This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

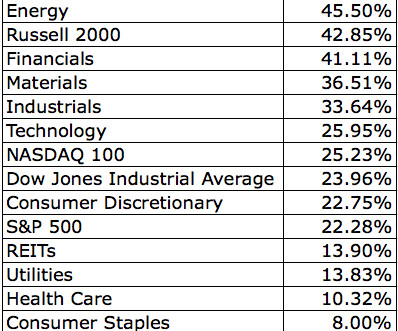

For the last 35 years, the classic 60/40 portfolio returned 10.5% a year. It's hard to imagine that these results will be matched over the next 35 years, which has a lot of people looking to alternative ways of managing a portfolio. Today I'm going to examine one of these alternatives, the "Permanent Portfolio," which was outlined in William Bernstein's "Deep Risk" (and elsewhere).

Making More From Less. achen. Tue, 11/29/2016 - 14:44. The directors at many nonprofits today are finding that, by some measures, working for the common good has never been so tough. The budget gap for nonprofits has widened because of a slump in their three sources of funds—donations, grants and portfolio returns. Charitable giving to foundations in 2015 shrank 3.8% from the previous year to $42.3 billion, according to Giving USA. 1 Also, from fiscal year 2009 until fiscal year 2016, federal ag

The costliest mistake 2% investors make is timing the market. They sell after losses and buy back only when the coast is clear. The problem is not just the money you leave on the table this time, but these mistakes leave behind scar tissue that compounds in our brains. It doesn't take long before we're unable to think objectively. Rather than viewing a buy/sell decision as independent from all others, we think about the outcome of previous mistakes and the regret we felt after buying or selling

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content