This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This week, Orion announced they were making it easier for those in need of free financial planning to find help, TIFIN and Morningstar partnered to enhance their AI-powered distribution platform and eMoney responded to recently-passed legislation with taxplanning upgrades.

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

However, it doesn’t mean that delaying IRA distributions is the right move for everyone. Here are some taxplanning strategies to consider when you should start drawing from your IRA. Here are some taxplanning strategies to consider when you should start drawing from your IRA.

Here are five reasons we suggest skipping nondeductible IRA contributions: How non-deductible contributions are taxed Never-ending recordkeeping requirements Capital gains tax rates vs ordinary income State tax rules, inherited IRA issues, and RMDs Other accounts may be better retirement planning vehicles 1. Yes and no.

Inheriting a Trust Fund: Distributions to Beneficiaries Do You Pay Tax on an Inheritance? These rules can be very complex and nuanced so its essential to consult with a tax professional and trust and estates attorney to understand the specific rules and current law in your state. Yes and no. The post What is a Stepped Up Basis?

” This meant annual required minimum distributions (RMDs) were out. Another key aspect that the 2019 Secure Act changed was the required minimum distribution age. Assuming the changes pass, some beneficiaries will have missed a required distribution. Individuals born before July 1, 1949 will retain an RMD age of 70 1/2.

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course).

How to Choose the Right WealthManagement Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealthmanagement firm in the Kansas City metro area.

Here are the distribution rules. This article focuses on the distribution rules for non-eligible designated beneficiaries as that is most common. Which non-eligible designated beneficiaries have required minimum distributions? Now the question is: which beneficiaries are also subject to required minimum distributions?

Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision. Darrow WealthManagement doesn’t provide tax advice; consult your tax advisor to discuss your personal situation. . that could increase the tax due from the surtax.

How to Choose the Right WealthManagement Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealthmanagement firm in the Kansas City metro area.

Control the distribution of your assets When assets go through probate, the court ultimately decides who gets what. If the assets were held in a living trust, you could not only avoid probate (or reduce the probate estate), but also control the timing and distribution of the assets. States have their own estate tax laws.

Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses. Dividends, interest, or capital gains distributions from mutual funds and ETFs received during the year are taxable annually.

We recently connected with Michael Paley, Chief Operating Officer of Klingman & Associates , for a Q&A on how tax advisors can collaborate with wealthmanagers to better serve clients. Unlike an endowment, taxes really matter. What we often see is people are too late to think about estate taxes.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). .

If you are expecting sudden wealth from the sale of a business or other liquidity event, then it may not make sense to do a conversion in the same tax year, but could be worth considering alongside cash allocation discussions. If they did, the prior year conversion would have no impact on their taxable IRA distributions this year.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. Raise the required minimum distribution age. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley WealthManagement, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley WealthManagement, LLC. Part 1: The Tools of the Tax-Planning Trade. No wonder people get nervous when there’s lots of talk about higher taxes, but little certainty on what may come of it, and who it might affect. .

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog. appeared first on Darrow WealthManagement.

Probate is a legal process where certain assets that were owned in the individual’s name are distributed by the probate court. The probate court will use the will to help guide their distributions and other decisions. Limiting access can provide estate taxplanning benefits for some).

So it’s clear there may be some new planning opportunities on the horizon. The ability to do 529 plan to Roth IRA rollovers goes into effect January 2024. No required minimum distributions (RMDs) in Roth 401(k) plans. Starting with the 2017 Tax Cuts and Jobs Act, then the 2019 Secure Act 1.0, The Secure Act 1.0

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

Use a qualified charitable distribution (QCD) from your individual retirement account (IRA). If you are age 70 ½ or older, you can transfer money from your IRA to a charity as a qualified charitable distribution (QCD), which makes it tax-free up to $100,000 ($200,000 if you file jointly).

To attract new clients and foster long-term relationships, tax advisors could consider adopting digital marketing strategies. For example, “comprehensive taxplanning” or “long-term tax strategies for small businesses” can, over time, help you attract the right visitors.

A few years ago, if you inherited an IRA from a parent, the distribution rules were simple: you could stretch withdrawals over your life expectancy. This was widely interpreted to mean required minimum distributions (RMDs) were gone, and instead, beneficiaries must take the entire sum within 10 years.

Unfortunately, the Commonwealth also passed a ‘millionaire tax’, which adds a 4% surtax to taxable income over $1M , even for one-time sudden wealth events. To expand the tax benefits past the 10x/$10M limits, consider planning strategies such as gifting stock to family members.

Some companies offer the benefit of employees owning stock in the employer company through 401(k) plans, profit-sharing plans, stock bonuses and employee stock ownership plans (ESOP). Anyone who owns company stock will eventually have to decide how to distribute those assets when leaving the company or entering retirement.

The new Regulations generally clarify (1) the trust look-through rules that apply when a trust is designated as a beneficiary of qualified plans (401(k), 403(b), and 457 plans generally), or individual retirement accounts, and (2) the required minimum distribution (RMD) requirements on designated beneficiaries subject to the new 10-year payout rule.

It involves deciding how your assets will be distributed upon your death or incapacitation. Furthermore, estate planning includes aspects such as tax minimization strategies, asset protection, and charitable giving. There are many different types of trusts, each designed to address specific estate planning needs.

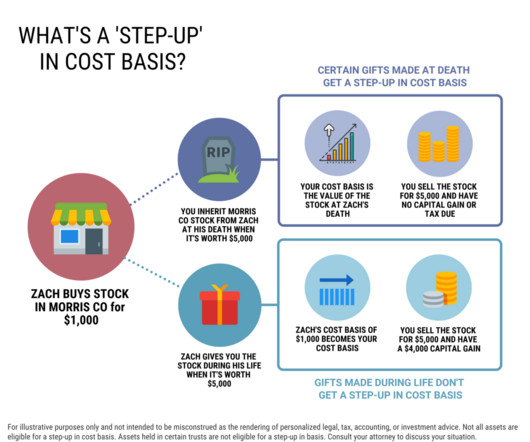

It’s important to understand the tax implications of this structure, as it may impact the timing and amount of taxes owed. It’s crucial to accurately calculate the cost basis in order to report capital gains taxes correctly. Tax services provided through Harness Tax LLC.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog. appeared first on Darrow WealthManagement.

To rank higher in search engine results, ensure your website includes key terms like “financial advisor,” “wealthmanagement,” or other relevant phrases. Distribute these videos on your business website, social media platforms, and through email campaigns to reach a wider audience.

In this article, we’ll go into detail on what to think about when it comes to financial planning, as well as a step-by-step process of how to build a sample financial plan that aligns with your personal goals and needs. Table of Contents What is a Financial Plan? Why is Financial Planning so Important?

Taxes are inevitable, but the amount you pay each year doesn’t have to be. There are several actions you can take to avoid higher tax rates and retain more money, including: . Distributingtax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability .

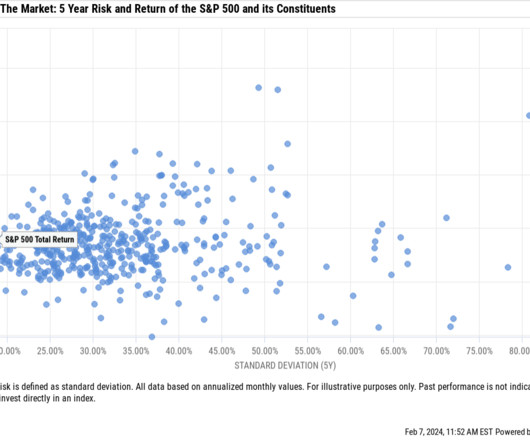

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ 5 ways to manage a concentrated stock position In no particular order, here are some strategies to reduce the risk of concentrated stock wealth.

If you wish to create a customized financial plan that will enable you to build a successful entrepreneurial venture, consult with a professional financial advisor who can guide you on the same. Why is financial planning important for entrepreneurs? A well-tailored financial plan here becomes paramount. .

If the present value of the minimum benefit is greater than the RC Account, then the MPP provides a benefit in the form of an annuity or a lump-sum distribution to make up for the shortfall (for more on evaluating whether to elect a lump sum or annuity payment, jump to this section ). Income, Expense, and TaxPlanning.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. Please conduct your own diligence on any wealthmanager you are considering hiring. Hourly financial advisors are not common. Jon Luskin.

If you are a high-net-worth individual and wish to learn about wealth preservation, tax-saving strategies, and management of large estates; engage the services of a wealth advisor who can advise you on the same. Income and capital gains taxplanning: The tax system in the U.S

However, in the past three decades, the confluence of tech innovation, and the democratization of financial product distribution and private capital have led to a boom in the independent registered investment advisor (RIA) channel.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content