This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

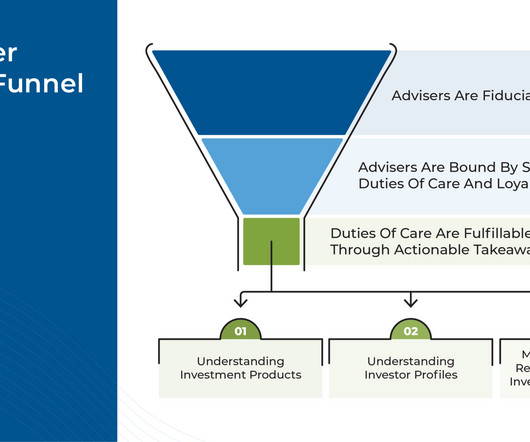

There is a general understanding that investment advisers have a fiduciary relationship with their clients – in other words, that they are required to act in the client's best interests. These 3 components in practice make up a core part of the adviser's fiduciaryduty to their clients.

For example, if an advisor recommends an investment that prioritizes the commission they would receive rather than any benefit the client would derive from it, they could incur fines and sanctions for violating their fiduciaryduty as an advisor.

In contrast, a commission-based financial advisor receives commissions or other forms of compensation from financial product providers for recommending and selling their products. This can make it difficult for investors to fully understand the potential conflicts of interest that may exist when working with a commission-based advisor.

In contrast, a commission-based financial advisor receives commissions or other forms of compensation from financial product providers for recommending and selling their products. This can make it difficult for investors to fully understand the potential conflicts of interest that may exist when working with a commission-based advisor.

When researching wealth management firms, paying attention to their credentials and qualifications is essential, including whether they have a fiduciaryduty to uphold. Regulatory Compliance Ensure the wealth management firm is registered and compliant with relevant regulatory authorities.

When researching wealth management firms, paying attention to their credentials and qualifications is essential, including whether they have a fiduciaryduty to uphold. Regulatory Compliance Ensure the wealth management firm is registered and compliant with relevant regulatory authorities.

Just a reminder that nothing in this podcast can be interpreted as a product, insurance or investment recommendation of any sort, nothing in this podcast can be interpreted as the legal or compliance advice, or any recommendations specific to your or your client’s personal situations. Please consult a consultant. Advisor or attorney?

While this requirement might sound relatively straightforward, the lack of a single definition for what this duty actually requires can make it challenging for advisers seeking to understand precisely what it means to comply with this responsibility. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content