This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

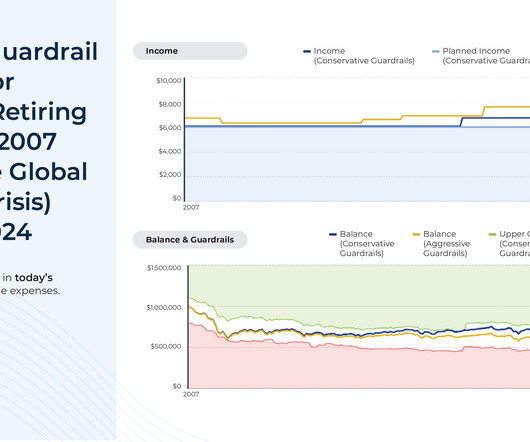

With this in mind, retirement income guardrails, which provide strategies that pre-determine when spending retirement adjustments would be made and the spending adjustments themselves – have become increasingly popular.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner.

Category: Clients Risk. When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. Good communication is the key to a successful advisor-client relationship.

Whether you’re a senior advisor looking to move into a CEO role, managing the burnout that comes from decades of client reviews, or preparing for retirement, having a well-defined system in place ensures that clients remain well-served and your firm operates efficiently. But, please note, youre not going to use this verbatim.

Planning for college Taking a gap year Relocating to another state or country Retirement income planning And so much more In embracing the Garrett Planning Network model, clients gain not just financial advice, but a partnership built on trust, transparency, and a commitment to their financial well-being.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

By using your expertise to communicate, educate, and provide perspective, you’ll likely magnify the loyalty of your clients. Use Continuous Communication Be proactive in your outreach to clients rather than waiting for them to call you. Here are some important steps to follow.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

As you enter your 50s, the urgency of retirement savings becomes palpable. For those who find themselves behind on their retirement savings, the path ahead may seem daunting. However, despite the challenges, there are strategies to catch up on your retirement savings.

Related posts about money questions for couples Communicate effectively with these important questions for couples about money! Learning how to communicate with your partner about finances is an adventure and it’s also very important, so let’s get into the top financial questions couples should discuss.

Service Company Dividend Yield Utilities Duke Energy 4% Communications AT&T 5.68% Groceries Kroger 1.44% Gas Exxon Mobil 4.01% Internet Comcast 2.3% Risk level : Varies. A Roth IRA is a type of investment account that lets you invest after-tax dollars for retirement. Fast Food McDonald’s 2.2%.

Are you saving for retirement, a home, or another goal? Understand your risktolerance Assess your age, income, and goals to determine your risk appetite. Longer time horizons allow for greater risk, while short-term needs may require a more conservative approach with more stable returns.

Saving monthly for retirement can create meaningful assets to help boost any shortfalls. Financial planners study and practice cash flow planning, credit planning, saving for a big purchase, retirement planning, estate planning, wealth management and insurance techniques. What Is Financial Planning? What Are Fiduciary Advisors?

Retirement planning. Financial advisors also spend years developing strong listening and communication skills to help you talk through your goals, uncover hidden risks and plot a course to work towards success. Saving monthly for retirement can create meaningful assets to help boost any shortfalls. Credit planning.

In case of any doubt or discrepancies, it is vital to communicate with your financial advisor openly. Communication is key in the evaluation of investment performance. Communication is key in the evaluation of investment performance. Transparent communication is paramount in risk management.

Investment advisors analyze market trends, assess the client’s economic situation, and develop personalized investment strategies tailored to their goals and risktolerance. Investment advisors can also specialize in specific areas such as retirement planning, tax planning, or portfolio management.

A financial advisor possesses a deep understanding of complex financial concepts and can help you navigate the intricacies of investing, retirement planning, debt management, estate planning, succession planning, tax optimization, and more. Make a note of their communication skills and interest in the conversation.

Wealth managers work closely with their clients to understand their unique financial situations, risktolerance, and investment goals to develop customized solutions that meet their needs. It is a holistic approach that focuses on the integration of various financial services to help clients achieve their goals.

Assess your risktolerance: Cryptocurrencies are known for their volatility, with prices that can fluctuate significantly in a short period. Avoid relying solely on crypto for critical financial goals like retirement. When investing in cryptocurrencies, securing your assets is crucial due to the risks of theft and hacking.

But this strategy can also be used outside of retirement savings accounts like mutual funds or ETFs. . This style of investing carries more risk and is better suited to investors with a high-risktolerance and a long investment time horizon. . Value stocks tend to be more cost-effective and have less risk attached.

Want to retire early? A financial plan can define your current savings plan, investment allocations, risk profile, desired lifestyle, projected expenses, and more to achieve that goal. You can accomplish this task in several ways like strategic charitable giving, maxing out your retirement accounts, tax-loss harvesting, and more.

Crafting a Comprehensive Financial Plan: This includes a detailed net worth statement, defining SMART Goals including retirement, children education etc., and a risktolerance analysis, all of which are sculpted around an individual’s circumstances. They are dynamic, evolving with the flow of life.

This includes articulating a policy with regard to investment risktolerance, long-term goals, cash flow needs and sector diversification. It also encompasses intended lifestyle, charitable giving, retirement and estate planning, and liabilities, including anticipated costs for health care.

BITTERLY MICHELL: And so, you start to learn things like, well, so how do you say call option, how do you say puts — so as I was like chatting with different people or communicating with different people on — on Bloomberg, let’s say, I would then, you know, put — what are they saying? RITHOLTZ: Right. RITHOLTZ: Sure.

To succeed as a financial advisor your focus should be more than just finance, investing, and a retirement plan. Your early interactions must include more than just fact-finding or standard risktolerance questionnaires, or formal information exchange. Ask them about their plans for retirement and how they envision spending it.

This especially becomes true in the distribution phase of your retirement when you are relying on your portfolio to provide income. I had many clients that began to feel the pinch of rising costs after they retired. If you are retired or close to retirement, inflation can erode the value of your savings. Warren Buffett.

There are 11 sectors in the S&P 500 , ranked below by the percentage of the index represented by each: Information Technology (26.4%) Health Care (15.1%) Consumer Discretionary (11.7%) Financials (11.0%) Communication Services (8.1%) Industrials (7.9%) Consumer Staples (6.9%) Energy (4.5%) Utilities (3.1%) Real Estate (2.8%) Materials (2.5%).

Most advisors that work with commission-based income will need an individual retirement account (IRA). Whether you’re starting a new business, buying a home, or saving for retirement, you need expert advice to succeed. A well-defined value proposition helps you: Communicate more effectively. Keep promises to your clients and.

You can learn about the stock market, bonds, budgeting, retirement planning, and saving. How does communication work? If you have strong opinions on the impact of your investments, then make sure you choose a financial advisor who aligns with your values and understands your risktolerance or how risk averse you are.

You can learn about the stock market, bonds, budgeting, retirement planning, and saving. How does communication work? If you have strong opinions on the impact of your investments, then make sure you choose a financial advisor who aligns with your values and understands your risktolerance or how risk averse you are.

To define your target audience, consider things like age, income, investment goals, risktolerance, job, and lifestyle. These could include subjects like retirement planning, investment strategies, or estate planning. Use clear communication that relates to each group of clients. These personas are made-up profiles.

The last time we spoke, we really were talking about the retirement crisis, and we spent a little bit of time discussing Vanguard. So let’s have 70 be our retirement age. But everybody needs to save for retirement to pay for their kids’ college, to leave something to the next generation. It doesn’t apply to me.

So built in a retirement offering an insurance offering, expanded their mutual fund offering, expanded their ETF offering. We have be behavioral finance tools so that the investor can understand their relationship with wealth and their risktolerance, their needs at a greater level of detail. It was great.

I don’t know when to retire or claim Social Security. For him, DIY investors on path to retiring in 5 years How do I want to serve? Instead, he provides them with an analysis of their risktolerance and investment plan, and even specific tickers. Do I have enough to retire? What the heck is going on? In what order?

The New York Fed is kind of, I don’t know how to say this first, amongst the regional feds, because you’re located right in the heart of the financial community. What is the communication like back and forth between the New York Fed and major players in finance, especially in the midst of a crisis like that? Try, try that.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content