This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understand the basics first, and then create an estateplan. Wills and trusts are both important estateplanning tools with important differences. A will ensures property is distributed after your passing, according to your wishes, while a trust goes into effect as soon as you create it. A Will vs. a Trust.

Fortunately, financial professionals have tools and wealth transfer strategies that can help couples be intentional about the use of their assets in an estateplan. Why Focus on EstatePlanning for Blended Families A thoughtful plan and good communication can go a long way in heading off conflict in large families.

The Imperative of EstatePlanning: Not Just for the Affluent Often, there’s a prevailing misconception that estateplanning is a luxury reserved for the wealthy elite. Real estateplanning is a crucial undertaking that every adult and family should prioritize.

While a financial plan focuses on managing your finances during your lifetime, an estateplan is essential for determining the fate of your assets after you pass away. Estateplanning involves the transfer of your assets to your heirs in the event of your passing.

An estimated 90% of wealthy families lose their wealth by the third generation, so if you are planning on leaving behind assets to your family, knowing the unique risks to the affluent investor and considering strategies to maintain your wealth within your family can be very beneficial. [1]

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. In this case, you can speak with your estateplanning attorney about gifting stock to family outright during your life (perhaps someone in a lower tax bracket!)

Help the elderly with estateplanningEstateplanning is an integral component of financial advice for seniors. can take advantage of a situation and misuse the client’s estate. However, proper estateplanning can help in these situations. Children, grandchildren, spouses, ex-spouses, etc.,

Since investors pay tax annually on dividends, interest, and capital gains distributions in a taxable brokerage account, even if they don’t sell assets, it can be worthwhile to consider allocating more tax-efficient investments here. At this time, the major tax changes in 2026 are widely expected, but nothing is set in stone.

Stage Four: Leaving a Legacy In the final phase of the financial planning lifecycle, which is also known as the wealth transfer stage, your clients will be preparing to pass on any remaining wealth to their loved ones and/or charities in a tax-efficient way.

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ Individuals who inherit a concentrated stock position should speak with their estateplanning attorney to confirm whether they’ll receive a step-up in basis.

A financial advisor possesses a deep understanding of complex financial concepts and can help you navigate the intricacies of investing, retirement planning, debt management, estateplanning, succession planning, tax optimization, and more. For instance, you may discuss estateplanning.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Certified Financial Planner (CFP) CFPs are professionals who have completed rigorous education, passed a comprehensive exam and have substantial experience in financial planning.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Certified Financial Planner (CFP) CFPs are professionals who have completed rigorous education, passed a comprehensive exam and have substantial experience in financial planning.

Yesterday it was early retirement projections for a corporate executive, tomorrow it’s a call with a planner to review a client’s estateplan. We spend about 12 hours reviewing and updating an established client’s plan each year, but I’m only responsible for about 4.5 hours of it.

Since investors pay tax annually on dividends, interest, and capital gains distributions in a taxable brokerage account, even if they don’t sell assets, it can be worthwhile to consider allocating more tax-efficient investments here. At this time, the major tax changes in 2026 are widely expected, but nothing is set in stone.

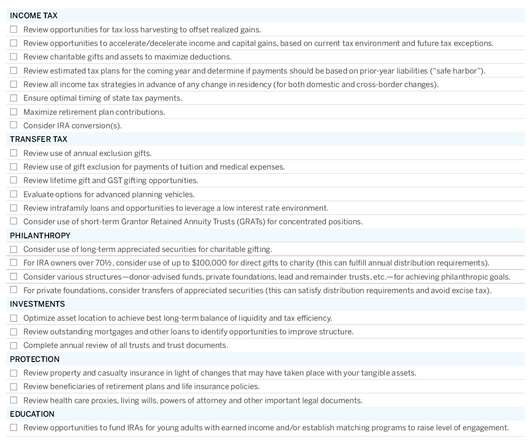

Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. You can find our annual planning checklist at the end of this article. It is important to evaluate near- and long- term planning options annually—each year can bring different opportunities.

AGI includes all taxable income, including wages, bonuses, taxable interest, dividends, capital gains, retirement distributions, annuities, rents and royalties. Distribute income out of trusts to reduce federal taxes. Gift and Estate Taxes. This is particularly true with the advent of the additional NII tax.

Spice Packages From Spiceology When it comes to gifting, we are all about thinking outside the box, so this client gift idea from Amanda Singletary, MBA , Marketing Manager at Cary EstatePlanning , is excellent. Melisa Joy, CFP® of Pearl Planning. Spiceology is a spice company based out of Spokane, Washington.

The outcome of the tax reform debate is likely to impact how we advise clients on tax planning, estateplanning and a host of other topics. are distributed to beneficiaries. These transactions are designed not to generate gift or estate taxes. Since last year’s U.S.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

This includes how we plan and manage our estate. Effective estateplanning is an act of financial stewardship. With our estate, we have the immense power to bless others, including our families, children, and charitable organizations we care about. In fact, your estateplan can reflect your deepest held values.

Your personal preferences and the potential good your bequests can do are factors to think about in your estateplanning. What Is Estate Equalization? Basically, estate equalization is the process of helping ensure fairness in your estateplan, whether that means leaving all your primary heirs the same bequests or not.

Comprehensive Tax Planning A flat per-service fee charged for filing a business’s taxes Between $1,000 and $20,000 or more annually. A CPA or tax attorney may charge an individual $10,000 per year to create a tax plan around venture capital fund distributions and crypto investments.

xyplanningnetwork.com) On the benefits of distributing equity in wealth management. investmentnews.com) Advisers How we communicate has changed. newsletter.abnormalreturns.com) Estateplanning is becoming table stakes for wealth managers. (investmentnews.com) RIA aggregators are the solution to the succession problem.

I mean, how… How much time do you need to spend with somebody who’s going through this major life change, maybe they’re retiring selling their business, maybe they’re getting divorced, how much actual time does the advisor need to speak with them and help them hit an hour, maybe two hours, maybe.

However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. Estateplanning is one of the key components of financial planning these individuals need to focus on. This makes asset protection a significant concern. in their work endeavors.

Navigating the complexities of estateplanning can often feel like charting through uncharted waters, especially when it comes to handling assets, taxes, and ensuring one’s legacy is preserved according to their wishes. Techniques such as swapping assets with a higher basis out of the estate can help achieve this objective effectively.

Types of Family Trusts To make estateplanning a bit more confusing , there are different types of revocable trusts. Limitation of exposure to estate taxes , as part of a proper estateplanning process. Additionally, there may be estate tax implications when assets are transferred into or out of the trust.

And so we don’t do the payment for distribution. There is that same payment for distribution service, the mutual funds. So there’s the, “Hey, I’ll work with you and we’ll develop goals and a plan how to get there.” They’ll do tax planning, right? That’s right, Barry. RAMPULLA: Right.

If your parent had a trust, the individual(s) named in the trust documents as successor trustee will control the distribution of the trust assets. Checklist for executors of their parent’s estate Get organized Where are the original estateplanning documents located? Who is the attorney who drafted the estateplan?

An essential step in estateplanning is making sure beneficiaries know all the responsibilities and challenges that accompany the management of increasing wealth. When an aging parent with an air-tight estateplan fails to prepare heirs for an inheritance, an act of kindness runs a high risk of backfire.

Such protection can be a cornerstone for sound estateplanning. This empowers an independent trustee to manage the trust assets and make decisions regarding distributions to descendant’s. If necessary, the trustee can distribute assets to a descendant. Shielding Assets.

EstatePlan: The prenuptial agreement also addresses each spouse’s disposition of assets on death and sets the “floor” of what each spouse must leave the other. It’s important to understand—and communicate to your child—that wanting to protect their wealth isn’t only about money or completely cutting off the divorced spouse.

For clients whose net worth falls below the federal exemption limit, we still recommend that they review their existing estateplanning documents with us and their other advisors, to determine if any of the new tax formulas are poised to create undesirable results. These transactions are designed not to generate gift or estate taxes.

Updating the EstatePlan: The prenuptial agreement also addresses each spouse’s disposition of assets on death and sets the “floor” of what each spouse must leave the other. Meaning, if a spouse is a beneficiary of a family trust, his/her spouse will not be entitled to distributions from that trust.

The goal is to treat each child fairly, and communication and transparency are crucial. EstatePlanning When creating an estateplan for a blended family, it’s best to get rid of old documents and start fresh.

If your parent had a trust, the individual(s) named in the trust documents as successor trustee will control the distribution of the trust assets. Checklist for executors of their parent’s estate Get organized Where are the original estateplanning documents located? Who is the attorney who drafted the estateplan?

Terms like “estateplanning” and “wealth transfer” provide little shelter from a painful reality—a large portion of what we do as advisors focuses on the issues associated with our clients’ mortality. The amount converted is subject to income tax at ordinary rates, but this income-tax liability reduces the size of a taxable estate.

Their compensation may take the form of consulting income, business distributions or equity ownership. Our next priority was to ensure Sharon’s estateplan was in place and up to date. Today, many of them find themselves in sectors shifting toward non-traditional corporate structures or work settings.

Their compensation may take the form of consulting income, business distributions or equity ownership. Our next priority was to ensure Sharon’s estateplan was in place and up to date. Today, many of them find themselves in sectors shifting toward non-traditional corporate structures or work settings.

Where an individual’s combined traditional IRA, Roth IRA and defined contribution retirement account balances exceed $10m at the end of a taxable year, the required minimum distribution (RMD) for the following year will be 50% of the excess total account value over $10 million. Corporate Income Tax.

Provisions recently extended or made permanent include tax-free treatment of some distributions to qualified charities from retirement plans, as well as several provisions designed to benefit small business owners and entrepreneurs. This is also helpful with planning related to the NII tax.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content