This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Welcome to the 432nd episode of the Financial Advisor Success Podcast! Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

The traditional way that most financialplanning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client's financial strategy that was delivered either on a one-time basis or updated annually.

While many IRAs include a clause in their advisory agreements limiting their liability in giving financialadvice in good faith, the SEC and state regulators have recently been scrutinizing such ‘hedge clauses’ to the extent that they may be found impermissible going forward.

While many IRAs include a clause in their advisory agreements limiting their liability in giving financialadvice in good faith, the SEC and state regulators have recently been scrutinizing such ‘hedge clauses’ to the extent that they may be found impermissible going forward.

Yet despite this – and perhaps even because of it – advisory firms are putting an ever-greater focus on financialplanning in 2022, as a way to both show value to clients in the midst of difficult market returns, and, more broadly, to help clients navigate the current environment.

riabiz.com) AI Is AI an existential threat to the business of financialadvice? advisorperspectives.com) Vanilla is rolling out more AI tools for estate planning. investmentnews.com) Compliance How to conduct and document an annual compliance review. riabiz.com) The upside of pro bono financialplanning.

There are many financialplanning considerations before, during, and after a divorce. A key part of the process from a financial standpoint is dividing the assets. Once the divorce is finalized, a crucial (but often overlooked) part of the process is updating estate documents and beneficiary designations.

As the move to transparency in financialplanning takes hold, regulations are changing in Colorado and other states. Here’s the triumph of virtue that financialplanning transparency will (FINALLY) bring to planners across the country and the benefits to clients that come along with it. What should financial advisors do?

Closer Than Ever to Clients “We are incredibly bullish on the future of financialadvice.” ” That’s Shawn Mihal, LPL’s new head of financial institution services, sharing his firm’s recent successes with the Bank Insurance and Securities Association (BISA).

We speak a secret language in financialplanning. Translating from the secret language of financialplanning, the sentence would read “Tammy specializes in insurance. Financial service professionals like Tammy climb a competence stairway to work with clients. Common degrees used in financialplanning include: .

Recognizing the need for a financialplan is a significant first step toward the goal of achieving personal financial security. Table of Contents What is a FinancialPlan? Table of Contents What is a FinancialPlan? Why is FinancialPlanning so Important?

Financial paraplanners can be recent college graduates with no work experience, or may also be career changers with an extensive background in other areas that can add more value to an RIA owner, such as tax professionals. He cold called over 500 financialplanning companies over a year or so to get to a full book of clients.

Share important articles, industry news, and useful tips on financialplanning. Always follow the rules for sharing financial information on social media. Offering Personalized FinancialAdvice Through Video Marketing In today’s world, people really like visuals. Basic financialadvice doesnt work anymore.

Considering the fact that the country’s population is likely to have more older people in the near future, it becomes vital to ensure the financial interests of the community are safeguarded at all costs. Elder financialplanning can help eliminate some common issues faced by older people.

Keep in mind that many financial advisor certifications and distinctions, including the Certified Financial Planner (CFP) , uphold strict ethical standards, and require their financial advisors to act as a fiduciary, meaning that they must put the needs and best interests of the clients ahead of their own.

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Table of Contents What Services Does a Financial Advisor Provide? Are Robo-Advisors a Good Alternative?

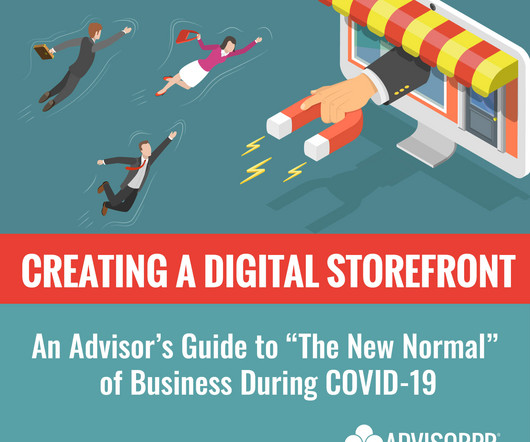

Creating Your Digital Storefront Policy (DSP) At AdvisorPR, we encourage you to create a Digital Storefront Policy, a proactive document that explains how you are available to safely provide digital service to your clients. This may even be a great virtual event you can host!) List your platforms here.)

This is because you have been failing to plan your funds because of less time, following the old ways, peer pressure, less understanding of the financial markets, and so on. A financial advisor is a certified financial planner who is licensed and regulated to take mandate decisions on multiple aspects of financialplanning.

To utilize this client retention strategy, go beyond mere financialadvice by listening actively, showing empathy, and asking about client concerns, aspirations, and feedback. Host quarterly webinars where clients learn more about your firm, ask financial questions, and get real-time answers.

Search for Unclaimed Funds and Gather Documentation: Start by locating any previous plan statements you may have, as they will provide your account number and the plan administrator’s contact information. Moreover, incorporating flexibility into financialplanning and daily schedules can significantly enhance work-life balance.

But no doubt that individuals have amassed a large amount of assets in their, what we call concentrated wealth at work or their retirement plans. Also very attractive from a financialplanning perspective and a net new asset gathering perspective. So that’s another key decision point.

If you are not careful you can wind up paying a lot of money for crap, or even getting blatantly deceived about what you are paying for when you hire a financial advisor. Are they just providing financialplanning? Don’t assume all financial advisor business models are the same. But first – what is a Form ADV?

This interview with Cody Garrett, CFP, of Measure Twice Financial was mind-blowing. It’s so clear to me what the future of financialadvice is – what it should be – and what it will be. I am an irreverent and fun marketing consultant for financial advisors. What is an advice-only financial planner?

Of course, this was never finalized. The second petition asks the SEC to stop pretending that giving financial/investment advice is “solely incidental” to the current wirehouse business model.

He thinks that the distinction has been deliberately (and very effectively) blurred by the brokerage industry, which advertises itself as helping facilitate peoples’ dreams with financialplanning and investment advice, whose brokers call themselves, on their business cards, advisors, vice presidents of investments or wealth managers. “If

You know, you put it off every day and you shouldn’t, nobody here that listens to this show should not have a financialplan even if they did it themselves. And, and Gimme One More 00:52:22 [Speaker Changed] Financially Fearless by Katie song, which was written out of a need Facebook group.

It is not personal legal/tax/financialadvice or an exhaustive discussion of the exclusion. But no extra supporting documentation is sent when filing (e.g. So the best practice is to document early and often and get a QSBS attestation letter from the company. Form 8949 and Schedule D).

As it turned out, financialplanning is where I felt I could have the most impact. I greatly benefited from financialadvice and my mission from that point on was to pay it forward. I wanted to help others with financialplanning and advice. Don’t be afraid to ask! Health insurance.

As it turned out, financialplanning is where I felt I could have the most impact. I greatly benefited from financialadvice and my mission from that point on was to pay it forward. I wanted to help others with financialplanning and advice. Don’t be afraid to ask! Health insurance.

A special needs trust document helps with these situations in managing the assets over their lifetime. Unmarried couples need to execute the right agreements and other documents, because many states do not provide the protection you likely want. Or, what if you die when your child is unmarried with minor children. Consider your home.

My father was an investment advisor, and he made his way to be an investment advisor from being a manager with a textile factory to selling insurance to find his way out of that business, went from insurance to financialplanning, financialplanning to the independent broker-dealer world, independent broker-dealer to hybrid IBD slash RIA.

Prince Rogers Nelson’s death at age 57 was tragic, and the tragedy compounded when it became clear the superstar musician didn’t have an estate plan. With proactive legal and financialadvice, the conflict over his name and likeness, large tax bill, and lengthy settlement process wouldn’t have been a foregone conclusion.

The Transparent Advisor Movement’s mission is to promote ideals of clarity, modesty, integrity, dignity, and client advocacy in all aspects of financialadvice, with a special focus on Advice Only, Flat Fee, and Hourly service models. If yes… Join the Transparency Advisor Movement. Yeah, you have a short fall.

We’ll discuss these questions: The CFP Board has specifically stated that it wants the CFP® mark to be a requirement for anyone who practices financialplanning. The debaters are: Robert Wright, CFP®, a financial consultant with Advocacy Wealth Management. What is your opinion? Robert will be on the “for” team.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content