This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that CFP Board announced that it has crossed the milestone of 100,000 CFP professionals in the United States, and despite having just celebrated its 50th anniversary last year, just set a record high in the number of advisors sitting (..)

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that Congress appears poised to pass “SECURE Act 2.0”, ”, a series of measures that will have significant impacts on the world of retirementplanning.

Enjoy the current installment of “Weekend Reading For FinancialPlanners” - this week’s edition kicks off with the news that the Federal Trade Commission has proposed a nationwide ban on noncompete clauses in employee contracts, aiming to give employees more freedom to change jobs within the same industry.

From there, we have several articles on investment planning: While I Bonds have received significant attention during the past year, TIPS could be an attractive alternative for many client situations. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

HSAs are not subject to required minimum distributions , allowing the HSA to continue to grow tax-free. Your HSA can be another leg on the retirementplanning stool. Please contact me with any thoughts or suggestions about anything you’ve read here at The Chicago FinancialPlanner. Click To Tweet.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. Of the many provisions in the bill, the so-called "Death of the Stretch" arguably received the lion's share of consternation from the financial advisor community.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Withdrawals from tax-deferred retirement accounts are taxed as ordinary income.

Qualified retirementplans – such as 401(k)s, 403(b)s and IRAs – offer clear tax advantages. Traditional 401(k)s, 403(b)s, and IRAs offer a tax deferral on contributions and growth until distribution. One of those is the Required Minimum Distribution (RMD) rule. Jamie Hopkins, Managing Partner, Wealth Solutions.

Please contact me with any thoughts or suggestions about anything you’ve read here at The Chicago FinancialPlanner. Related Posts: Choosing A Financial Advisor? - Don’t miss any future posts, please subscribe via email. Photo credit: Wikipedia.

Check out my freelance financial writing services including my ghostwriting services for financial advisors. Please contact me with any thoughts or suggestions about anything you’ve read here at The Chicago FinancialPlanner. Related Posts: Managing Inflation in Retirement Is a $100,000 Per Year Retirement Doable?

FINANCIALPLANNING 4 Areas Your FinancialPlanner Should Cover as a High-Net-Worth Individual Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Given the complex nature of their portfolios, HNWIs require assistance from experienced financialplanners who understand their unique situations and needs.

RetirementPlanning 5 Ways to Catch Up on RetirementPlanning Later in Life Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirement is a significant investment, which is why so many financial experts recommend establishing goals and starting when still a younger adult.

Secure Your Financial Legacy When planning for your legacy, it’s important to consider various financial aspects. Here are some additional details and keywords to help guide you: Estate planning involves creating a plan for the management and distribution of assets after death.

You may have recently changed jobs and are wondering, “What should I do with my retirement account that was established through my former employer’s retirementplan?” Some 403(b) plans offer a Roth feature, as well. It will continue to stay invested in the mutual funds or the annuity contract within the 403(b) plan.

You may have recently changed jobs and are wondering, “What should I do with my retirement account that was established through my former employer’s retirementplan?”. Some 403(b) plans offer a Roth feature, as well. Roll” the 403(b) into your new employer’s retirementplan. Roll” the 403(b) into an IRA.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Work With a Financial Advisor .

Distributing tax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability . Increasing tax-deferred savings, such as an employer-sponsored retirementplan, to lower your taxable income . One of the most overlooked aspects of financialplanning is healthcare.

Discretionary expenses include money spent traveling, eating out, contributing to savings and retirementplans or occasional purchases and upgrades. Maximize Your RetirementPlan Savings . Employers often match a portion of this contribution to a retirementplan as an employer benefit.

No RMDs: Roth IRAs don’t hassle you with required minimum distributions, letting your money grow peacefully for longer. Tax Diversification: With funds in both traditional and Roth accounts, you’re better equipped to handle your tax situation in retirement, picking and choosing withdrawals based on your tax bracket.

Roth IRAs certainly have advantages, such as no required minimum distributions, and beneficiaries will receive the Roth IRA tax-free. There may be new tax legislation that could change the way we plan for retirement assets.

If you’re under significant debt pressure, consider talking with a Certified FinancialPlanner Professional or an Accredited Financial Counselor who specializes in consumer credit and debt management. . Building Up Retirement Assets . Reinforcing Positive Financial Behaviors .

Just as a diverse garden thrives, a well-allocated portfolio grows robustly, securing your financial future. By distributing your investments across different assets, you can take advantage of the divergent impact of prevalent market conditions on these assets. Financial advisors work alongside clients to create a retirement roadmap.

A beneficiary is the person or entity who receives the death benefit of an insurance policy, or retirement account proceeds at the death of an insured or account owner. Beneficiary designation transfers through life insurance policies or retirementplan assets often comprise the bulk of a younger person’s estate. .

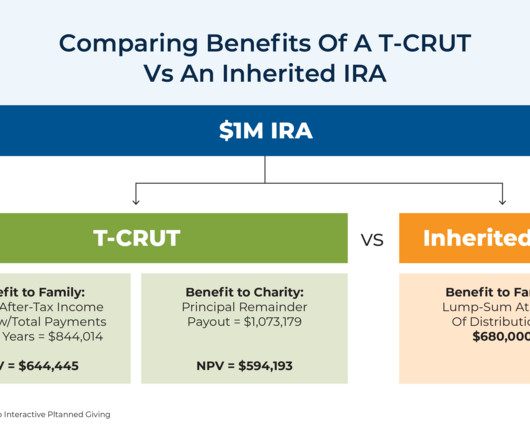

The rules surrounding Individual Retirement Accounts (IRAs) undergo frequent and impactful changes. While IRAs are a cornerstone for many retirementplans, these accounts being inherited adds a layer of complexity to them. You may plan a gradual withdrawal strategy that spaces out the distributions over the 10-year period.

Trusts can be highly beneficial for those engaged in estate planning. Trusts involve moving financial resources to a third party called the trustee. Trustees manage the funds wisely and ensure they are distributed to the beneficiaries, according to the grantor’s wishes. Attain Estate Planning Guidance at Park Place Financial .

Roth IRAs don’t come with Required Minimum Distributions (RMDs) at age 72 like a traditional IRA either, so you can continue letting your money grow until you’re ready to access it. When you do decide to take distributions from a Roth IRA, you won’t have to pay income taxes on that money. Not sure about your future tax brackets?

If you have an IRA, you will be able to take a distribution without the 10% penalty past age 59 ½. The conversion amount is considered ordinary income, meaning it incurs tax, but all future profits and distributions don’t get taxed — provided they fall within established limitations. . How to Choose a Personal Financial Advisor.

RETIREMENTPLANNING The Four Phases of Retirement Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirementplanning has become increasingly difficult as the cost of living continues to rise. What Factors Can Impact RetirementPlanning? Begin RetirementPlanning Today.

When you establish a trust, you’re creating a legally-binding plan that stipulates how your wealth will be distributed after your death. Beneficiary: This is the person or people who receive a distribution of assets from the trust after the grantor’s death. Decide How You Want to Distribute Your Wealth. 0 Comments.

Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Chartered Financial Analyst (CFA) CFAs are experts in investment management and analysis.

If you pass away without one, the state will be in charge of distributing the resources and, most likely, give them all to your children, which may have been your plan anyway. It is particularly valuable if the court finds your will invalid as it provides a guide for distributing your wealth to your family. 0 Comments.

However, those contributions grow tax-free and qualified distributions remain tax-free. This could be incredibly helpful in retirement if you’re trying to stay in a low tax bracket and can pull funds from this tax bucket. Plus, Roth IRAs are the only account that doesn’t have required minimum distributions (RMDs).

O ne of my most favorite questions that I often get as a financialplanner is “What’s your best rates on Roth IRA’s ?” By contributing to a Roth IRA with after-tax dollars, you can avoid paying taxes on distributions down the line. You don’t have to begin taking distributions at a certain age.

Some specific reasons you may want an estate plan include: . Family members or other loved ones depend on you for financial support. . You want to ensure your assets are distributed according to your wishes following your death or incapacity (also referred to as heritage wealth planning ). . 0 Comments. 0 Comments.

Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Chartered Financial Analyst (CFA) CFAs are experts in investment management and analysis.

Create a will A will is a legal document documenting how a person’s assets will be distributed after their demise. That said, laws pertaining to wills may vary from state to state and drafting a will may not guarantee that your assets are distributed according to your wishes. These are: 1.

This may be a good time to talk to a financialplanner so there’s no misunderstanding about how routine expenses will be divided. Plus, a life insurance payout can help equalize your estate if your new spouse is the beneficiary of your qualified retirementplan (which is required under federal law unless they sign a waiver).

Be it insuring your business, raising debt, lining up investors to invest their money, or managing equity, financialplanning in business is as essential as personal financialplanning. A well-tailored financialplan here becomes paramount. . Financialplanning tips for entrepreneurs.

The 401(k) retirementplan is one of the most powerful tools. Moreover, it facilitates financial discipline with consistency. Reaching the age of 50 with over $2 million in your 401(k) is an impressive financial landmark that can provide you with a comfortable retirement if managed wisely.

And that’s why I’m writing this blog; because I feel that financial advice rendered by the hour is a great thing for the American public (for the reasons we’re going to discuss below). But the idea of becoming an hourly financialplanner is met with such resistance you would think you told people to saw off their left arm.

Hiring reputable and experienced high-net-worth financialplanners can benefit high-income groups and help them lower taxes. Financialplanners employ different approaches to save tax. For instance, financialplanners may recommend turning your traditional retirement accounts into Roth accounts to lower your tax burden.

Enjoy the current installment of "Weekend Reading For FinancialPlanners" - this week's edition kicks off with the news that a recent survey indicates that 70% of affluent financial advisory clients who believe their advisor is always obligated to act as a fiduciary indicated they are satisfied with their relationship and aren't seeking out a new advisor, (..)

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content