This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that the latest Fidelity RIA Benchmarking Study shows that while RIAs saw gains in AUM and revenue last year, their operating margins tightened, suggesting that rising expenses are cutting into firm profits.

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that CFP Board announced that it has crossed the milestone of 100,000 CFP professionals in the United States, and despite having just celebrated its 50th anniversary last year, just set a record high in the number of advisors sitting (..)

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that the Federal Trade Commission has proposed a nationwide ban on noncompete clauses in employee contracts, aiming to give employees more freedom to change jobs within the same industry.

Enjoy the current installment of "Weekend Reading For FinancialPlanners" – this week's edition kicks off with the news that Charles Schwab and other brokerage platforms are planning to increase the interest rates they pay on client cash held in their platform or cash sweep programs, which could boost the income of clients who maintain a cash (..)

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that Congress appears poised to pass “SECURE Act 2.0”, ”, a series of measures that will have significant impacts on the world of retirement planning.

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that AdvisorTech giant Envestnet has announced a partnership with New Zealand-based FNZ that will allow Envestnet to offer custodial services to advisors beginning in the second half of 2023.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirement plans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

Which suggests that while firms might be tempted to zero in on compensation when it comes to retaining advisors, focusing on these other factors (which do not necessarily involve hard dollar expenses) could pay off in the form of increased advisor (and client) retention over time.

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. An HSA can serve as an additional retirement savings vehicle on top of your IRA or 401(k) to help cover healthcare and other retirement expenses. Click To Tweet.

Qualified retirement plans – such as 401(k)s, 403(b)s and IRAs – offer clear tax advantages. Traditional 401(k)s, 403(b)s, and IRAs offer a tax deferral on contributions and growth until distribution. One of those is the Required Minimum Distribution (RMD) rule. Jamie Hopkins, Managing Partner, Wealth Solutions. RMD Basics.

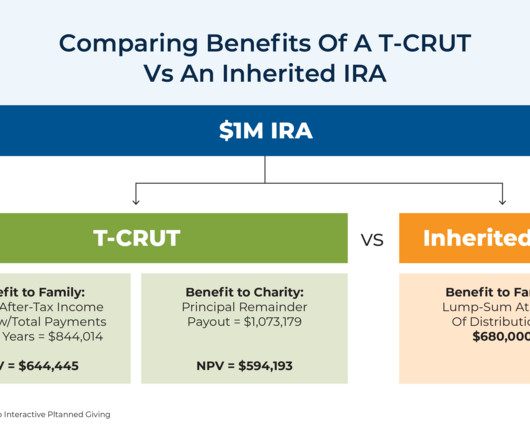

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. Of the many provisions in the bill, the so-called "Death of the Stretch" arguably received the lion's share of consternation from the financial advisor community.

In today’s world of early or semi-retirement, many people wonder when they should begin taking their Social Security benefits. Full retirement age. Your full retirement age or FRA is the age at which you become eligible for a full, unreduced retirement benefit. FINANCIAL WRITING. This increases to $19,560 for 2022.

Approaching retirement and want another opinion on where you stand? Check out my Financial Review/Second Opinion for Individuals service for more detailed advice about your situation. Financial coaching focuses on providing education and mentoring on the financial transition to retirement. FINANCIAL WRITING.

Key among them are the options to roll over the account into their own IRA, keep it as an inherited IRA, or consider varying stances based on the decedents Required Minimum Distributions (RMDs). Unlike non-eligible beneficiaries who are limited to a strict ten-year distribution period, EDBs can choose from various withdrawal schedules.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. When aiming for financial independence, the importance of a structured approach should be emphasized. Within this framework, the concept of the five pillars of retirement planning emerges as a valuable strategy.

FINANCIAL PLANNING 4 Areas Your FinancialPlanner Should Cover as a High-Net-Worth Individual Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Given the complex nature of their portfolios, HNWIs require assistance from experienced financialplanners who understand their unique situations and needs.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirement planning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

Retirement Planning 5 Ways to Catch Up on Retirement Planning Later in Life Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirement is a significant investment, which is why so many financial experts recommend establishing goals and starting when still a younger adult.

Thinking about converting your retirement account to a Roth IRA? Roth IRAs don’t come with Required Minimum Distributions (RMDs) at age 72 like a traditional IRA either, so you can continue letting your money grow until you’re ready to access it. You don’t want to begin taking distributions at age 72.

Note: Make sure that any non-retirement assets are titled in the name of the trust in order for them to be valid. They’ll help close your accounts, file your will and distribute your assets the way you’ve specified. The trustee is responsible for acting as the legal owner of the trust and handles managing and distributing the assets.

RETIREMENT PLANNING The Four Phases of Retirement Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirement planning has become increasingly difficult as the cost of living continues to rise. To help you better prepare for the future, discover the four phases of retirement below. Pre-Retirement.

Can women retire successfully if they were to invest in gender equity? If you’ve read any of my articles on values based financial planning and investing, you will read that I believe that everyone should build a financial plan aligned with their values. Here’s to your gender equality-powered retirement!

Secure Your Financial Legacy When planning for your legacy, it’s important to consider various financial aspects. Here are some additional details and keywords to help guide you: Estate planning involves creating a plan for the management and distribution of assets after death.

Distributing tax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability . Increasing tax-deferred savings, such as an employer-sponsored retirement plan, to lower your taxable income . Long gone are the days when individuals relied on interest from investments to fund their retirement.

You may have recently changed jobs and are wondering, “What should I do with my retirement account that was established through my former employer’s retirement plan?” It is a defined-contribution plan that offers an opportunity for an employee to save and invest for retirement in a tax-deferred manner. However, it is an option.

This blog post explains why financial planning is important and how it can benefit you in the future Understanding the Importance of Financial Planning: Financial planning involves setting financial goals, creating a budget, saving and investing managing debt, and planning for retirement and estate.

O ne of my most favorite questions that I often get as a financialplanner is “What’s your best rates on Roth IRA’s ?” Whenever I get that question, I typically start by explaining what an I-R-A stands for: Individual Retirement Arrangement (emphasis on arrangement). Rate subject to change.)

You may have recently changed jobs and are wondering, “What should I do with my retirement account that was established through my former employer’s retirement plan?”. It is a defined-contribution plan that offers an opportunity for an employee to save and invest for retirement in a tax-deferred manner. Cash it out. Do nothing.

Your financial planning needs get more complex than in your 20s. The following are into five areas of focus for retirement saving in your 30s. . Talk with a qualified financialplanner to ensure you have appropriate coverage to protect your family, assets and legacy if the unthinkable were to happen. . .

As we bid adieu to this year, it’s a golden opportunity for savvy investors and retirementplanners to give their strategies a once-over, particularly when it comes to Roth IRA conversions. No RMDs: Roth IRAs don’t hassle you with required minimum distributions, letting your money grow peacefully for longer.

Use a qualified charitable distribution (QCD) from your individual retirement account (IRA). If you are age 70 ½ or older, you can transfer money from your IRA to a charity as a qualified charitable distribution (QCD), which makes it tax-free up to $100,000 ($200,000 if you file jointly).

The rules surrounding Individual Retirement Accounts (IRAs) undergo frequent and impactful changes. While IRAs are a cornerstone for many retirement plans, these accounts being inherited adds a layer of complexity to them. A professional can help guide you through the complex maze of retirement account regulations.

Additionally, the government has made changes to tax rules, further prompting Americans to reevaluate their tax and financial strategies. Retirement Savings Accounts . In 2023, Internal Revenue Service (IRS) will increase the contribution limit for multiple types of retirement accounts, including: . 0 Comments. 0 Comments.

Roth IRAs certainly have advantages, such as no required minimum distributions, and beneficiaries will receive the Roth IRA tax-free. There may be new tax legislation that could change the way we plan for retirement assets. There are proposals to change the deduction for retirement plan contributions, making Roths much more valuable.

Their primary objective is to ensure that the assets are managed & distributed according to the wishes of the client. The FinancialPlanner will ensure that the Estate Planning strategy is curated in terms of client requirements, estate complexity and requirements of the legal heirs /other parties.

And as you think about retirement and long-term goals, they feel more tangible than they did twenty years ago. Consider the following five steps to take planning for retirement in your 40s: . Maximize Your Retirement Plan Savings . Ellie’s employer will match any 401(k) retirement contributions up to 4% of her salary.

Take Advantage of Retirement Plans and Matching Contributions. Most employer retirement plans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Work With a Financial Advisor . Consider the following example below:?? .

Investing your money is crucial to securing your financial future and achieving your goals. Whether saving for retirement, buying a home, or building an emergency fund, investing grows your wealth over time. Just as a diverse garden thrives, a well-allocated portfolio grows robustly, securing your financial future.

Estate planning touches two critical aspects of our lives: It can direct the distribution of property while providing a structure of guardianship and care for ourselves as well as those we love and care for. You should think about property distribution as you accumulate wealth. Craig Lemoine, Ph.D., When Do You Need an Estate Plan?

Anyone with dependents, retirement accounts, life insurance or real property. A beneficiary is the person or entity who receives the death benefit of an insurance policy, or retirement account proceeds at the death of an insured or account owner. Who needs estate planning? Estate Planning in Your 20s .

Trusts involve moving financial resources to a third party called the trustee. Trustees manage the funds wisely and ensure they are distributed to the beneficiaries, according to the grantor’s wishes. With a CRUT, you create a trust that provides annual distributions to you or certain beneficiaries for a set period. 0 Comments.

However, those contributions grow tax-free and qualified distributions remain tax-free. This could be incredibly helpful in retirement if you’re trying to stay in a low tax bracket and can pull funds from this tax bucket. Plus, Roth IRAs are the only account that doesn’t have required minimum distributions (RMDs).

When you establish a trust, you’re creating a legally-binding plan that stipulates how your wealth will be distributed after your death. Beneficiary: This is the person or people who receive a distribution of assets from the trust after the grantor’s death. Decide How You Want to Distribute Your Wealth.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content