This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course).

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

Qualified Charitable Distributions (QCDs) QCDs are direct transfers of funds from an individual retirement account (IRA) to a qualified charity. or older, QCDs offer a strategic way to contribute to charity while meeting required minimum distribution (RMD) obligations. Available to taxpayers aged 70.5

We would like to take this opportunity to remind you about your annual Required Minimum Distribution (RMD). As you may know, the Internal Revenue Service (IRS) requires that you take an annual distribution from your retirement accounts starting with the year in which you turn 72 years old and every year thereafter.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. Raise the required minimum distribution age. Keep in mind, matching contributions are often voluntary so it would be up to the plan as to whether to adopt this provision.

Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses. Dividends, interest, or capital gains distributions from mutual funds and ETFs received during the year are taxable annually.

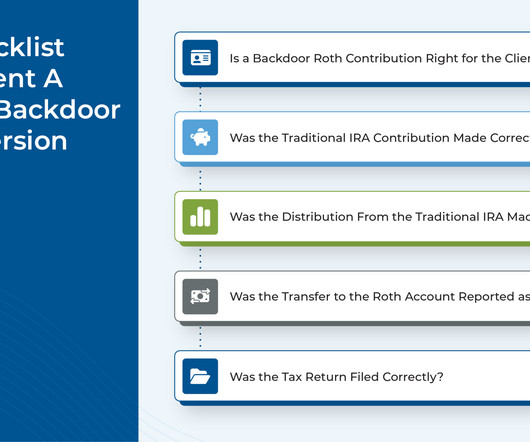

Backdoor Roth 401(k) $23,000 ($30,500 if 50+) Allows conversion of 401(k) funds to Roth, increasing tax diversification Required Minimum Distributions apply. It also requires an individuals 401(k) plan to allow after-tax contributions and in-service withdrawals. Complex setup process.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-taxretirement account distributions, dividends, etc., that could increase the tax due from the surtax.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. The example above assumes the couple does not need the full distribution from the IRA to meet lifestyle expenses.

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. What is Net Unrealized Appreciation?

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger. The next key step is to consolidate all of your retirement accounts.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Certified Financial Planner (CFP) CFPs are professionals who have completed rigorous education, passed a comprehensive exam and have substantial experience in financial planning.

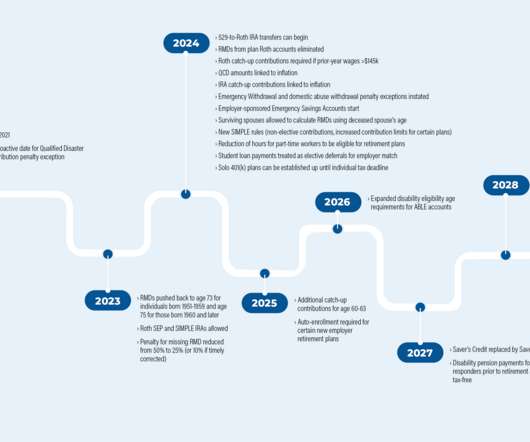

So it’s clear there may be some new planning opportunities on the horizon. The ability to do 529 plan to Roth IRA rollovers goes into effect January 2024. No required minimum distributions (RMDs) in Roth 401(k) plans. Starting with the 2017 Tax Cuts and Jobs Act, then the 2019 Secure Act 1.0, The Secure Act 1.0

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Certified Financial Planner (CFP) CFPs are professionals who have completed rigorous education, passed a comprehensive exam and have substantial experience in financial planning.

There are several actions you can take to avoid higher tax rates and retain more money, including: . Distributingtax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability . Diversify your Investment Portfolio. March 14, 2022. |. 0 Comments. 0 Comments.

Here are some innovative financial planning marketing ideas: Host workshops and webinars: These are effective ways to educate your audience on topics such as retirementplanning, investing strategies, and taxplanning.

Financial Planning Needs: Retirementplanning Education and family planning Obtaining appropriate insurance coverage Business and taxplanning Significant asset purchases Strategies for Serving Clients in This Stage: Clients at this stage are experiencing life events — both large and small — that will impact their financial planning needs.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

The 401(k) retirementplan is one of the most powerful tools. This tax-advantaged savings vehicle allows you to accumulate wealth steadily over a lifetime of diligent saving and investing. Start taxplanning A traditional 401(k) is a pre-tax account. You are not just looking to save for retirement.

By working with a tax professional, you can apply tax strategies to reduce your taxable income or defer paying taxes. 20 tax reduction strategies for high-income earners in 2024 Tax strategy is complex, and there are numerous ways of reducing taxable income depending on your situation.

These forms include: 1099-NEC (Non-Employee Compensation): Reports payments made to independent contractors or freelancers for services performed that total $600 or more in a tax year. 1099-DIV (Dividends): Reports dividends and other distributions from investments, typically received from stocks or mutual funds.

Apart from financial planning in the business sphere, entrepreneurs also need to engage in financial planning to save for retirement and financially protect their families. A well-tailored financial plan here becomes paramount. . Financial planning tips for entrepreneurs. Make the best use of tax-saving strategies.

By weaving in extra savings into your spending plan, you can have enough money to cover gifts, cook your fancy holiday dinner, and keep the lights on (literally). . Max Out Your RetirementPlans. Saving for retirement should be as commonplace as meal prepping for the week.

There now exists a meaningful incentive for many long-time Intel employees to retire from Intel before May 2021. We’ve received many questions so far about the relevance and magnitude of these changes on one’s retirementplans. What is the best time to retire from Intel? Income, Expense, and TaxPlanning.

Planning opportunities with RSUs: Use RSU income to maximize contributions to other benefits programs. Incorporate taxplanning with your RSU vesting schedule to minimize taxes. Planning Note: In some of the proposed tax changes currently in Congress for 2022, this Mega Backdoor Roth option is eliminated.

Planning opportunities with RSUs: Use RSU income to maximize contributions to other benefits programs. Incorporate taxplanning with your RSU vesting schedule to minimize taxes. Planning Note: In some of the proposed tax changes currently in Congress for 2022, this Mega Backdoor Roth option is eliminated.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. Asset diversification is an essential component of effective taxplanning.

There are income limits for contributions to a traditional IRA that qualify for a tax deduction. The deductibility phase-out is based on filing status, income (MAGI), and whether or not the individual(s) are eligible to participate in a retirementplan at work. To calculate the tax-free percentage: Your Total Basis (e.g.

The key to creating a diversified portfolio is to distribute your money across multiple asset classes, such as stocks, bonds, real estate, and alternative investments. Build an emergency fund for future financial emergencies An emergency fund is one of the most critical yet overlooked aspects of a financial plan.

If your financial advisor is not keeping a close eye on your taxes, they might be missing out on various opportunities that could impact your financial well-being. An effective financial advisor should be proactive in reviewing your taxplan before the year-end.

As such, one of the most important retirement income resources is Social Security, which provides retirees inflation-adjusted income for life. Making the right decisions around claiming Social Security — based on your spending needs, longevity and taxplanning — could mean the difference between meeting your retirement goals or not.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content