This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Notably, while many financial coaches satisfy the majority of these requirements – they are in the business of offering advice to clients and are compensated as such – they often steer clear of making specific securities recommendations, focusing instead on areas like budgeting, debtmanagement, savings, and retirementplanning.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

By taking a holistic approach to financial planning, you can help your clients manage their debt effectively and work toward building financial security. Here are three things financial professionals can do to help their clients deal with debtmanagement: 1.

The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years. Retirementplanning is not just about reaching a target savings number.

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. To secure a stable financial future, you must address outstanding debts before retiring.

Debtmanagement: Develop a strategy to pay off existing debts efficiently, minimizing interest costs. Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts. Emergency fund: Establish and maintain an emergency fund to cover unexpected expenses.

Based on the 2022 Workplace Wellness Survey , published in the Employee Benefit Research Institute (EBRI) journal, younger employees prioritize professional development opportunities, while older employees value retirementplanning more. Retirement benefits are a key component of a benefits package that attracts and retains top talent.

However, in some cases, you may need to sign up for a DebtManagement Program (DMP), which will usually have a cost. You can get basic budget counseling at their various agencies as well as debtmanagementplans. They can help connect you to a member agency that will offer debt relief solutions.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Intermediate and short-term goals may include saving for a vacation, buying a home, paying off debts or funding your child’s education. RetirementPlanningRetirementplanning is a primary focus for many clients.

Saving is an integral part of budgeting, as it allows individuals to build emergency funds, plan for future expenses, and achieve long-term financial objectives. RetirementplanningRetirementplanning involves setting financial goals for one’s golden years and devising strategies to achieve them.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Intermediate and short-term goals may include saving for a vacation, buying a home, paying off debts or funding your child’s education. RetirementPlanningRetirementplanning is a primary focus for many clients.

Retirementplanning is a must, so start with maximizing your 401k and Individual Retirement Accounts (IRAs). They can also help with debtmanagement, retirementplanning, estate planning, and more. Financial planning for dual-income families is not all that complicated. To conclude.

A reputable financial advisor should provide a comprehensive range of services, including budgeting, debtmanagement, insurance optimization, tax planning, retirementplanning, estate planning, and investment management.

If you’re under significant debt pressure, consider talking with a Certified Financial Planner Professional or an Accredited Financial Counselor who specializes in consumer credit and debtmanagement. . If you find yourself under pressure to meet these guidelines, take advantage of any employer retirementplan matches.

Now is when you should be more focused on managingdebt and planning for – not just looking toward – the future. Debtmanagement: In your 30s it’s important you managedebt obligations carefully. Planning in Your 50s Your 50s mark the beginning for retirementplanning – yes, already!

At the end of the course, you will gain knowledge on personal finance, budgeting, debtmanagementplans and retirementplanning. Also, it helps you understand how to implement strategies to meet your financial goals. You can enroll in the course here.

A critical aspect of advising clients is to ascertain their financial goals correctly. If you or your clients don't genuinely understand the goal, your advice could be dangerously off base, and you could lose your client's confidence.

Hiring a financial advisor can provide several benefits that are essential for managing your financial well-being. They can create a comprehensive financial plan tailored to your specific needs and goals. In addition to their financial expertise, a financial advisor can also address your emotional needs.

Not prioritizing debtmanagementDebtmanagement is another reason why financial planning for physicians is necessary. In most cases, healthcare professionals have a lot of unpaid debt. Remember to start planning for your retirement immediately, regardless of the age you start earning.

Pay off debt. When you create a financial plan, be sure it includes a debtmanagement system and how you'll pay off debt. Sadly, you can't really kick-start your financial future if you're carrying a ton of debt. Plan for taxes. Yup, taxes!

These professionals also hold expertise in various fields, such as retirementplanning, tax management, estate planning, investment management, insurance, debtmanagement, wealth management, and more. They help prepare a retirementplan based on a client’s financial needs and goals.

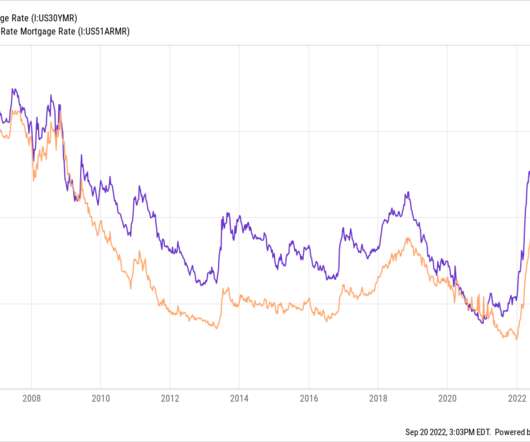

Is retiring with a mortgage a good idea? Most individuals will jump through hoops to live mortgage-free, regardless of whether it makes the most sense financially. Sure, all else equal, it’s always better to reduce your expenses.

You can also consolidate high-interest debt into a lower-interest loan or use balance transfers to streamline your repayment efforts and reduce overall interest costs. Additionally, you can consider consulting with a financial advisor or credit counselor to explore debtmanagement strategies tailored to your unique situation.

This plan may cover estate and retirementplanning, college savings, debtmanagement, and more. Tax Planning: Financial advisors can help manage your tax liability, advising on strategies to minimize capital gains taxes, maximizing tax-efficient investments in retirement accounts, and charitable giving.

Due to the complex and diverse range of their financial assets, these individuals also require specialized high-net-worth financial planners and personalized investment management tailored to meet their specific needs. 2023 may see several changes with respect to retirementplans, Social Security, etc.,

The simplest definition of the role of a financial advisor would of that of a person who helps individuals, families, and organizations make decisions related to their investments, taxes, insurance planning, retirementplanning, estate planning, and money management. Wealth Management Firms. Brokerage Firms.

Pay off debt When you make your money plan, be sure it includes a debtmanagement system and a plan for paying off debt. Sadly, you can’t really kick-start your financial future if you’re carrying a ton of debt. Am I on track with my savings for my children, including 529 plans ?

Opening Individual Retirement Accounts (IRAs) and managing your 401(k). Retirementplanning, estate planning, tax planning. Insurance planning and debtmanagement. How to make the most of veteran and other public benefits. Developing a diversified investment portfolio.

Financial advisors play a pivotal role in helping clients navigate a spectrum of financial matters, from budgeting and investments to healthcare and retirementplanning. Financial advisors offer a range of services, including investment management, financial planning, tax planning, debtmanagement, and ongoing advice.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content