This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Over the last 60 years, the top Federal marginal tax bracket has steadily decreased from over 90% in the 1950s and 60s to 'just' 37% today. While it's true that the top marginal tax rate has decreased dramatically since the mid-20th century, the difference in the actual tax paid by most Americans has been far more modest.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

The SEC claims Vanguard made misleading statements about capital gains distributions and tax consequences to retail investors who held target date funds in retirement accounts.

Health Savings Accounts (HSAs) feature useful tax advantages that make them a popular savings vehicle. One possible outcome of ‘superfunding’ an HSA, however, is that the account owner may not actually use up all of their HSA funds over their lifetime, which can have significant tax consequences. Read More.

open.spotify.com) Taxes What happens if you don't file and/or pay your taxes. financialducksinarow.com) Who pays taxes on Social Security benefits? morningstar.com) The upside of a qualified charitable distribution or QCD. whitecoatinvestor.com) Aging These are the four phases of retirement.

Would you rather give that amount directly to the organization or withdraw $100,000, pay $40,000 in taxes and have only $60,000 of your contribution left to donate? Obviously, youd choose to avoid taxes and give the full amount, especially if that approach brought additional tax benefits with it. Note: This only applies to U.S.-based

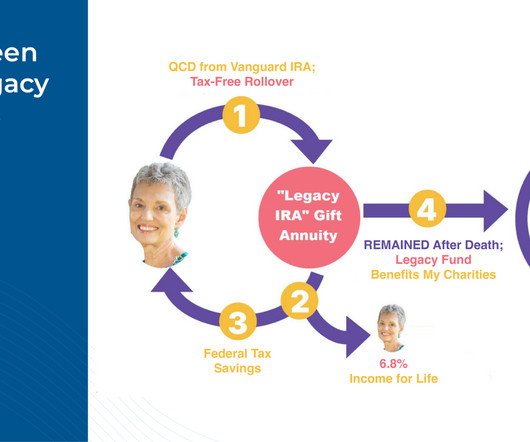

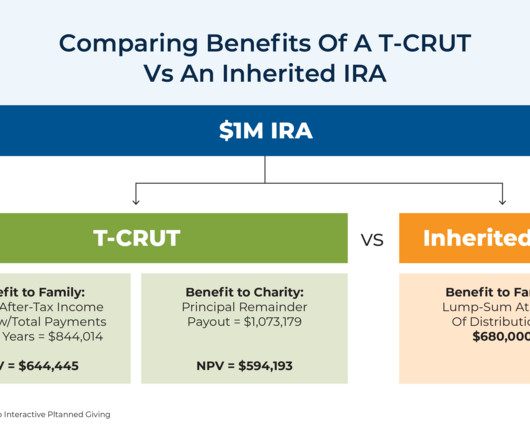

However, the caveat with current CGAs has been that they could only be funded with after-tax dollars before the donor’s death, meaning that if an individual only had tax-deferred funds (e.g., Second, they reduce the donor's tax bill in the year the CGA is created by excluding the amount contributed to the CGA from taxable income.

As December unfolds, it’s easy to overlook year-end tax planning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

The maximum amount of earnings subject to Social Security tax (taxable maximum) will increase to $176,100 from $168,600. The individual tax brackets for ordinary income have been adjusted by inflation. On average, tax parameters that are adjusted for inflation will increase about 2.80%.

Would you like to diversify but also defer paying big capital gains taxes? I’m Barry Ritholtz and on today’s edition of at the money we’re going to discuss how to manage concentrated equity positions with an eye towards diversification and managing big capital gains taxes. None of these solutions are optimal.

Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Yes and no.

Although the 'one big pot' mindset might be the simplest approach to estate distribution, it may not be the one that results in the most wealth being passed down or the most equitable distribution of assets between each beneficiary.

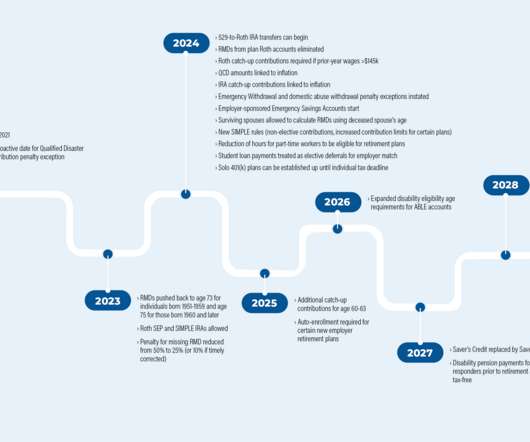

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Like gardening or working out, tax planning is one of those activities where you get out what you put in. Tax planning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Tax planning is similar in the sense that you can put work in on the front end that youll reap benefits from later.

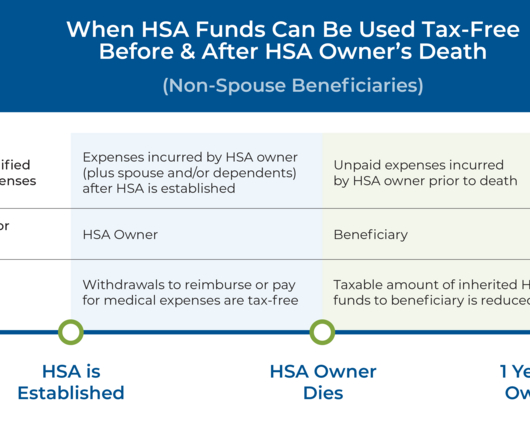

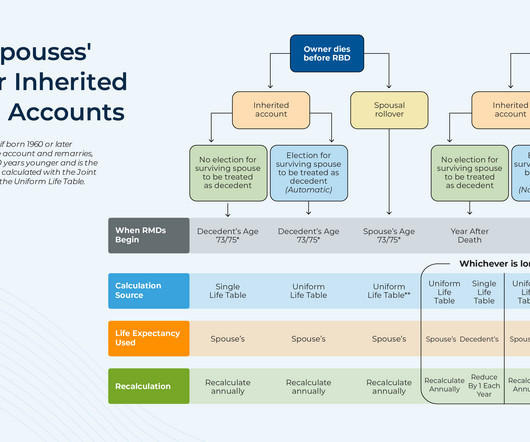

Among all the different types of retirement account beneficiaries, those who are the surviving spouse of the original account owner receive the most preferential tax treatment when it comes to distributing the account's assets after the owner's death. But the SECURE 2.0

And so the conundrum of people with "too much" savings in their 529 plan – either because they overestimated how much they needed to save, or because they chose a different path entirely that didn't involve going to college – has been how to get funds out of the plan without sacrificing a large part of their value to taxes and penalties.

Strategic charitable giving not only benefits the recipient but can also create significant tax advantages for the giver. You can deposit money into the account now, receive the tax benefit, and then make the donation in your own time. Theres no time limit on when you need to make the donation.

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. The costs of adopting a child can vary significantly depending on the method of adoption.

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. An HSA can serve as an additional retirement savings vehicle on top of your IRA or 401(k) to help cover healthcare and other retirement expenses. Prescription drugs and insulin.

Research on tax-efficient retirementdistribution strategies aims to sequence withdrawals from taxable, tax-deferred, and tax-exempt accounts to maximize after-tax spending.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirement plans held by 10s of millions of Americans.

Qualified retirement plans – such as 401(k)s, 403(b)s and IRAs – offer clear tax advantages. Traditional 401(k)s, 403(b)s, and IRAs offer a tax deferral on contributions and growth until distribution. To prevent individuals from taking advantage of the tax-deferred growth in perpetuity, there are certain rules in place.

by Jake Anderson, Paraplanner Retirement accounts like 401(k)s and IRAs allow individuals to save for their future in a tax advantaged manner. IRA and 401(k) contributions are often tax deductible and gains are tax deferred – meaning you may only pay taxes when you withdraw money from your account.

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirement planning, the same questions often arise: What should my retirement plan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirement plan. How much should I be saving?

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

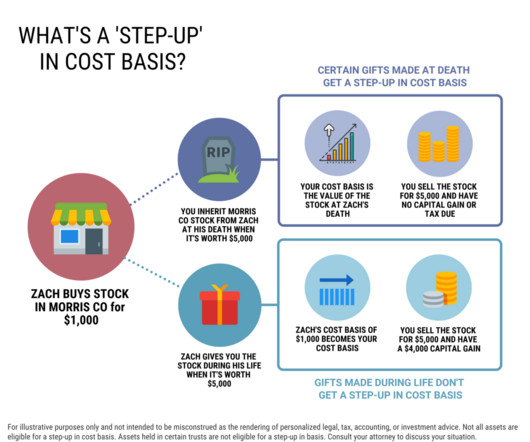

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets. This increases the tax basis, which determines capital gains or losses when the asset is sold.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts.

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

just upended retirement planning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. However, it doesn’t mean that delaying IRA distributions is the right move for everyone. The Secure Act 2.0 When should you start taking money from IRAs?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

As you move toward retirement, you can’t be content just to accumulate assets. You need to develop a retirement income plan that can help guide you when it comes time to turn savings into sustainable retirement income. of Social Security benefits are paid to retired workers and their dependents.

A potential compromise during the lame-duck Congressional session could see a boost to the child tax credit and extended tax breaks for businesses. From there, we have several articles on tax planning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions.

wsj.com) Aging What you can learn from a 'retirement mastermind group.' humbledollar.com) Distributions What do required minimum distributions measure? nytimes.com) What can we learn from past Presidents' tax returns? (peterlazaroff.com) Trusts What is the difference between a personal representative and trustee?

This month's edition kicks off with the news that robo-advisor Betterment entered into a $9M settlement with the SEC for misrepresenting its tax-loss harvesting practices in its client agreements and marketing materials compared with its actual practices (e.g.,

Retirement planning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA. Maybe you have a growing family.

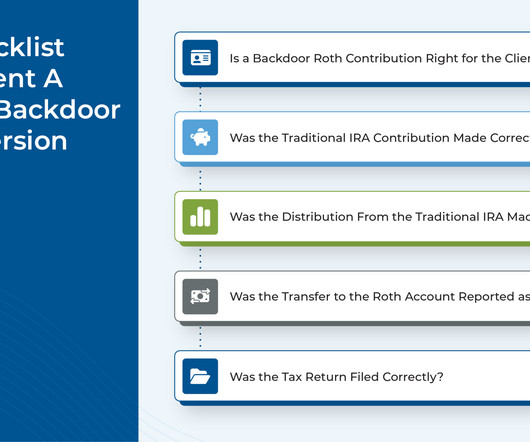

There are many tax planning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Advisors also can support the backdoor Roth process by communicating with clients' tax preparers about the strategy and why they are recommending it for their mutual client.

We’ve covered a lot of ground with regard to how various tax laws impact your retirement plans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

The Tax Impact of Charitable Giving The personal financial and income tax impact from charitable giving can affect the size of the gift and the timing of giving. If a family has a large taxable income year, they may be willing to increase donations to reduce their income tax liability.

Also in industry news this week: The Office of Management and Budget (OMB) has completed its review of the Department of Labor's new "fiduciary rule ", indicating that it could be released in the coming days or weeks (though, like its predecessors, its ultimate disposition is likely to be determined in the courts) The IRS announced this week that it (..)

Key Takeaways: Preparing for retirement is important. Knowing their monthly expenses, social security plans, long term tax implications, and more can be important steps in helping clients prepare for retirement. Like a lot of people my age, I find myself thinking more and more often about retirement these days.

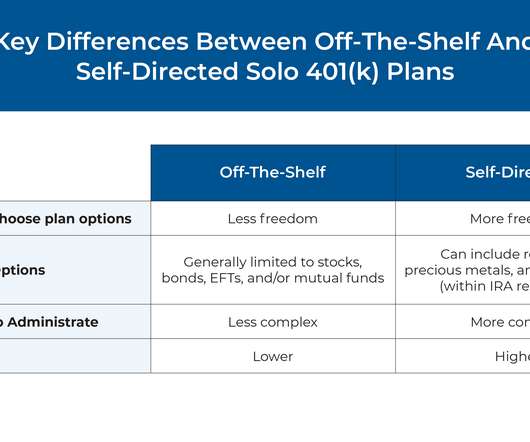

Among the several different types of retirement plans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content