This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Investors have faced a host of financial challenges over the past year—from record inflation, to rising interest rates, to market corrections and rebounds. So it’s no wonder that many investors who are not yet retired are recalibrating their expectations for retirement and their financial future.

How will elections affect the economy? These are all interesting and important questions, but preparation for retirement is much more important than panicking over issues you have no control over. For many investors, however, the more important questions to ask and answer relate to your retirement strategy. default on its debt?

That’s why at Nationwide Financial, we gather and share insights from our in-house thought leaders to help simplify what’s happening in the economy to help financial professionals shed light on potential opportunities in the financialmarkets. What will inflation do to my savings?

Upcoming Webinar – February 22nd at 12:00pm PST Volatility has spiked due to changing concerns over inflation, interest rates, recession fears, geopolitics, and other fear-provoking issues, but how can you grow and protect your retirement nest egg? Learn how to avoid these missteps and expand your wealth.

Plus, just months ago, A YouGov survey found that 60% of Americans prioritize trustworthiness as the most important factor when selecting a financial advisor. So, if its about trust, then we should study 5 of the most proven digital marketing strategies for financial advisors that are being used right now to win in the trust-economy.

Individual investors are more anxious for the Fed to start easing rates; a recent Advisor Authority survey, powered by the Nationwide Retirement Institute, found that nearly 40% of individuals want the Fed to begin cutting interest rates to help relieve economic pressures.

economy appears to be in the late stage of expansion, with strong economic activity but labor and supply chains remain constrained. The labor market is very tight, with a low unemployment rate of 3.7% As of this writing, market expectations call for a path of Fed rate hikes to a range of 5.0-5.25%, Responding to recession risks.

Top Marketing Trends for Financial Advisors in 2023 via Advisorpedia In any industry, if you want to stay ahead of the curve, then it’s important that you’re keeping up with trends. And that goes for financialmarketing, as well! You help clients to set financial goals, plan for retirement and much more.

The Significance Of Financial Compliance Financial compliance requires all actions, procedures, guidelines, and business culture to abide by the rules and regulations set by the regulatory authorities of the financialmarket.

A hedge fund is a type of investment fund that uses financial instruments to offset the risk of investments. Hedge fund managers use their knowledge of the financialmarkets to manage their investment objectives, liquidity, and risk. Financial advisors help people invest their money after learning about their financial goals.

If you can time the economy, you can time the stock market. I am not suggesting home ownership is bad in any way, but there is this idea that you buy a house, sell it after thirty years, take your gains and retire to a beach. Okay, this one is actually more true than I thought it would be before I looked at the data.

It has to be such a different set, the retirement planning is different, the safety net is different. First of all, I think the amount of investors that participate in the financialmarkets is much smaller than it is in the U.S. And I think that the financial advisors are used, but not as widely used as they are in the U.S.

Taking steps to help ensure you’re reasonably prepared for any type of economic uncertainty or recession, personal financial crisis (loss of a job, divorce, medical expenses, etc.), or downturn in the financialmarkets that could occur at any time is just common sense. So many things to say here.

The Standard & Poor’s 500, more commonly known as the S&P 500, is a stock market index that was launched by its eponymous credit agency in 1957. An index is a way to track the overall performance of a financialmarket by looking at a collection of different investments – in this case, stocks. Consumer staples .

Just imagine what unknown leaky costs on your investments could mean for your retirement. Do you want high or unknown investment fees to delay your retirement by years? Focus on lower costs because quite simply, the less you pay, the more you keep, and the earlier you can retire. I think not. www.Sidoxia.com Wade W.

They are characterized by rapid economic growth and increasing integration with the global economy. Emerging marketeconomies represent the transition phase between developing and developed nations. Such growth can translate into substantial returns on investment, making these markets attractive for wealth accumulation.

At times, it seems like this is the only issue on the minds of market prognosticators and TV’s talking heads. As shown in the chart on page 2, even the slightest hint of a possible move from the Fed can trigger a financialmarket reaction. bond and stock markets have been relatively stable. Higher rates in the U.S.

It also encompasses intended lifestyle, charitable giving, retirement and estate planning, and liabilities, including anticipated costs for health care. During times of market volatility, such long-term planning enables clients to shake off an impulse to sell. Diamonds In The Rough. By Tom Graff, CFA, Head of Fixed Income.

In his recent work, “ Chaos is a friend of mine ,” financial columnist Bob Seawright points to a range of historical events demonstrating why complex adaptive systems like financialmarkets are essentially unpredictable. This brings our report to a wrap.

While concerns about the debt ceiling have been increasing, markets, businesses, and the economy are likely to see only minimal impact until we are days, or maybe a few weeks, from the “x date,” the date on which the federal government will no longer be able to meet all its obligations, likely in the summer or early fall.

As the world continues to recover from the pandemic and economies stabilize, the investment landscape is evolving rapidly. It is important to consider your personal financial goals and needs before making any financial decision about such a large sum of money. Need a financial advisor?

There was an exceptional item related to the employee’s retirement settlement expenses and foreign currency translation reserve as per the Ind AS framework. With more movement of goods from import and export coupled with a growing economy, it stands to gain. Meanwhile, PAT Margins have improved from 26% in FY23 to 30% in FY24.

The entire economy, the world of investing, is based upon being able to trust who we are listening to. Helping parents send their kids to college, care for an aging parent and retire with financial independence are literally what gets him up every day. Scott has been serving families for 29 years in the financial services space.

Following the financial crisis and the Fed cutting rates, economy and the market starts recovering in late 2009 and then 2010 and we kept hearing from a lot of different value corners, hey, everything is richly priced. There’s old and there’s old but there’s not both. Bonds are the most expensive.

Growth and change in the securities markets over the past 100 years or so has resulted in management’s becoming more and more distanced from the ultimate owners of public companies—individuals. Still, one cannot ignore the number of private companies that have achieved meaningful size and scale in today’s relatively sluggish economy.

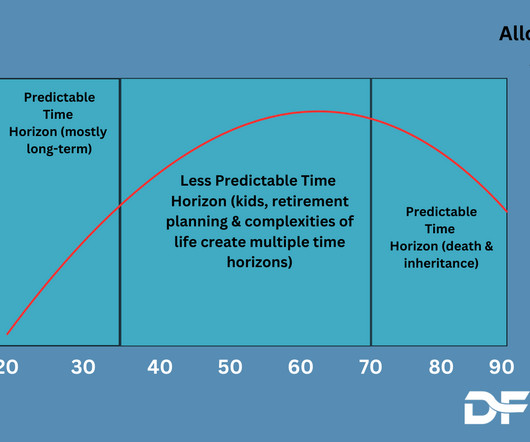

Tariffs and trade wars are the equivalent of putting boulders in your own harbors thinking you’ve made your economy more accessible to everyone when all you’ve really done is make things more difficult for everyone. As you may or may not know – I have an obsession about time within financial planning processes.

Cato Institute ) • The Evolution of Retirement : No one knows precisely how much to save for multiple decades into the future. No one knows what financialmarket returns or interest rates or inflation will be going forward. In June 2022, he said “we need 5 years of unemployment above 5% to contain inflation, 2 years of 7.5%

We ended up buying, this is one of the wonderful things about financialmarkets and degrees of completeness. There’s a continual, the economy continues to grow. People earn wages, whether it’s a retirement account or a tax deferred account or just an investment account. That’s amazing leverage.

He brings a fascinating approach and a bit of an outlier, contrarian way of looking at the world that has allowed him to identify specific changes in what’s taking place in the economy, in the markets, and essentially provide a helpful sounding board to many of the world’s best investors. Simple answer, demographics.

I didn’t think I would be necessarily doing what I’m doing today, but I knew that I was gonna be interested in financialmarkets of some kind, and I think I probably ended up in the right place. I don’t even know what it’s going to be yet, but I mean, I’m not retiring. So I, I went to school.

My theory is post great financial crisis, mom and pop said, “You know, we’re done playing this game.”. Let Mr. Market do his thing and we’ll find out how we did when we get ready to retire. We have mutual funds now; they’re not going to go anywhere because they’re baked into our retirement system.

It’s the rules of the game for the economy and they affect all companies. ADMATI: So, the use of debt to fund things, meaning I give you money, then I get an IOU from you, OK, is pervasive throughout the economy. It is well known that tax bias of debt over equity is a distortion in the economy.

Typical thinking – thinking that should be cast to the dustbin of history – fails to grasp the complexity and dynamic nature of financialmarkets. The financialmarkets are simply too complex and too adaptive to be readily predicted. Those who cannot, should and will fall by the wayside.

As we write this letter, financialmarkets are grappling with plenty of controversy and uncertainty, from the aftershocks of the dramatic fall in oil prices, to the potential impact of a British exit from the EU, to the implications of the pending U.S. Maximize retirement plan contributions. Midyear Planning Tools for 2016.

Source: The Financial Times (FT) Dumb Rules of Thumb Wall Street is notorious for providing rules of thumb and shortcuts for the masses, but if investing was that easy, I’d be retired on my private island consuming copious amounts of coconut drinks with tiny umbrellas.

trillion into the economy in addition to the $4.1 In 1998, the then-future Nobel laureate Paul Krugman made a remarkable and erroneous prediction : “By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s.” Inflation was already hot.

Your real business is having the best perspective of what is happening this moment in the economy. 00:17:41 [Speaker Changed] So you’re getting like a real time snapshot of what’s happening, not just across the economy but within very specific subs sectors. Your side hustle. Hustle was managing institutional right assets.

The Fed’s goal is to inflict quick, near-term pain on the economy in exchange for long-term price stability and future economic gains. With these kind of drops, a mild-to-moderate recession is already baked into the cake, even though the economy is expected to grow for the next four quarters and for all of 2023 (see GDP forecasts below ).

There are few people in the world who understand the interrelationships between central banks, the economy, and markets like Bill Dudley does this, this is just a master class in, in understanding all the factors that affect everything from the economy to inflation, to the labor market, the housing market, and of course, federal Reserve policy.

The transcript from this weeks, MiB: Apollo’s Torsten Slok on the US Economy & Trump 2.0 , is below. You know, most of the economists that you’re probably familiar with haven’t really had a good handle on the state of the economy over the past couple of years. He was just on such a roll.

And few do it better than Neil does in terms of putting together a global view of what’s happening in the economy, what’s happening around the world, what’s happening with the Fed, and what’s happening with the stock market. DUTTA: Well, it means that they’re going to push the economy into recession.

The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow. If you are one of the people who thinks the stock market is too high, then you should definitely ignore Warren Buffett, arguably the greatest investor of all-time. growth during the 4th quarter of 2023 (see chart below).

Traditional market analysis has generally failed to grasp the inherent complexity and dynamic nature of the financialmarkets, which chaotic reality goes a long way towards explaining highly remarkable and volatile outcomes that seem inevitable in retrospect but were predicted by almost nobody. How will the market perform?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content