This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

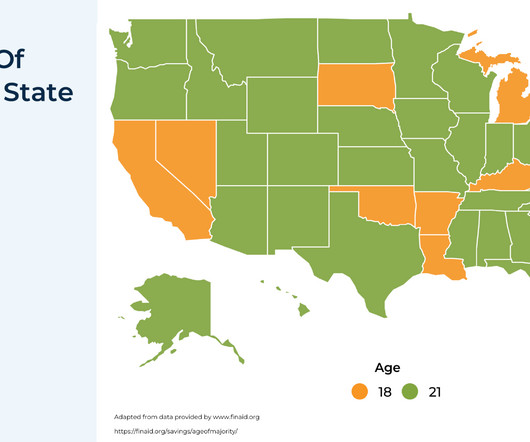

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estate planning purposes. 529 plans offer greater flexibility in ownership but restrict how funds can be used, particularly for educational expenses. Read More.

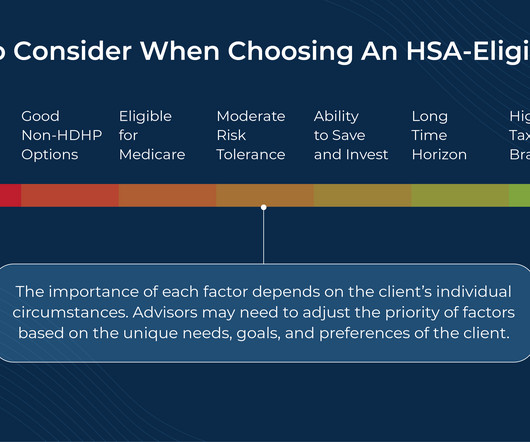

Health Savings Accounts (HSAs) have become an increasingly popular tool for financial advisors and their clients due in part to the 'triple tax savings' they offer: tax-deductible contributions, tax-free growth, and non-taxable distributions for qualifying expenses.

While many people approach their financial planning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. Lets explore several potentially effective financial planning tools that may help you maximize your impact and meet your philanthropic goals. government.

Accumulation-phase planning software won't cut it for solving your clients' complex retirement income puzzles, but there are dedicated applications that can.

advanced tax and estate planning) and ensure that both members of client couples remain engaged in the planning process (to encourage a surviving partner to stay with the firm in case of a death of their spouse) could have more durable client satisfaction and, ultimately, higher client retention rates.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

When thoughtfully drafted, it aligns the interests of the firm's owners, sets clear expectations for operations, and establishes how profits will be distributed. The next step is establishing a profit distribution philosophy. As a foundational document, the operating agreement is essential for RIA firms.

When thoughtfully drafted, it aligns the interests of the firm's owners, sets clear expectations for operations, and establishes how profits will be distributed. The next step is establishing a profit distribution philosophy. As a foundational document, the operating agreement is essential for RIA firms.

Consequently, when in estate planning, thinking about how to divide their assets after their death, they often aim to simply apportion the whole pot among their beneficiaries, without regard to the nature of each individual asset. Read More.

For advisors who recommend HSA-maximizing strategies, then, it’s important to consider the risks of the account owner being unable to use up their funds and to plan for potential ways to quickly draw down the account in the event the HSA owner will not outlive their HSA funds.

Apollo’s products for individual investors are distributed through intermediaries such as bank wealth channels and registered investment advisers, and the firm doesn’t expect that to change.

Financial advisors add value for their clients not only by helping them grow their wealth, but also by working with them to create a plan for how to use it. While much of this process may focus on the client's own lifetime planning needs (e.g., With this in mind, many financial advisors offer estate planning guidance to clients.

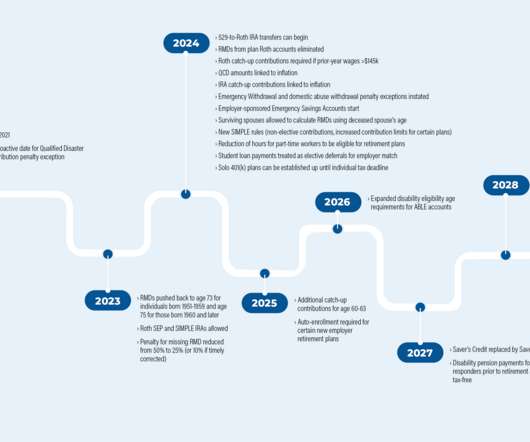

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

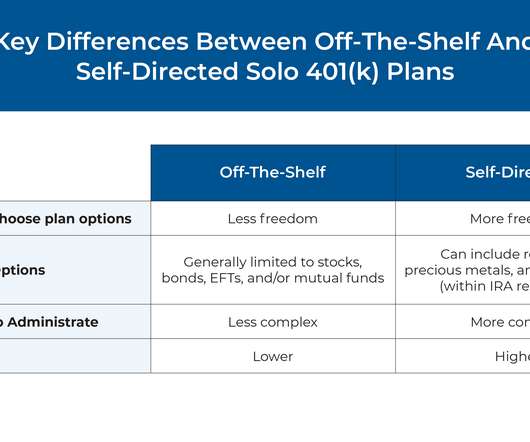

Among the several different types of retirement plans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. At the same time, adoption can be expensive, with costs that can add up to $70,000 or more.

Act regarding individual retirement accounts, including changing when the first required minimum distribution can be made from the account, new rules for inhe The panel of experts will discuss and answer questions about the changes made by SECURE 2.0

Hobby comes over from Fidelity Investments, where he served as the head of distribution for private wealth management, executive services, workplace planning and advice and stock plan services.

understand the value of qualified charitable distributions (QCD). Not only does this money count toward your required minimum distribution (RMD), but the donation is made tax-free, and the funds dont count toward your total taxable income. Note: This only applies to U.S.-based taxes.)

However, as the cost of equity rises and accessibility becomes more limited, firms face the challenge of inspiring ownership behavior without distributing equity.

The deductibility phase-out is based on filing status, income (MAGI), and whether or not the individual(s) are eligible to participate in a retirement plan at work. When you make a distribution, the original nondeductible IRA contribution amount isn’t included in your taxable income, but the earnings and growth from it is.

In this guest post, Michael Levin, a New York Times bestselling author and ghostwriter, writes about how financial advisors can make a more effective impression on prospective clients by writing, publishing, and distributing a book that establishes their authority, confidence, and, above all, trust.

Morgan Christiansen, VP of Distribution at The Pinnacle Group, explores the evolving role of insurance in financial planning at Nitrogen's 2024 Fearless Investing Summit.

Jeff is the Owner and Founder of Cypress Financial Planning, an independent RIA based in Haddon Heights, New Jersey, that oversees $275 million in assets under management for 380 client households. My guest on today's podcast is Jeff Jones.

This week, Orion announced they were making it easier for those in need of free financial planning to find help, TIFIN and Morningstar partnered to enhance their AI-powered distribution platform and eMoney responded to recently-passed legislation with tax planning upgrades.

Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . These types of plans are becoming more common with employers and are available privately as well. How the HSA works . Click To Tweet.

Qualified charitable distributions are made directly to the eligible charity from a traditional IRA, inherited IRA, inactive Simplified Employee Pension (SEP) plan and inactive Savings Incentive Match Plan for Employees (SIMPLE) IRAs. 2025 amounts should become available later this year.

morningstar.com) The biz Creative Planning was able to retain some 60% of the United Capital assets. riabiz.com) XY Planning Network is launching a new in-house RIA, XYPN Sapphire. obliviousinvestor.com) Estate planning Changing an estate plan takes time. wealthmanagement.com) Do your clients have a digital estate plan?

One Shein distribution center, located in Whitestown, Indiana, is already operational and could reduce shipping times by up to four days. It currently has 800 employees, with plans to have 1,000 by the end of this year. A second facility is expected to open in Southern California by the spring of 2023.

The role of estate planning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., The most common example involves trust provisions that direct assets to be distributed to beneficiaries once they obtain a certain age (e.g.,

The role of estate planning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., The most common example involves trust provisions that direct assets to be distributed to beneficiaries once they obtain a certain age (e.g.,

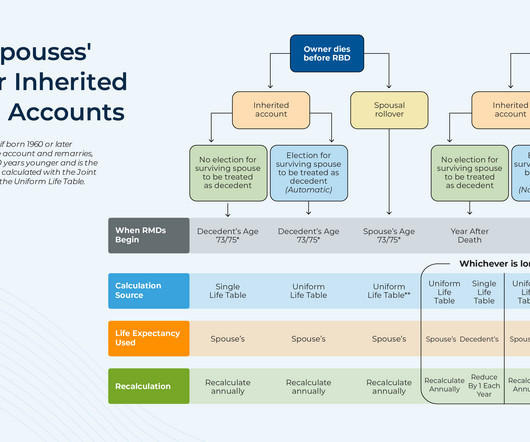

Among all the different types of retirement account beneficiaries, those who are the surviving spouse of the original account owner receive the most preferential tax treatment when it comes to distributing the account's assets after the owner's death. But the SECURE 2.0

kitces.com) Jamie Hopkins & Ana Trujillo Limón talk with Dave Yeske, CFP, founder and Managing Director of YeskeBuie about the role of emotions in financial planning. Podcasts Michael Kitces talks with Carl Richards about building a career in financial advice. wiredplanning.com) SECURE 2.0 A deep dive into SECURE Act 2.0

The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on planning than the changes to the post-death distribution rules for retirement accounts. being passed so late in the year.

Like gardening or working out, tax planning is one of those activities where you get out what you put in. Tax planning is similar in the sense that you can put work in on the front end that youll reap benefits from later. This initial question may help you put together the rest of your tax planning strategies.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirement planning, the same questions often arise: What should my retirement plan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirement plan. Looking for personalized retirement planning advice?

Your personal preferences and the potential good your bequests can do are factors to think about in your estate planning. Basically, estate equalization is the process of helping ensure fairness in your estate plan, whether that means leaving all your primary heirs the same bequests or not. What Is Estate Equalization?

So, let’s say you contribute money to a traditional 401(k) plan in your 20s. As part of that, Congress established rules that require annual distributions from tax-advantaged plans once you reach age 72, 73 or 75. prior to 2020) 1951–1959 73 1960 or later 75 Required minimum distribution (RMD) rules can be complex.

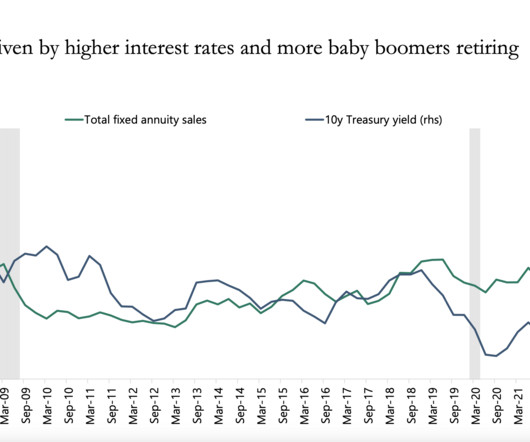

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” aka The Hidden World of Failure ) (October 23, 2020) Stock Ownership : Distribution of Household Wealth in the U.S.

By Brady Marlow, CFP, AEP, CAP, CPWA, CExP , Director, Carson Private Client Wealth Strategy Although most people focus first on loved ones in developing their estate plan, you may also want your legacy to include continuing support of issues and organizations youre passionate about. The trust is a wholly separate entity from you.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content