This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

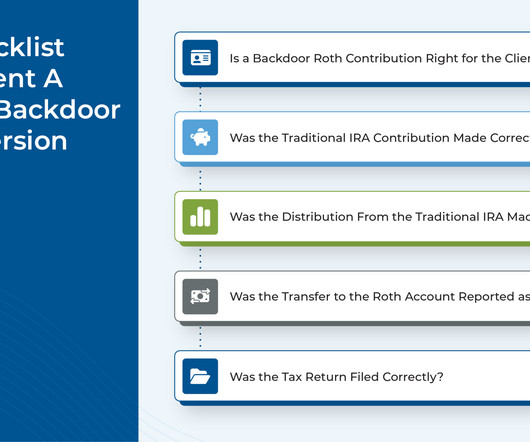

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

This week, Orion announced they were making it easier for those in need of free financial planning to find help, TIFIN and Morningstar partnered to enhance their AI-powered distribution platform and eMoney responded to recently-passed legislation with taxplanning upgrades.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

Because not only were very few households actually subject to the 1950s-era top tax rates (which were triggered at the equivalent of over $2 million of income in today's dollars), but the long decline in nominal tax rates has also come with the elimination of many loopholes and deductions that have resulted in more income being subject to tax.

However, it doesn’t mean that delaying IRA distributions is the right move for everyone. Here are some taxplanning strategies to consider when you should start drawing from your IRA. Here are some taxplanning strategies to consider when you should start drawing from your IRA.

Here are five reasons we suggest skipping nondeductible IRA contributions: How non-deductible contributions are taxed Never-ending recordkeeping requirements Capital gains tax rates vs ordinary income State tax rules, inherited IRA issues, and RMDs Other accounts may be better retirement planning vehicles 1. Yes and no.

A potential compromise during the lame-duck Congressional session could see a boost to the child tax credit and extended tax breaks for businesses. From there, we have several articles on taxplanning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts. As a whole, these regulations introduce significantly more complexity to the process of taxplanning around retirement accounts, particularly after the death of the account's original owner.

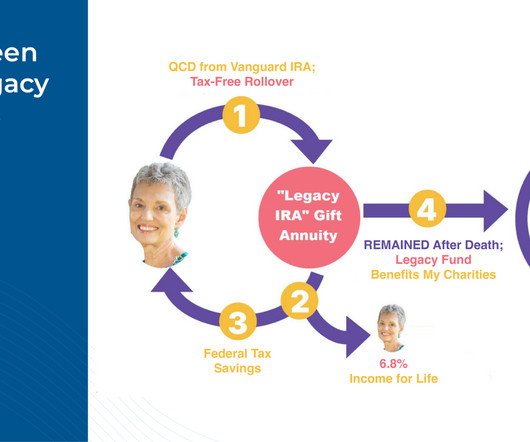

Act, passed in December 2022, created the ability for individuals over age 70 1/2 to make a one-time Qualified Charitable Distribution (QCD) of up to $50,000 of IRA funds into a CGA, with the amount distributed to the CGA being excludable from the donor's taxable income. But the SECURE 2.0 legislation at the end of 2022.

Key among them are the options to roll over the account into their own IRA, keep it as an inherited IRA, or consider varying stances based on the decedents Required Minimum Distributions (RMDs). Unlike non-eligible beneficiaries who are limited to a strict ten-year distribution period, EDBs can choose from various withdrawal schedules.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

” This meant annual required minimum distributions (RMDs) were out. Another key aspect that the 2019 Secure Act changed was the required minimum distribution age. Assuming the changes pass, some beneficiaries will have missed a required distribution. Individuals born before July 1, 1949 will retain an RMD age of 70 1/2.

This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. This allows the account to grow on a tax-deferred basis, with income to beneficiaries being taxed when distributions are made.

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course).

Make sure they take their required minimum distributions Clients who are age 73 or over must take required minimum distributions (RMDs) from their qualified plans and IRAs. Businesses There are several steps that business owners may want to take in 2022 to minimize taxes.

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Making the right decisions around claiming Social Security — based on your spending needs, longevity and taxplanning — could mean the difference between meeting your retirement goals or not. Distributions from IRAs and 401(k)s are often taxable. As such, they raise your tax rates and taxable income.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Also in industry news this week: 2 House committees this week advanced legislation that would halt implementation of the Department of Labor's new Retirement Security Rule, which, combined with ongoing lawsuits, threaten to derail the regulation either before or soon after it becomes effective in late September A Federal judge has put the future of (..)

Qualified Charitable Distributions (QCDs) QCDs are direct transfers of funds from an individual retirement account (IRA) to a qualified charity. or older, QCDs offer a strategic way to contribute to charity while meeting required minimum distribution (RMD) obligations. Available to taxpayers aged 70.5

We would like to take this opportunity to remind you about your annual Required Minimum Distribution (RMD). As you may know, the Internal Revenue Service (IRS) requires that you take an annual distribution from your retirement accounts starting with the year in which you turn 72 years old and every year thereafter. Annual deadlines.

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. The first three options are pass-through entities, so profits and losses are distributed to the owners who are taxed on them.

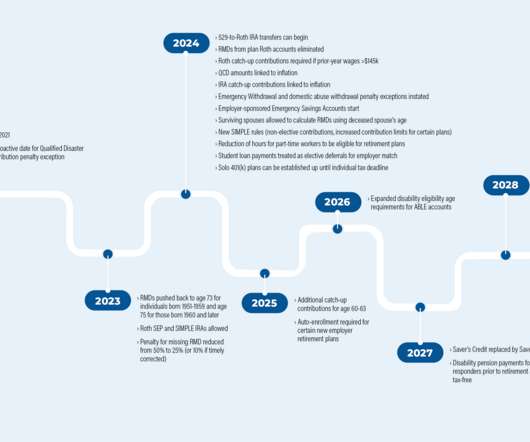

is significant legislation signed into law on December 20, 2022, and is expected to have several impacts on retirement income planning. It contains several provisions designed to improve Americans' retirement security, including later required minimum distributions (RMDs), 529-to-Roth rollovers, and other taxplanning opportunities.

Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency. The usage policy establishes the purposes for which the charity can use the fund distributions.

Here are the distribution rules. This article focuses on the distribution rules for non-eligible designated beneficiaries as that is most common. Which non-eligible designated beneficiaries have required minimum distributions? Now the question is: which beneficiaries are also subject to required minimum distributions?

Instead, partners (investors) are taxed directly on their share of the fund’s income, gains, losses, and deductions, regardless of whether those amounts are actually distributed. Each partner receives a Schedule K-1, which reports their share of the fund’s tax items. FIRPTA planning using a U.S.

For example, if you convert $50,000 and it grows to $100,000 in a Roth IRA over the next several years, that essentially results in $50,000 tax-free dollars. Keeping your funds in a traditional IRA only defers taxation on the full amount until the funds are distributed at some point in the future.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). .

Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses. Dividends, interest, or capital gains distributions from mutual funds and ETFs received during the year are taxable annually.

There are three buckets of estate planning to consider: the estate planning everyone should do, which includes will creation, the estate planning for those that want to preserve assets for beneficiaries, and estate planning for strategic taxplanning. at the federal level. Get started here.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning.

In general, you won’t be required to pay income taxes to another state simply because you opened a 529 account in that state. But you’ll probably be taxed in your state of residency on the earnings distributed by your 529 plan if the withdrawal is not used to pay the beneficiary’s qualified education expenses.

It was once common for donors to distribute their wealth through smaller grants to numerous organizations. But the donor or a representative of the donor has advisory privileges regarding the distribution of the funds or the investment of assets in the accounts. [i] A CRT may be partially tax-deductible right away.

This will allow you to bunch your donations in a single year but then distribute them over a long period of time. [1] 1] The benefit to this is that you can still gain the tax advantage of a large, itemized donation but can distribute your donations over more than just one year. [1]

It also helped minimize the tax impact of inherited accounts. . However, the SECURE Act effectively eliminated the stretch strategy by requiring that all inherited IRAs and 401(k)s must be distributed within 10 years after the death of the owner. When done right, this can be a very valuable taxplanning strategy.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

Control the distribution of your assets When assets go through probate, the court ultimately decides who gets what. If the assets were held in a living trust, you could not only avoid probate (or reduce the probate estate), but also control the timing and distribution of the assets. States have their own estate tax laws.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., that could increase the tax due from the surtax.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content