This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Everyone reading this understands the benefits of someone starting to invest for their retirement when they are in their 20’s vs. their 50’s. Although young investors might see some monetary gains from their investments when they’re in their 30’s, it most likely is not enough money to finally retire from work. Some of the advisors that we work with at AdvisorPR discuss how many people give in to instant gratification and spend their money on everything from lattes to a fancy car rather than save

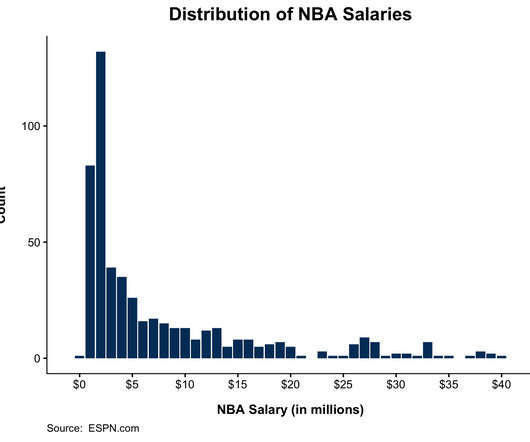

There are just over 130 million full-time workers in the United States and not a single one of them thinks they're overpaid. This holds for people all over the income pool and paradoxically, is especially true for people towards the top of the ladder.* It sounds absurd, but a person making $1 million can feel more stress over money than someone making $100,000 because the more you make, the easier it is to let your spending spiral out of control.

Speaking as someone who has spent hundreds of hours helping financial advisors generate reliable, qualified leads over the years, I understand first-hand what an important goal this is for many people. I also understand that there’s no “one right way” in which to do it – every business is unique and you need the type of strategy that will play directly into that fact, broadcasting exactly what it is that makes you unique to the widest possible audience.

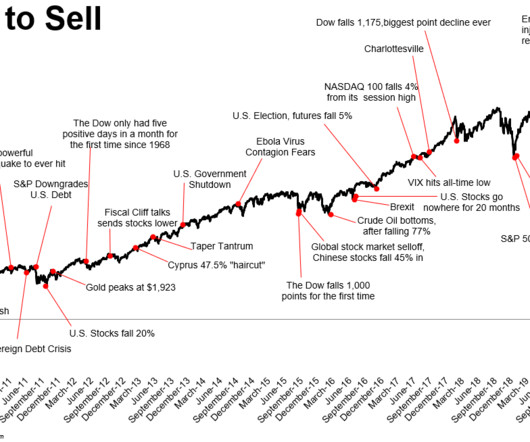

When I sat down this morning* to create a “Wall of Worry” chart, the hard part wasn’t coming up with the list, but rather choosing what to leave off. Since the stock market bottomed in 2009, there have been so many potential reasons to sell that it wasn’t possible to fit them all on the chart. Below are a few that didn’t make the cut: MF Global Bankruptcy All the quantitative easing programs Ashton Kutcher is a venture capitalist China hard landing(s) CAPE ratio Occupy Wall Street Mike Tyson rep

As businesses increasingly adopt automation, finance leaders must navigate the delicate balance between technology and human expertise. This webinar explores the critical role of human oversight in accounts payable (AP) automation and how a people-centric approach can drive better financial performance. Join us for an insightful discussion on how integrating human expertise into automated workflows enhances decision-making, reduces fraud risks, strengthens vendor relationships, and accelerates R

Today’s Animal Spirits is brought to you by YCharts. Mention Animal Spirits to receive 20% off (*New YCharts users only) Listen here On today’s show we discuss Ben's new book, buy it here! Zero fee commissions Why there's little enthusiasm for this bull market JPM Guide to the Markets The middle class is slowly going away WeRamp Millennials have how much in their 401(k) The aging of America 74% of people have a budget, ya right People aren't driving as much as they used to Millennials approve

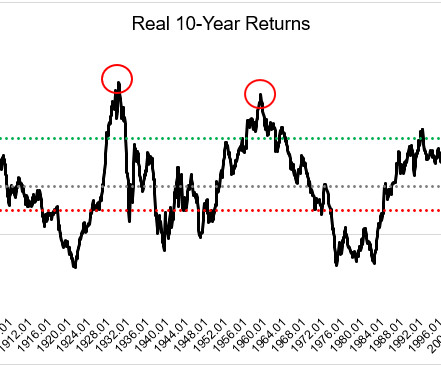

Performance is one of the most mean-reverting data sets in the financial universe*. What goes up must come down and what goes down sometimes comes back up, eventually. For example, real 10-year returns for U.S. stocks going back to 1900, have averaged 6.5%. (gray line) When 10-year returns have been twice the average, forward ten-year returns fall to just 3%.

Articles Progress happens too slowly to notice while setbacks happen too quickly to overlook By Morgan Housel Investing is overrated By Christine Benz Unremarkable kids no longer have access to remarkable opportunities By Scott Galloway A commitment to raising my savings and investment rate By Josh Brown Change is gonna come. By Bob Seawright They’re like NFL Offensive Lineman.

Articles Progress happens too slowly to notice while setbacks happen too quickly to overlook By Morgan Housel Investing is overrated By Christine Benz Unremarkable kids no longer have access to remarkable opportunities By Scott Galloway A commitment to raising my savings and investment rate By Josh Brown Change is gonna come. By Bob Seawright They’re like NFL Offensive Lineman.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content