This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that NAPFA has announced that it will no longer exclude advisors who receive up to $2,500 in annual trailing commissions from previous product sales, if they agree to donate that money to a non-profit organization (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the SEC this week fined 4 RIAs for violations of its marketing rule related to their claims that they offered 'conflict-free' financial advice.

Also in industry news this week: A recent study finds that having a defined marketing strategy is a linchpin of marketing success, as advisors with a defined strategy were more likely to have seen an increase in inbound leads during the past 12 months and have more confidence in meeting their practice goals during the coming year than those without (..)

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management.

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management.

billion in feeonly asset flows for the full year 2013; 37% of Morgan Stanley wealth management’s total client assets are now in fee based accounts a record high. I’ve lost count of the number of times that 30 seconds into an interview, I’ve gotten a side-eyed glance from him that says “ Loser. It’s uncanny.

The best way to solve this problem is by increasing the number of fee-only SEBI Registered Investment Advisors (RIAs) who by design think in the interest of clients. By regulation, RIAs can’t earn from commissions received from product companies.

Below are the different types of financial advisors you can choose from based on their fee model: 1. Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products.

The advisors can be differentiated based on the fee structure they use to charge fees such as fee-only, commission-only, hourly-fee, monthly fee, etc. It may also be the case that the advisor pushes a particular investment in the hopes of earning a commission.

.” Only 4 percent of Certified Financial Planner™ professionals identify as Asian American or Pacific Islander (AAPI), though they make up 6.2 1,2 Despite the small numbers, AAPI professionals remain the largest ethnic minority within the financial planning profession. percent of the American population.

They may charge for their services either on a commission basis or hourly rates. However, our advice is to trust financial planners who either take a flat annual fee or charge per hour for managing your portfolio instead of charging a commission on every stock they buy or sell. Go for Fee-Only Financial Advisors.

As you are researching your wealth management options, you will see a number of names for those who can help you invest, including brokers and advisors. Brokers are paid by a commission on the investment products they sell. Fiduciary advisors are generally fee-only. Let’s break it down. How Are They Paid?

Soft Skills – The role of a financial advisor goes beyond reading numbers, interpreting them, and offering advice to clients. There are two types of Financial Advisors in India – Fee-Only Advisors and CommissionOnly Advisors. Numerous software and tools can do these jobs right now.

The obvious next priority to put on the regulatory watch list is sales commissions. I think it’s self-evident that any product that has to pay people to recommend it is probably not competitive on its own merits.

Depending on the target asset allocation, there can be a number of ways for a portfolio to drift. Trading costs vary by platform and commissions may apply if you’re not working with a fee-only advisor. Then work down, perhaps going to U.S. The costs of rebalancing Does it cost money to rebalance?

However, the numbers tell a different story. According to the Federal Trade Commission (FTC), in 2021, American consumers lost over $5.8 million consumers filed a fraud report, the highest number since 2001. However, the FTC expects the actual numbers to be higher than the reported numbers since multiple scams go unreported.

This is the time of year when the various industry magazines come out with their broker-dealer surveys, listing the ‘top’ BD rankings based on total revenues or the number of ‘producing’ reps. The number of reps gives the FSI the appearance of heft in its primary activity, which is lobbying. What is it lobbying for?

But a disturbing number of advisors who go through its appeals process have used the term ‘kangaroo court’ to describe their experiences, and of course the organization has, in the past, leaned over backwards, nearly breaking its back, to accommodate wirehouse CFP brokers.

If their sole method of compensation is a product, and/or they are taking commissions, then in reality it is less likely they are embracing all the values that the standard requires. Commissions are opaque. But if they are acting in the capacity of a broker or agent then they are not bound to follow the fiduciary standard.

As discussed above, starting early can have a number of benefits. Financial advisors can be hired on fee-only or commission-based models. When to start planning for retirement. While there is no fixed time to start planning for retirement, it can benefit you more if you start early. You can be much more relaxed.

As discussed above, starting early can have a number of benefits. Financial advisors can be hired on fee-only or commission-based models. When to start planning for retirement. While there is no fixed time to start planning for retirement, it can benefit you more if you start early. You can be much more relaxed.

” As an hourly financial advisor he doesn’t make commissions for recommending products such as private REITs, structured products, etc. It’s all your number… How much are you managing it? I was managing their money in. SARA GRILLO, CFA: The attire you hybrid or A and M. That’s how you get paid.

KEY POINT For advisors: When you look at the illustration and you see an illustrated rate that is 5, 6, 7% based on the maximum AG 49 rate, which is the cap applied to the historical data, as an advisor you should ask for a much lower number, such as 2-4%. Undisclosed #3 Try to ignore the illustration The illustrations are a distraction.

I mean, how is the CFP Board even going through a process of due diligence, again, innocent till proving guilty in the sense when they have all kinds of disclosures, but at the same time, they’re publicly reprimanding 40 people, 80 people, whatever the number is, in a given year, out of the tens of thousands.

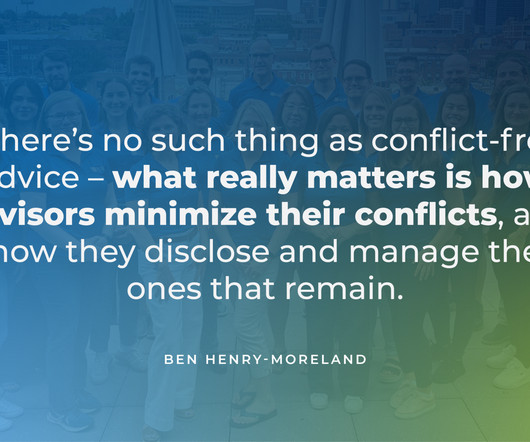

And given the sheer number and scope of potential conflicts that do exist in the advisory industry (where a wide range of providers seek to incentivize advisors to recommend their products and services to clients), there's a vanishingly small number of RIAs that don't have at least some form of actual or potential conflict to disclose.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content