This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, not all prospects have immediate financial concerns. While these individuals may genuinely be interested in financialadvice, they might also feel ambivalent about the timing, relevance, or ultimate value of working with an advisor. I help clients in retirement by doing X, Y, and Z."). Read More.

Which could prove to be a boon for the financialadvice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?).

How much to charge for financialadvice is rarely a decision made lightly. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning.

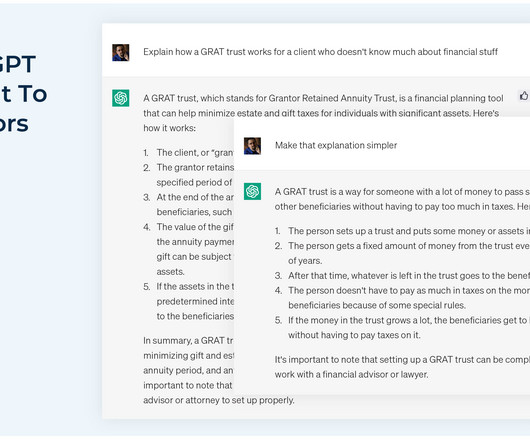

These responsibilities also extend to the use of any technology used in the process of giving advice: A recommendation made with the aid of technology still needs to be in the client's best interests, while the technology also needs to carry out any function as it's described in the advisor's marketing materials and client communications.

As such, new firms that start with low fees might make plans to raise fees quickly and, in the meantime, avoid promising clients that the fees will stay the same. And while new clients often come in at higher fees, early clients may still be paying well below the firm's current rates.

riabiz.com) Creative Planning is exploring its custody options. riabiz.com) Archive Intel has entered the adviser communications archiving space. blogs.cfainstitute.org) How life events affect retirement planning. papers.ssrn.com) Advisers There is an tension inherent in the practice of financialadvice.

The traditional way that most financialplanning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client's financial strategy that was delivered either on a one-time basis or updated annually.

As financialplanning has evolved over the years, better tools have become available to help advisors maximize their impact with more clients by increasing their efficiency. However, as advisor technology continues to evolve, many tools have focused on helping advisors scale their financialadvice to accommodate growing businesses.

There are many financial advisors who take issue with the financialadvice offered by popular personal finance personalities such as Dave Ramsey. Though many potentially valid criticisms of this process tend to concern technical details (e.g.,

About a decade or so ago, one of the most pressing issues facing the financialadvice industry was the threat of an imminent deluge of advisor retirements coupled with a paucity of succession plans to transition clients to the next generation.

(riaintel.com) How AI will play a role in the provision of financialadvice. wsj.com) Family Communication is important for every family, but especially for the wealthy. thinkadvisor.com) Blended families don't plan their money lives in advance. thinkadvisor.com) 7 things that clients hate that financial advisers do.

standarddeviationspod.com) Brendan Frazier on getting clients to actually implement your advice. podcasts.apple.com) The biz Software is eating financialadvice. thereformedbroker.com) How financial advisers can publish their own book. riabiz.com) Demand for financialadvice is only increasing.

For most of its history, the financialadvice industry has been very slow to change. Additionally, those promoting change can be very clear about what the process will entail and how it will be implemented (with the caveat that the plan needs to be flexible to allow for change as conditions evolve).

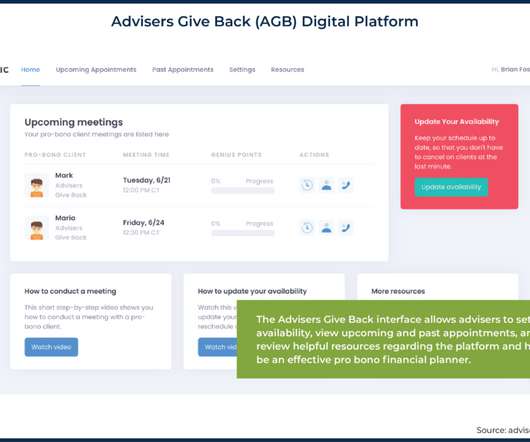

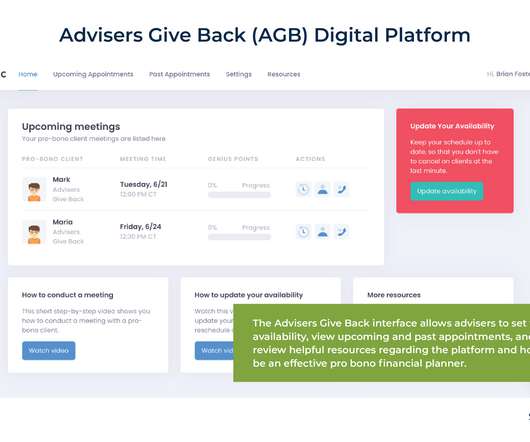

By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives. Pro bono financialplanning refers to free, no-strings-attached financialadvice and planning for underserved people.

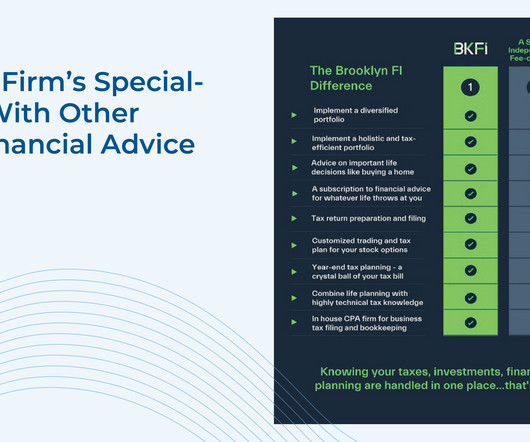

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-only financialplanning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet FinancialPlanning.

Consumers have a wide range of options when it comes to choosing a provider of financialadvice, from larger wirehouses and asset managers to smaller Registered Investment Advisers (RIAs).

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the SEC this week fined 4 RIAs for violations of its marketing rule related to their claims that they offered 'conflict-free' financialadvice.

Initial outreach to a financialadvicer rarely (if ever) results from a prospective client waking up in the middle of the night in a cold sweat because they just figured out that they're in desperate need of a comprehensive financialplan.

By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives. Pro bono financialplanning refers to free, no-strings-attached financialadvice and planning for underserved people.

In particular, financial advisors who offer ongoing services to clients can focus on 3 key areas that are unique to service-based sales as part of a successful sales strategy.

When it comes to politically charged discussions, financial advisors generally try to stay neutral and focus on providing clients with objective financialadvice. These clients may just need someone to talk to, and the advisor can help by providing reassurance on the status of their financialplan.

Also in industry news this week: A legal challenge to FINRA's operations as a self-regulatory organization has the potential to upend the current regulatory system for broker-dealers and their registered representatives A recent study indicates that while many consumers appear confident handling their finances on a 'DIY' basis during their careers, (..)

But in reality, none of these advances meant the end for the advice industry; rather, they often made financial advisors more productive by increasing their efficiency with back-office tasks from producing financialplanning calculations more quickly and accurately to being able to serve more clients across the country.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that Congress appears poised to pass a series of changes affecting retirement planning, dubbed “SECURE ACT 2.0”, ”, by the end of the year. Social Security COLA for 2023.

For many financialadvicers, helping long-time clients identify and progress toward their goals eventually transitions into conversations around the best ways to enjoy the fruits of their labor once they reach them. And by ensuring that their clients are equipped with (and know how to follow!)

Welcome back to the 346th episode of the Financial Advisor Success Podcast ! Jim is the founder of MainStreet FinancialPlanning, an hourly, fee-only financialplanning firm, and also created Procrastination Junction, a coaching program for fee-only financial advisors looking to improve their sales skills.

Meaningful communication is crucial to building strong, durable relationships, and asking effective questions is an essential part of facilitating impactful conversations. More often, initial outreach from a prospect occurs because there's some urgent issue they need help with.

Ultimately, the key point is that there are a number of ways that the financialplanning industry can tackle the looming spike in demand for new advisors without imposing an artificial obligation on advisors, which, if not met, would imply a deficiency in professional duty.

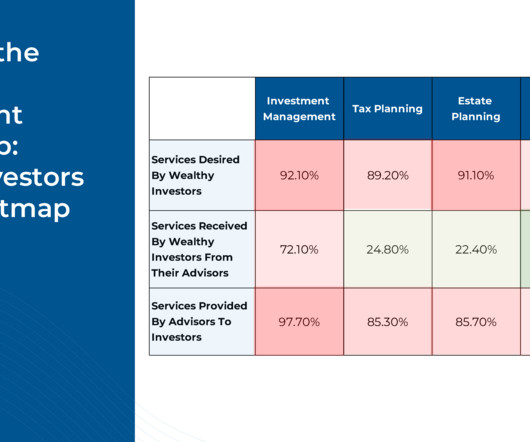

For example, an advisor may think of "risk management" in terms of life and property insurance coverage, whereas HNW clients may instead think of tax and estate-planning strategies as asset protection measures – particularly for the future wealth of their heirs.

a single person, a couple, a business, or a retirement plan) and the date on which the agreement will become effective. To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g., The agreement should also lay out some acknowledgments for the client to review.

a single person, a couple, a business, or a retirement plan) and the date on which the agreement will become effective. To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g., The agreement should also lay out some acknowledgments for the client to review.

For many financial advisors, the most valuable part of what they offer comes down to the financialadvice that they give, whether it be the expert guidance they give to a certain niche or a unique point of view that presents unique insights to an individual client. developing a valuable offering for consumers.

And for financial advisors who want to offer planning services to individuals who may not have the means to work with a financial advisor on an ongoing basis, specializing in certain niches can even prove lucrative enough to profitably sustain incorporating pro bono or low-cost services as part of their practice. Read More.

Offering financialadvice can mean many things for different financial advisors, and there are many reasons that advisors choose to join the planning profession.

The unique dynamic of presenting fees to clients can be heightened when an advisor offers life planning, which may involve multiple meetings to truly understand the prospect's situation before the advisor even presents the fee for an in-depth plan. Read More.

Key Highlights Millennials can benefit a lot from getting financialadvice. You should change your marketing approach to meet the specific financial needs and interests of millennials. Listen to their concerns and adjust your financialadvice to align with their goals. Right now, few of them use advisors regularly.

For over a decade, the financialadvice industry has been bracing for an "any-minute-now" tsunami of advisor retirements and concomitant sales of financialplanning practices. Which begs the question, to what extent should an advisory firm owner discount the sale price of their firm for a next-gen successor?

Podcasts Christine Benz and Jeff Ptak talk with Stacy Francis who is president and CEO of Francis Financial about working with female clients. morningstar.com) Brendan Frazier talks with Ted Klontz about how to better motivate, communicate and connect with clients and prospects. thinkadvisor.com)

Key Highlights The financialadvice world is changing. RIAs need to update their marketing plans to stay ahead. They need to put in more effort to attract prospective clients looking for financialadvice. Understanding the Marketing Landscape for RIAs The world of financialadvice is changing fast.

Natalie is the owner of Natalie Taylor Consulting Services, an independent virtual RIA, and is also the Head of FinancialAdvice for Monarch Money, a personal financial management tool that helps consumers track their spending and net worth over time.

In the initial stages of their careers, many financialadvicers find that, with little revenue coming in and less than a full load of client-facing work to do, they spend the majority of their time on operations and marketing as they try to establish their practice.

The importance of getting women into financialplanning feels like it should go without saying. Unfortunately, we’re not quite there yet as a society, since as of 2022, the Bureau of Labor Statistics reports only a third of financial advisors are women. In 2022, nearly 42% of the externships participants were women.

Of an estimated 104 million households seeking some level of financialadvice, 88 million of those households want that advice from a financial professional. In this overview, we will explore the demographics of each stage, the financialplanning needs of people in each stage, and strategies for serving them.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content