flagging the potential risks to firm and client data from the use of third-party vendors (..)

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households.

Jennifer is the CEO of The Mather Group, an RIA based in Chicago, Illinois, that oversees $15 billion in combined assets under management and advisement for approximately 4,400 client households. Read More.

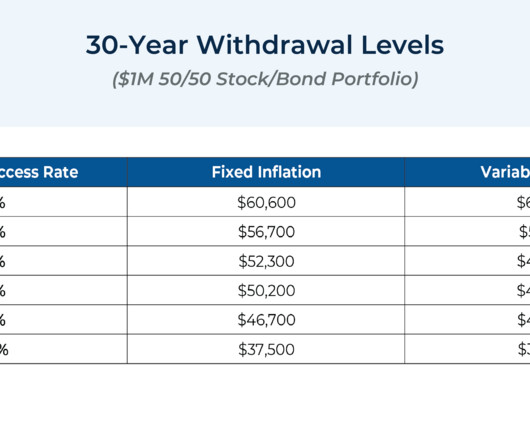

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. the Great Depression or the Global Financial Crisis), showing clients when and to what degree spending cuts would have been necessary.

Liddell, BS As we all do, your clients experience the joys and challenges of lifes many different stages. This may include buying homes, having children, getting married, expanding their business and retiring. Because I practice holistic financial planning, I help clients navigate through all of this.

kindnessfp.com) Why clients need to organize their digital assets for estate planning purposes. riabiz.com) This money manager's ETF business was built on entertaining clients. flowfp.com) Stop using this phrase in retirement planning. thinkadvisor.com) Why clients may feel like they can't have enough assets in retirement.

For many financial advisors, financial planning advice traditionally focuses on optimization: tax-efficient, continually rebalanced portfolios are often designed to maximize a client's wealth throughout retirement. Which can help clients narrow down what really matters to them most.

However, when these aspirations are delayed or blocked by senior advisory firm partners who choose to delay their retirement plans, it can leave younger advisors frustrated and in a place of uncertainty about their futures with their firm.

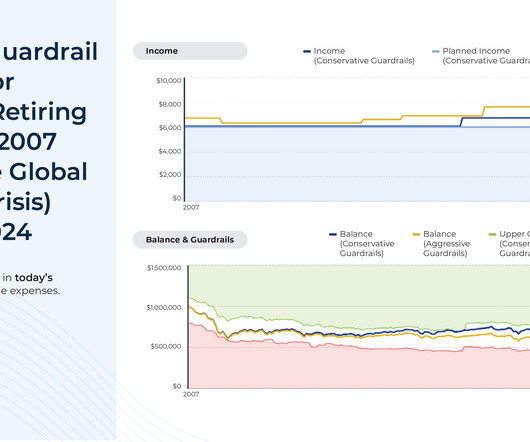

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans. Read More.

Podcasts Michael Kitces talks with Nick Rodkin, managing partner of Stoic Financial, about working with client couples. knowledge.wharton.upenn.edu) Why advisers may spot dementia in clients first. nextavenue.org) Advisers Clients prefer advisers with a fiduciary duty. timmaurer.com) How to better visualize retirement spending.

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Which, if implemented under the new administration, could provide relief for investment advisers, particularly smaller firms that already have to balance compliance with client service, marketing, and the other duties that go into running a firm.

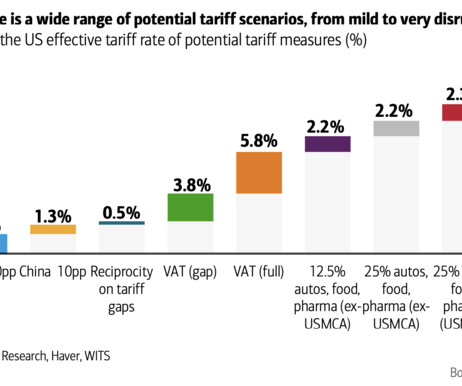

A quick note on tariffs : Over the past few weeks, I’ve been putting together my quarterly call for clients. Its not the same thing in theory, but in practice, especially with the chatter of reducing income taxes, it feels that way: European consumption tax minus the universal health care, education, and retirement benefits.

On April 25, 2024, the Department of Labor (DoL) issued the final version of its Retirement Security Rule (the "Final Rule"), which imposes an ERISA fiduciary standard "that applies uniformly to all investments that retirement investors may make with respect to their retirement accounts ".

For many financial advicers, helping long-time clients identify and progress toward their goals eventually transitions into conversations around the best ways to enjoy the fruits of their labor once they reach them. And by ensuring that their clients are equipped with (and know how to follow!) Read More.

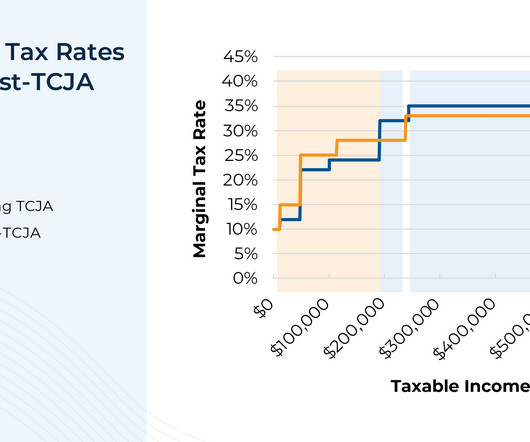

From an advisor's perspective, TCJA's impending expiration raises the importance of planning for clients who will potentially be impacted, which, given the law's broad scope, could be nearly every client. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content