This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This month's edition kicks off with the news that custodial platform Altruist is eliminating the $1 per account monthly fee for its portfolio management and reporting technology for advisors on its platform, which on the one hand suggests that the economies of scale Altruist has achieved in the wake of its move to become a fully self-clearing custodian (..)

Going beyond FPA’s existing PlannerSearch tool, the narrowed-down list is meant to help consumers identify a focused subset of the most reputable planners.

By Mike Valenti, CPA, CFP ® , Director, TaxPlanning Corporate executives often receive the brunt of the U.S. tax system. Typically, most or all of their income is W-2 income and subject to the higher ordinary tax rates as well as FICA taxes. The spread is taxed as ordinary wage income, subject to FICA taxes.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Copyright 2022.

The ‘millionaires’ tax will also ensnare taxpayers who exceed the $1M limit after selling a home, business, stock options, or other types of one-time events. Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

SmartOffice — SmartOffice , the customer relationship managemen t s olution from Ebix, is a financial planning CRM that helps financial advisors tackle critical tasks like analysis, communication, and client services. . CRM systems make it easier to juggle tasks, opportunities, and communications.

Article is for informational purposes only and should not be misinterpreted as personalized advice of any kind or a recommendation for any specific financial or tax strategy. This is a general communication should not be used as the basis for making any type of tax, financial, legal, or investment decision.

Mike Valenti, CPA, CFP ® , Director of TaxPlanning Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner It’s January, so it’s officially tax season! One of the most common client questions heard by tax preparers is, “So, what do you need from me?” The short answer to that question is often, “Everything.”

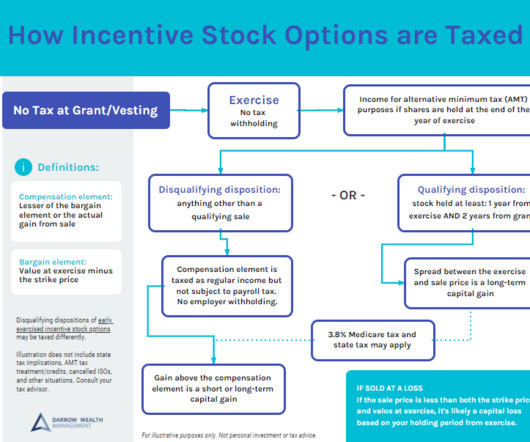

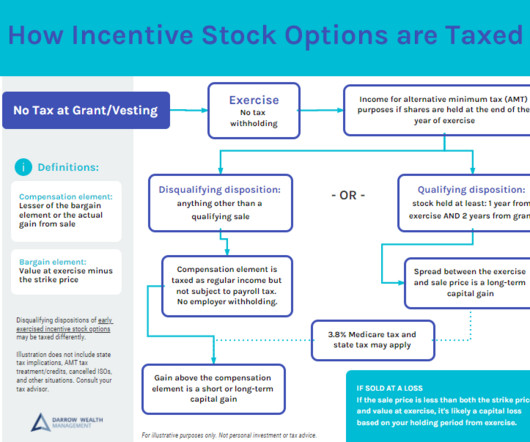

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. You’d have liquidity from the sale to pay any tax due in April. The cash crunch is quick to rain on a potential taxplanning parade.

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. You’d have liquidity from the sale to pay any tax due in April. The cash crunch is quick to rain on a potential taxplanning parade.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

Particularly for individuals who are holding a lot of cash or have proceeds from a windfall such as the sale of a business, a multi-year Roth conversion strategy is worth considering. Aside from the tax bill, you’ll want to have enough cash or resources to live on to minimize your taxable income in the year of conversion.

Core components of CAS involve bookkeeping, payroll, taxplanning & compliance services customized for each client. TaxPlanning and Compliance With any of the above components, taxplanning and compliance will be a major area of need, particularly for newer businesses.

Video: Qualified Small Business Stock (QSBS) Explained QSBS tax benefits: excluding capital gains taxes If you have Section 1202 shares, the gain you’re able to exclude from federal long term capital gains tax at sale depends on your gain and the date the stock was acquired.

The Challenge: Tax Firms and CPAs Struggle to Expand Client Relationships Today, there is a significant opportunity for tax practices and CPAs to expand and deepen their tax-client relationships by offering more valuable, long-term services, including comprehensive taxplanning.

and have reported more than $5 million in gross receipts or sales on their previous year’s tax return. This email address will be used for communication regarding the report. gross receipts/sales), and certain other regulated entities are typically exempt. Full name: Enter the submitter’s full legal name.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Understanding Financial Planning Marketing Financial planning marketing encompasses various strategies to attract clients to financial advisory services. This means identifying your target audience, crafting attention-grabbing messages, and using effective communication methods.

Article is for informational purposes only and should not be misinterpreted as personalized advice of any kind or a recommendation for any specific financial or tax strategy. This is a general communication should not be used as the basis for making any type of tax, financial, legal, or investment decision.

Running focused social media campaigns that highlight their services and share their skills in areas like taxplanning or retirement planning. They like communication that is tailored just for them. Pay attention to their special problems, such as preparing for the future, managing taxes better, and protecting wealth.

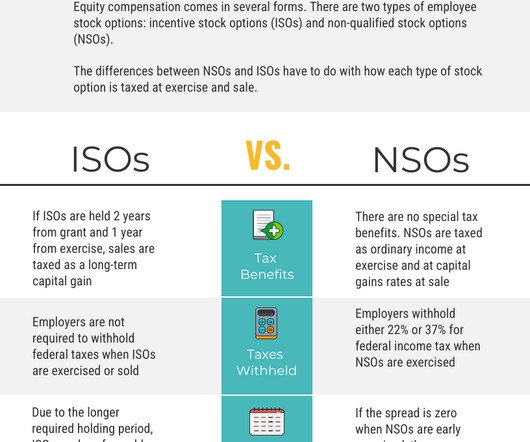

How stock options are taxed depends on the type of options you have and your sale and exercise strategy. In most cases, incentive stock options receive more favorable tax treatment compared to non-qualified stock options. Here’s a primer on how employee stock options are taxed at exercise and sale.

A deep discussion of these strategies is outside the scope of this overview, and because every situation is so different, be sure to discuss your situation with your tax and financial advisor. Again, every situation is different, so be sure to discuss your situation with your tax and financial advisor. holding period of over one year).

presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics. Since last year’s U.S. Those conditions do not exist today.

Investment advisors can also specialize in specific areas such as retirement planning, taxplanning, or portfolio management. Their tasks include regularly reviewing the credit histories of existing and potential customers to assess their creditworthiness and ensure their contributions to the company’s sales.

People my age, who I grew up with in the business, the one-time rebels in the financial services community who bravely, boldly created the planning profession out of a dysfunctional sales culture, have gradually become obstacles to change in their own firms.

If you own a stake (or plan to invest) in a startup or small business, you need to know about an important taxplanning tool available to you. If you qualify, you may be able to avoid federal taxes on any and all capital gains you realize when you exit.

If you own a stake (or plan to invest) in a startup or small business, you need to know about an important taxplanning tool available to you. If you qualify, you may be able to avoid federal taxes on any and all capital gains you realize when you exit.

Indexed universal life (IUL) is often sold using smoke-and-mirrors sales shams, but in this podcast we’ll expose the truth! Listen to this if you are a financial advisors or consumer who wants to see through the crap and make better decisions about whether IUL is good for you (or your client) or NOT. And that would be a huge problem.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. And it’s just all hourly, there’s no way you win there at all, no product sales. Hourly financial advisors are not common. Jon Luskin.

So there’s the, “Hey, I’ll work with you and we’ll develop goals and a plan how to get there.” They’ll do taxplanning, right? We’ll do estate planning and other complex financial planning. So Jack hates ETFs, doesn’t like advisors, and he hates sales.

Now, there was one really important part of, of that as part of my job training, I was sent to the big sales offices to learn how the product was sold. One of the big sales offices was out in Long Island in Garden City. She left there, she became a crisis communications expert. She also knew Washington in and out.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content