This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Accumulation-phase planning software won't cut it for solving your clients' complex retirement income puzzles, but there are dedicated applications that can.

(morningstar.com) The upside of a qualified charitable distribution or QCD. whitecoatinvestor.com) Aging These are the four phases of retirement. theretirementmanifesto.com) What you need to know about health care if you retire before age 65? wsj.com) Companies need to be more flexible when it comes to retirement.

The SEC claims Vanguard made misleading statements about capital gains distributions and tax consequences to retail investors who held target date funds in retirement accounts.

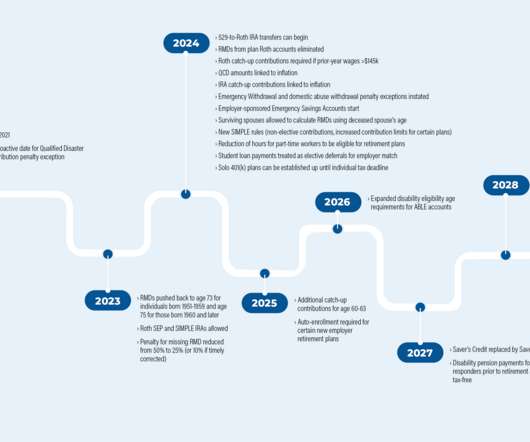

The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on planning than the changes to the post-death distribution rules for retirement accounts.

Act regarding individual retirement accounts, including changing when the first required minimum distribution can be made from the account, new rules for inhe The panel of experts will discuss and answer questions about the changes made by SECURE 2.0

And when it comes to retirement planning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes. If the portfolio balance declines due to excess distributions (e.g.,

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

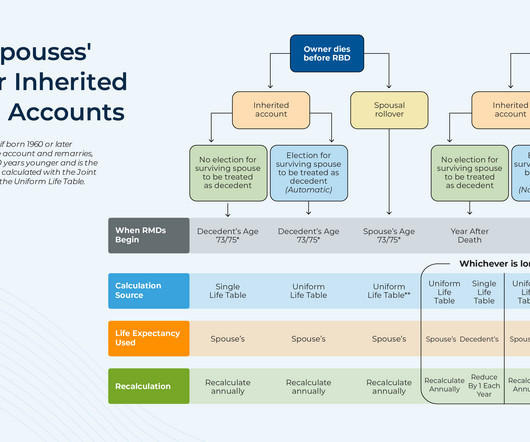

Among all the different types of retirement account beneficiaries, those who are the surviving spouse of the original account owner receive the most preferential tax treatment when it comes to distributing the account's assets after the owner's death. But the SECURE 2.0

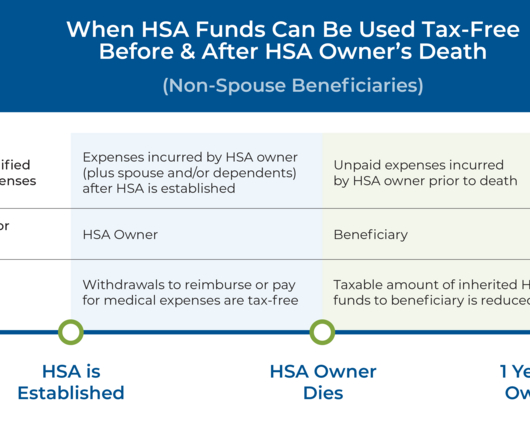

It’s also important for other parties involved in the owner’s estate plan to be aware of their roles, and to ensure that any funds withdrawn from the HSA are still distributed according to the HSA owner’s wishes.

When thoughtfully drafted, it aligns the interests of the firm's owners, sets clear expectations for operations, and establishes how profits will be distributed. The next step is establishing a profit distribution philosophy. As a foundational document, the operating agreement is essential for RIA firms.

When thoughtfully drafted, it aligns the interests of the firm's owners, sets clear expectations for operations, and establishes how profits will be distributed. The next step is establishing a profit distribution philosophy. As a foundational document, the operating agreement is essential for RIA firms.

For example, if taxes were expected to rise in the future, it would be better to contribute to a Roth retirement account (which is taxed on the contribution, but not upon withdrawal) than to a traditional pre-tax account (which is tax-deductible today but is taxable on withdrawal). Read More.

The combined business will operate under The Standard brand, and include Securian's retirement solutions employees, management, client relationships and distribution networks.

Because of the strict limitations on when and how the 529-to-Roth rollover can be done , it has limited usefulness as a planning tool beyond its intended purpose of giving individuals with overfunded 529 plans an opportunity to reallocate some of those funds tax-free towards their retirement savings. Read More.

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. An HSA can serve as an additional retirement savings vehicle on top of your IRA or 401(k) to help cover healthcare and other retirement expenses. Click To Tweet.

The deductibility phase-out is based on filing status, income (MAGI), and whether or not the individual(s) are eligible to participate in a retirement plan at work. When you make a distribution, the original nondeductible IRA contribution amount isn’t included in your taxable income, but the earnings and growth from it is.

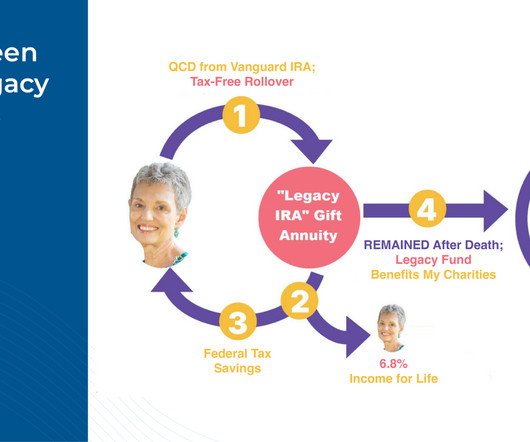

Act, passed in December 2022, created the ability for individuals over age 70 1/2 to make a one-time Qualified Charitable Distribution (QCD) of up to $50,000 of IRA funds into a CGA, with the amount distributed to the CGA being excludable from the donor's taxable income. But the SECURE 2.0 legislation at the end of 2022.

Qualified retirement plans – such as 401(k)s, 403(b)s and IRAs – offer clear tax advantages. Traditional 401(k)s, 403(b)s, and IRAs offer a tax deferral on contributions and growth until distribution. One of those is the Required Minimum Distribution (RMD) rule. Jamie Hopkins, Managing Partner, Wealth Solutions. RMD Basics.

by Jake Anderson, Paraplanner Retirement accounts like 401(k)s and IRAs allow individuals to save for their future in a tax advantaged manner. This gives you ample time to grow your savings and investments for retirement. IRAs and 401(k)s are primarily designed to help fund retirement not pass wealth onto future generations.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirement plans held by 10s of millions of Americans.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirement planning, the same questions often arise: What should my retirement plan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirement plan. How much should I be saving?

You can move these large stock holdings to a DAF, get the tax break, and then use the money to make donations every year through your retirement. Donate Your Required Minimum Distributions If youre 73 or older, required minimum distributions (RMDs) are kicking in.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts.

just upended retirement planning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. However, it doesn’t mean that delaying IRA distributions is the right move for everyone. The IRS may also require annual distributions during this window.

It was made as an independent film because none of the studios were interested: Nobody wanted to finance it; once it was financed, no one wanted to distribute it; even after a distribution deal was inked, no one wanted to show it or review it. But it almost wasn’t made at all.

Research on tax-efficient retirementdistribution strategies aims to sequence withdrawals from taxable, tax-deferred, and tax-exempt accounts to maximize after-tax spending.

Retirement planning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA. Are you financially ready for retirement?

wsj.com) Aging What you can learn from a 'retirement mastermind group.' humbledollar.com) Distributions What do required minimum distributions measure? (peterlazaroff.com) Trusts What is the difference between a personal representative and trustee? obliviousinvestor.com) When should you name a professional trustee?

From there, we have several articles on retirement planning: The latest rules for 2023 Required Minimum Distributions from inherited retirement accounts. Why relying on Treasury Inflation-Protected Securities (TIPS) to support the bulk of retirement income needs could be risky.

Although the 'one big pot' mindset might be the simplest approach to estate distribution, it may not be the one that results in the most wealth being passed down or the most equitable distribution of assets between each beneficiary. Read More.

The passing of the 2019 Secure Act changed the rules about when non-spouse beneficiaries must begin taking money from inherited retirement accounts. ” This meant annual required minimum distributions (RMDs) were out. Another key aspect that the 2019 Secure Act changed was the required minimum distribution age.

We’ve covered a lot of ground with regard to how various tax laws impact your retirement plans: pensions, IRAs, 403(b) and 401(k) plans. State Tax The big deal with state tax laws and retirement plans is that some states have special tax deals for money inside of retirement plans.

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

Key Takeaways: Preparing for retirement is important. Knowing their monthly expenses, social security plans, long term tax implications, and more can be important steps in helping clients prepare for retirement. Like a lot of people my age, I find myself thinking more and more often about retirement these days. We all know that.

Also in industry news this week: The Office of Management and Budget (OMB) has completed its review of the Department of Labor's new "fiduciary rule ", indicating that it could be released in the coming days or weeks (though, like its predecessors, its ultimate disposition is likely to be determined in the courts) The IRS announced this week that it (..)

Here are the distribution rules. If you’ve just inherited a retirement account like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. The change won’t impact anyone who inherited a retirement account during 2019 or years prior.

ofdollarsanddata.com) 15 reasons you may regret an RV in retirement. whitecoatinvestor.com) How to use in-kind distributions for RMDs. (awealthofcommonsense.com) 'Dying with zero' is a worthy goal, that is difficult to accomplish in practice. kiplinger.com) An example of putting an emergency fund into action. humbledollar.com).

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. This allows the account to grow on a tax-deferred basis, with income to beneficiaries being taxed when distributions are made.

Managing cash flow in retirement is a crucial aspect of financial planning that can feel daunting after decades of receiving regular paychecks. Consider new expenses like healthcare before Medicare coverage begins and subtract any expenses that will no longer apply in retirement, such as commuting or work-related clothing.

As you move toward retirement, you can’t be content just to accumulate assets. You need to develop a retirement income plan that can help guide you when it comes time to turn savings into sustainable retirement income. of Social Security benefits are paid to retired workers and their dependents.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. Raise the required minimum distribution age. In the bill, Roth 401(k) plans would also be freed of mandatory distributions starting in 2024.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content