This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ATM: Valuation is an exercise in faith with Aswath Damodaran. Full transcript below. ~~~ About this week’s guest: Professor Aswath Damodaran of NYU Stern School of Business is known as the Dean of Valuation. . ~~~ About this week’s guest: Professor Aswath Damodaran of NYU Stern School of Business is known as the Dean of Valuation.

To find out more, I speak with Jeremy Schwartz, Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Dividends come from earnings, and so those are sort of anchors to valuation.

And on today’s edition of At the Money, we’re going to discuss how you can participate in shareholder yield and get more out of dividends to help us unpack all of this and what it means for your portfolio. Because of the valuation gap looks about the best it’s ever looked, uh, over the past decade.

We’re currently seeing one of the largest disparities in valuations between growth and value stocks which in our opinion presents a very appealing opportunity for dividend seeking investors. While everyone is bantering about the official definitions of what a recession is, we’re very likely to see a period of stagflation.

. ~~~ About Jeremy Schwartz: Jeremy Schwartz is Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies, and multi-asset Model Portfolios. But when you buy a broad market portfolio, You’re getting that diversification.

Full transcript below. ~~~ About this week’s guest: Professor Aswath Damodaran of NYU Stern School of Business is known as the Dean of Valuation. These describe those must-own, “Set & Forget” companies that absolutely have to be in your portfolio if you want to keep up. He has written numerous books on valuation and finance.

Both these growth stocks and value stocks are considered very important while building your stock portfolio. Many times, while picking stocks you might have wondered why people are buying the stocks which are trading at a high valuation whereas conceptually most intelligent investors are looking for a low valuation and lower PE.

From checking the real-time streaming market price of the stock, making a virtual portfolio, drawing stock charts, following market trends to tracking your portfolio; everything is now accessible from your smartphone or tablet. Key Features: Ease of Use : Easy navigation to all financial data, portfolio, watchlist and message board.

We do discretionary macro trading, which is typically a portfolio manager — and we have some number of portfolio managers, 15 or 18 different portfolio managers that independently manage a book of, you know, risk assets. Definitely. Well, as you sort of referenced, we do a lot of different trading styles at Graham.

And definitely, their retail market participation is significantly lower than you can see in the U.S. But I think it’s definitely changing, Barry, because, you know, you see more and more fintech platforms and robo-advisors that in a way, are making accessing financial markets easier for more and more investors in in Spain.

Overall, this is definitely one of the best value investing books and for serious investors- this is a must-read. Hagstrom describes the necessary aspects to achieve similar success like Buffett that you can apply immediately to your own portfolio. It was originally written in 1991 and definitely contains many time-tested principles.

If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Dick Mayo was a traditional, I’d say portfolio, strong portfolio manager focused on US stocks. He’s a big picture guy.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years.

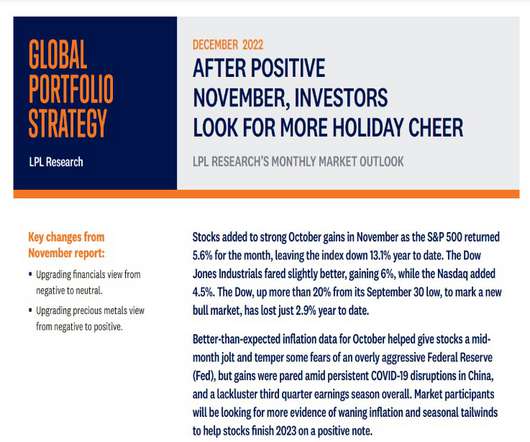

The economy has decelerated sharply in the last year, but we aren’t seeing data that is consistent with what the NBER would define as a “recession” So how concerned should we be about these technical definitions? In our view we’re still in the “muddle through” camp as it pertains to the economy.

All of their portfolio managers not only are substantial investors in each of their funds, but they do a disclosure year that shows each manager by name and how much money they have invested in their own fund. 00:10:10 [Speaker Changed] I mean, the, the deal was definitely done in Japan and Australia, not in the us right?

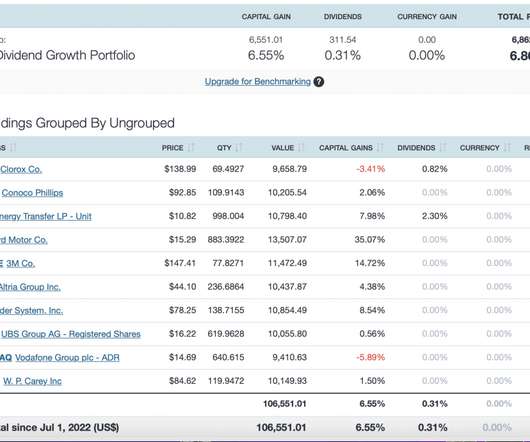

S&P returns (including dividends) since 2019, graph by the excellent portfolio visualizer website. Which makes the landlord business a lot less profitable, and we should expect exactly the same thing as stock investor: lower future profits as a percentage of our portfolio value. And it has more than doubled in the past five.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years. All index data from FactSet.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years. All index data from FactSet.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. It is also a major component used to calculate the price-toearnings valuation ratio. It is expressed as a number of years. All index data from FactSet.

At the time, those funds were having success because of Hussman's generally defensive portfolio posture. The funds might play a role in a diversified portfolio but hard to peg either one as a single portfolio solution. The idea of a single fund, all-weather portfolio is intellectually appealing even if it probably doesn't exist.

The transcript from this week’s, MiB: Antti Ilmanen, Co-Head, Portfolio Solutions, AQR , is below. BARRY RITHOLTZ; HOST; MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Antti Ilmanen is AQR’s Co-head of the Portfolio Solutions Group. CO-HEAD, AQR’S PORTFOLIO SOLUTIONS GROUP: Thanks, Barry.

While there’s no universally accepted definition, we can outline some general characteristics and criteria: Extreme Valuations : Prices are significantly higher than can be justified by fundamental analysis. Disregard for Valuation Models : The marginal buyer doesn’t care about traditional valuation methods.

A Solid Foundation: The Value of Private Real Estate in Balanced Portfolios. We believe that focusing solely on current market conditions ignores the true, long-term value that private real estate investments can add to a portfolio. Low correlation means that real estate helps to diversify balanced portfolios.

Had you invested every two weeks in a 60/40 portfolio, hard as it is to make sense of, you would be at an all-time high today. For example, I'm "conveniently" leaving out valuations. Or the fact that nobody actually holds this portfolio. It's true that it didn't have to turn out this way, and I definitely did not think it would.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. they definitely did that. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector. BARATTA: Yeah. In the long run. BARATTA: Well.,

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

Definitely not! Depending upon your risk appetite and market levels, you should accordingly maintain equity exposure in your portfolio. You can choose to invest in equity in the range of 30-80% of your overall portfolio and remaining in Debt (FDs, Debt Mutual Funds, Bonds, etc.) Is it wrong to keep money in FDs?

Balancing Act | For Good Measure: How We Value Global Leaders achen Wed, 04/18/2018 - 11:03 Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio.

Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio. This makes ratios like the P/E ratio dangerous as a valuation tool. Wed, 04/18/2018 - 11:03.

And, and definitely more emphasis on the, the types of investments the fund is, is making. , Barry Ritholtz: Michael Carmen: 00:05:59 [Speaker Changed] So you started out investing directly in the public markets, small cap, mid cap, various styles. Post money valuations until the market has changed dramatically. That are all gone.

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

However, alongside these positive fundamental trends we also see potential causes for concern—valuation risk, to be sure, but also macroeconomic and geopolitical risks. As always, we want to avoid skewing portfolios toward a specific market scenario, because we can’t accurately predict which scenario will come to pass.

While there is no single universally accepted definition, most quality-focused investors look at factors such as: The Definition of Quality Return on Invested Capital (ROIC): This measures how efficiently a company generates returns on the capital it deploys. So what exactly constitutes a “high quality” company?

In many clients’ portfolios we have eliminated our overweight position in U.S. equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations. Impact on U.S. Impact on U.S.

Large-Cap Sustainable Growth Strategy: Reporting on the impact of our investment decisions 2022 ajackson Wed, 04/12/2023 - 09:56 A Letter of Introduction From The Portfolio Managers Since launching this strategy more than 13 years ago, the demand for information on ESG, impact, and sustainability has risen dramatically.

2022 Impact Report: Large-Cap Sustainable Growth Strategy ajackson Wed, 04/12/2023 - 09:56 A Letter of Introduction From The Portfolio Managers Since launching this strategy more than 13 years ago, the demand for information on ESG, impact, and sustainability has risen dramatically. and Brown Advisory Trust Company of Delaware, LLC.

This is achieved by investing in a concentrated portfolio of companies that, according to our analysis, generate durable levels of free cash flow, exhibit capital discipline and have attractive valuations. We do not take an exclusionary approach at Brown Advisory andinstead build portfolios from the bottom up. Source: FactSet.

Tell us a little bit about the giant portfolio of companies you guys are managing. So we manage a portfolio of several dozen companies. When you add together all of our portfolio companies, it’s effectively $100 billion enterprise — RITHOLTZ: Wow. You sit on the board of directors on a number of portfolio companies.

As we discuss in this article, we believe that credit naturally plays a complementary role with equities in portfolios, and that this pairing can be particularly fruitful during cyclical downturns. In some situations, we may be looking to bolster portfolio stability to counteract potential macro or sector-specific headwinds.

As we discuss in this article, we believe that credit naturally plays a complementary role with equities in portfolios, and that this pairing can be particularly fruitful during cyclical downturns. In some situations, we may be looking to bolster portfolio stability to counteract potential macro or sector-specific headwinds.

We can divide that up into three key pieces that make overall returns: Earnings growth has contributed 57%-points Dividends contributed 14%-points Valuation multiple growth contributed 21%-points In other words, most of the returns have come from profits (and dividends). away from being rounded down to 4.0%.

From an investment perspective, the global government policies underway to reduce emissions and promote healthy communities are ones that simply should not be ignored in your wealth-building portfolios. Investing in clean energy can be beneficial, not only for the environment but also for your financial portfolio. compared to 97.2%.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content