This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that the Department of Labor released the final version of its Retirement Security Rule (a.k.a.

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that NAPFA has announced that it will no longer exclude advisors who receive up to $2,500 in annual trailing commissions from previous product sales, if they agree to donate that money to a non-profit organization (..)

Enjoy the current installment of "Weekend Reading For FinancialPlanners" – this week's edition kicks off with the news that a recent survey sponsored by CFP Board demonstrates the upsides of a career in financial planning, from a median salary of nearly $200,000 to flexible work schedules and a strong sense of purpose among advisors.

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that a recent study by Cerulli has shown a sharp increase in the number of affluent investors willing to pay for advice, which on the one hand reflects the increasing financial complexity in peoples' lives (while they've also gotten (..)

But these positions are often tenuous for new advisors, with extremely high failure rates, driven in large part by compensation that is reliant primarily on commissions from product sales.

Stockbrokers, registered representatives, dual registered advisors, insurance agents, and other types of advisor-sales roles don’t always have to act in your best interest depending on the situation. For non-fiduciary financial advisors, recommendations may only need to be suitable , not necessarily in the client’s best interest.

When it comes to choosing a financialplanner, it’s important to choose the right fit for you. Do the research of the available advisors – the first step is to find a financialplanner who will help you plan your finances. A planner should be able to answer any question that you may have regarding his services.

I am an irreverent and fun marketing consultant for financial advisors. Before we get started, I wanted to give hanks to Jonathan Grannick of Wonder Wealth , as well as other financialplanners for their input. What is a financial paraplanner? How do you get a job as a financial paraplanner?

Fee-Only financial advisors and firms receive no sales-related compensation or incentives. Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose. Alicia Vande Ven , M.S.,

Fee-Only financial advisors and firms receive no sales-related compensation or incentives. Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose.

Different Types of Investment Advisors FinancialPlanner: A financialplanner assists individuals achieve their financial goals. They help clients manage their financial aspects and develop customized strategies based on their needs. Excellent communication and interpersonal skills.

If you’re as old as Methuselah, like I am, you might remember a pivotal moment in the evolution of the planning profession, when Forbes magazine noticed that brokers, life insurance and tax shelter salespeople were starting to call themselves ‘financialplanners.’ But not as a financialplanner.).

Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products. Choosing a fee-only financial advisor offers several benefits.

In this article, we’ll dive into the many tax and financial considerations of buying and selling real estate, how real estate fits into estate planning, and the role that a wealth manager or financialplanner can play in guiding your decision-making. down payment.

The petition notes that the SEC, in response to litigation from the Financial Planning Association back in 2005, had proposed to go further, and require anyone holding themselves out as a “financialplanner” or providing “financial planning services,” or delivering a financial plan to their customers, be required to register as an RIA. .

Some of us remember that the consumer revolution, which phased out salespeople and put the consumer in charge of selecting purchases based on price and quality, was very slow to enter the financial services world. So how does financial planning fit into this?

However, stock compensation, large bonuses, commissions, etc., The sale of the stock is treated as a capital gain or loss, subject to the holding period at the time of sale. The gain or loss on the subsequent sale of the stock is subject to the capital gain/loss treatment (i.e.,

Watch as all h&#@ breaks loose discussing the question of broker vs. financial advisor, commissions, fees, value, and more! The advisors made the point that the cost of insurance can’t be separated from the “cost of service” or the commission the agent makes. The commission is the commission. Who cares?

The standard, however, is often used haphazardly, invoked as a sales tool by dual-registered advisors who want to virtue signal, only to be abandoned in a legal context by those same advisors who backpedal into being “just a salesperson.” Commissions are opaque. Let’s talk about it. This is where the confusion comes in.

Once the course is complete, I do some continued marketing and client support which amounts to just a few hours per week, while sales roll in month after month. Assess your skills When I started GoodFinancialCents I was a Certified FinancialPlanner looking to grow my business and answer common client questions.

But yeah, I was making commission at that point in time. So when I was a salesperson at Business week, I sold more ads than anybody, and I made $2 million commission when I was 29 years old. So I went to Yahoo and worked on their revenue and sales and marketing for a few years. The, the prompt loses them a sale.

I think we all know about the long, slow transition from sales, to service, to expertise and advice, and how the early promoters of the trend were rewarded with a first-mover advantage. Some of them told me stories.). I’ll offer one more topic we plan to talk about: practice management.

And that’s why I’m writing this blog; because I feel that financial advice rendered by the hour is a great thing for the American public (for the reasons we’re going to discuss below). But the idea of becoming an hourly financialplanner is met with such resistance you would think you told people to saw off their left arm.

B y now, I’m sure most of you are familiar with the Committee for the Fiduciary Standard—but if not, well, it’s a group of prominent advisors who advocate that anybody who holds out as a financialplanner or advisor be held to a strict fiduciary standard. Or will brokers go back to winning sales contests?

In my case, it was my experience as a financialplanner. Best of all, none of those brokers charge commissions for buying and selling individual stocks. “I I even put together an article, Best Items for Garage Sale Flipping for Fun and Profit , listing some of the best items for profitable sales.

Baby Boomers and retirees are the prime target market for the annuity sales types. For example, an insurance agent or registered rep is not going to show you a product from a low cost provider who offers a product with ultra-low fees and no surrender charges because they receive no commissions. What is an annuity?

Early on in his entrepreneurial journey, Scott saw firsthand the inherent flaws and conflicts of interest in the traditional sales and product driven approach, as several family members had lost a significant portion of their hard-earned life savings to high-cost, commission-based investment products and inappropriate advice.

Early on in his entrepreneurial journey, Scott saw firsthand the inherent flaws and conflicts of interest in the traditional sales and product driven approach, as several family members had lost a significant portion of their hard-earned life savings to high-cost, commission-based investment products and inappropriate advice.

Salaske: Yeah, I don’t agree with the CFP Board becoming any type of regulator whatsoever over financial advisors, financialplanners, whatever you wanna call us in the advice space. Wright: Well, and to respond to that, if I may. The confusion is with the CFP.

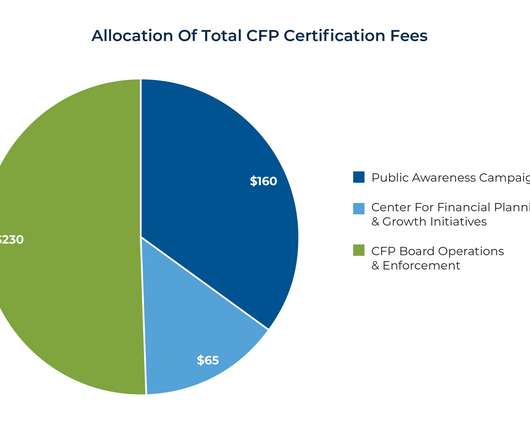

In our debate we will discuss the following questions: The CFP Board harms consumer through its multi-million dollar ad campaigns by suggesting that CFPs are more ethical than non-CFP financialplanners and by suggesting that its member standards are higher than those of regulatory agencies. Source: SEC. Source: CFP Board.

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that President-elect Trump plans to nominate former Securities and Exchange Commission (SEC) Commissioner Paul Atkins as the next SEC chair, replacing Gary Gensler.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content