This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

For example, if taxes were expected to rise in the future, it would be better to contribute to a Roth retirement account (which is taxed on the contribution, but not upon withdrawal) than to a traditional pre-tax account (which is tax-deductible today but is taxable on withdrawal).

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

From there, we have several articles on taxplanning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions. A new research study suggests that delaying taxes in retirement is often not the optimal course of action.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

is significant legislation signed into law on December 20, 2022, and is expected to have several impacts on retirement income planning. It contains several provisions designed to improve Americans' retirement security, including later required minimum distributions (RMDs), 529-to-Roth rollovers, and other taxplanning opportunities.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

Which suggests that while firms might be tempted to zero in on compensation when it comes to retaining advisors, focusing on these other factors (which do not necessarily involve hard dollar expenses) could pay off in the form of increased advisor (and client) retention over time.

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Planning can help optimize annual RMDs depending on your goals and cash flow needs. Mandatory withdrawals from retirement accounts begin for most taxpayers at age 72. For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs.

In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Available to taxpayers aged 70.5

After you’ve spent your whole life working, you may find that in retirement, you want to give some money to charity. But if you are living off of income streams from sources like your retirement accounts and Social Security, you may be worried about finding a way to make charity work for your financial picture.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. Raise the required minimum distribution age. In the bill, Roth 401(k) plans would also be freed of mandatory distributions starting in 2024.

Financial advisors play a crucial role in assisting you before your retire. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Here are 5 benefits of hiring a financial advisor after you retire: 1.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

We would like to take this opportunity to remind you about your annual Required Minimum Distribution (RMD). As you may know, the Internal Revenue Service (IRS) requires that you take an annual distribution from your retirement accounts starting with the year in which you turn 72 years old and every year thereafter.

Investing after maxing out a 401(k) is smart, especially since your retirement accounts may not be enough to fully fund the lifestyle you want. If you have time to dig into the details, here’s a primer on what you can do after maxing out a 401(k) including the tax advantages of each account type.

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

Financial advisors want to make the right suggestions surrounding taxable Social Security benefits for their retired clients. In many cases, properly planningretirement account withdrawals alongside Social Security benefits can lower the total tax burden. Let’s look at how to help clients with taxable Social Security.

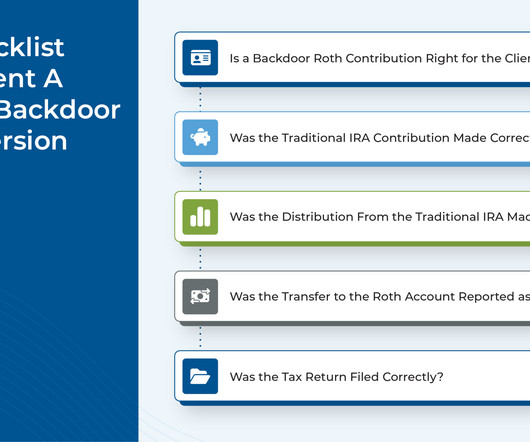

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-taxretirement account distributions, dividends, etc., that could increase the tax due from the surtax.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

A little bit of effort and forward thinking during our summer and fall months will lead to a much more palatable and, potentially, financially advantageous tax season the following year. The reason for this is quite simple – taxplanning requires actual planning. One of the reasons to consider could be taxes.

When tax rates are stable, it’s wise for you to defer as much income as possible from one year to a later year and to accelerate deductions so that you can postpone payment of the tax. When you eventually realize the income at some future point, it’s possible that you’ll be retired and/or in a lower tax bracket.

For those employees eligible for Intel’s minimum pension benefit (MPP) at retirement, the interest rate used to calculate today’s value of that benefit is changing. This means that your estimated Minimum Pension Plan benefit amount is significantly reduced or erased altogether in many cases. What should I do next?

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. What is Net Unrealized Appreciation?

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers. So it’s clear there may be some new planning opportunities on the horizon. The ability to do 529 plan to Roth IRA rollovers goes into effect January 2024. Prior to the passing of Secure Act 2.0,

Use a qualified charitable distribution (QCD) from your individual retirement account (IRA). If you are age 70 ½ or older, you can transfer money from your IRA to a charity as a qualified charitable distribution (QCD), which makes it tax-free up to $100,000 ($200,000 if you file jointly).

However, a period of lower income in 2024 could present valuable taxplanning opportunities. One potential benefit of a job layoff is a temporary drop in your federal income tax bracket, which can create opportunities for future tax savings.

Starting Out clients are likely to be digitally-fluent, so putting this type of responsibility on them isn’t overly burdensome and can create major efficiencies in your planning processes. Holistic planning will be a valuable way for you to address this broad range of needs.

Retiring Abroad? TEP Zoe Financial Services Partner Retiring Abroad? TEP Zoe Financial Services Partner From sandy beaches to bustling cities, there are no limits to the retirement of your dreams as long as you know how to plan for it. income tax returns and Form 8621 reporting.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

There are several actions you can take to avoid higher tax rates and retain more money, including: . Distributingtax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability . Consult an Advisor on Retirement Accounts. What is Portfolio Rebalancing?

By working with a tax professional, you can apply tax strategies to reduce your taxable income or defer paying taxes. 20 tax reduction strategies for high-income earners in 2024 Tax strategy is complex, and there are numerous ways of reducing taxable income depending on your situation.

Besides meeting all the requirements for this date, have you considered the impact of implementing long-term tax strategies on your wealth? So take advantage of the opportunity to optimize your taxplanning and maximize your financial growth potential. Traditional Pre-Tax or Roth After-Tax Saving?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content