This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

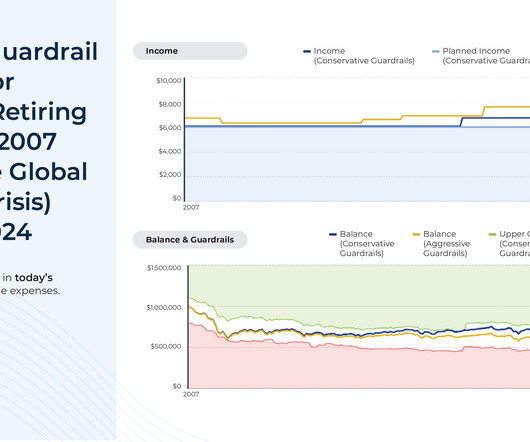

But by communicating the guardrails withdrawal strategy (and not necessarily the underlying Monte Carlo probability of success changes) to clients, advisors offer them both the portfolio value that would trigger spending changes and the magnitude that would be prescribed for such changes.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years. Retirementplanning is not just about reaching a target savings number.

Before making any investment decisions, consider all the factors as well as your personal risktolerance and retirement income needs. As you evaluate how to retire comfortably or achieve financial flexibility, (re)consider the importance of living off dividends in your financial plan. versus 1.1%

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

The financial planning process adds value to your journey through life, and people skilled at helping clients through that process have spent years developing technical and emotional expertise for life’s journeys ahead. Consider the client’s goals, risktolerance and objectives in providing investment advice.

Their primary objective is to help clients make informed investment decisions, manage risks, and achieve financial objectives. Investment advisors analyze market trends, assess the client’s economic situation, and develop personalized investment strategies tailored to their goals and risktolerance.

A financial advisor possesses a deep understanding of complex financial concepts and can help you navigate the intricacies of investing, retirementplanning, debt management, estate planning, succession planning, tax optimization, and more. Make a note of their communication skills and interest in the conversation.

Wealth managers work closely with their clients to understand their unique financial situations, risktolerance, and investment goals to develop customized solutions that meet their needs. It is a holistic approach that focuses on the integration of various financial services to help clients achieve their goals.

Credit planning. Retirementplanning. Estate planning. Financial advisors also spend years developing strong listening and communication skills to help you talk through your goals, uncover hidden risks and plot a course to work towards success. Saving for big purchases. Wealth management.

In case of any doubt or discrepancies, it is vital to communicate with your financial advisor openly. Communication is key in the evaluation of investment performance. Communication is key in the evaluation of investment performance. Transparent communication is paramount in risk management.

To succeed as a financial advisor your focus should be more than just finance, investing, and a retirementplan. That can be done by asking the right financial planning questions and providing your clients with a unique and extraordinary advisor-client experience. Category: Client Relations.

It helps to encourage open communication about financial expectations and work together to develop a plan that promotes independence while ensuring financial stability for both parties. Effective communication is essential in navigating the delicate balance between supporting adult children and prioritizing retirement savings.

A well-defined value proposition helps you: Communicate more effectively. Financial planning is about more than just managing your money. It’s about understanding all the factors that impact your financial future, including your income, expenses, investments, and risktolerance. Keep promises to your clients and.

You can learn about the stock market, bonds, budgeting, retirementplanning, and saving. How does communication work? If you have strong opinions on the impact of your investments, then make sure you choose a financial advisor who aligns with your values and understands your risktolerance or how risk averse you are.

You can learn about the stock market, bonds, budgeting, retirementplanning, and saving. How does communication work? If you have strong opinions on the impact of your investments, then make sure you choose a financial advisor who aligns with your values and understands your risktolerance or how risk averse you are.

To define your target audience, consider things like age, income, investment goals, risktolerance, job, and lifestyle. These could include subjects like retirementplanning, investment strategies, or estate planning. Use clear communication that relates to each group of clients.

We have be behavioral finance tools so that the investor can understand their relationship with wealth and their risktolerance, their needs at a greater level of detail. But you would be surprised that merely saying to somebody, oh, we, we have you in a conservative portfolio based on your risktolerance and goals.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content