This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We all love to use quotations in our arguments. It’s both an appeal to higher authority as well as social proof ( Hey! I’m not the only one who believes this stuff ). I find it useful occasionally to go back to first principles and reconsider the sources that have influenced my thinmking. Along those lines, here are in chronological order, the thinkers who have helped shape how I view the world view, including how I philosophically think about the economy, markets, and investing.

You know Hancock and Washington and Franklin and Jefferson. You might even know Greene and Knox, Henry and Hale. And we know you know Hamilton, pretty tough to escape that one these days! But it is very unlikely that you know the name Haym Solomon. This is unfortunate, because he’s the guy who arranged financing to keep the Continental Army alive during its darkest days, finding the money to keep the revolution goin.

Stocks Remain Strong Stocks took a break last week, which was perfectly normal after a five-week win streak coming off the late-October lows. It is important to remember that stocks lead the economy, both on the way up and the way down. Various indexes are closing in on new all-time highs, and one of the most important indexes in the world is already there.

Personal finance was my first love in the money world. I was a saver before I ever knew what investing even was. Yet my relationship with personal finance has evolved as I’ve aged and changed my habits. Many of the personal finance rules written in stone will always apply. Live below your means. Pay yourself first. Stay out of credit card debt.

As businesses increasingly adopt automation, finance leaders must navigate the delicate balance between technology and human expertise. This webinar explores the critical role of human oversight in accounts payable (AP) automation and how a people-centric approach can drive better financial performance. Join us for an insightful discussion on how integrating human expertise into automated workflows enhances decision-making, reduces fraud risks, strengthens vendor relationships, and accelerates R

“When I see a bubble forming I rush in to buy, adding fuel to the fire. That is not irrational.” – George Soros, 2009 I’ve spent 25 years watching, trading and investing in the stock market. The repetition of patterns is amazing. In every generation we see new bubbles, which form when a new innovation comes along and everyone gets excited about the future.

Last year was one of the worst years ever for financial markets. Call it recency or loss aversion or some other Daniel Kahneman bias but for some reason, our brains are hard-wired to assume big losses will be followed by additional losses (just like we assume big gains will be followed by additional gains).1 The thing about big losses in the stock market is sometimes they are followed by big losses…but sometimes t.

By Mark N. Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). This will mean: · Elimination of the state and local tax cap of $10,000 · The return of other itemized deductions in 2026 · Reversion of individua

By Mark N. Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). This will mean: · Elimination of the state and local tax cap of $10,000 · The return of other itemized deductions in 2026 · Reversion of individua

One of my favorite responsibilities as chief investment officer at Ritholtz Wealth Management is the quarterly conference call I do for our clients. I run through 30 charts in 30 minutes that explain where we are in the economic cycle, what markets are doing, and what it means to their portfolios. I like to finish with a thought-provoking, often “investing-adjacent” idea they might not have previously considered.

The AI craze is in full effect so everyone is trying to figure out who the winners will be. Maybe it will be the upstarts, some new start-up that gives you your own personal assistant in your ear, on your iPhone and at your desk. Or maybe it will be the big tech players who have gobs of money to throw at AI like Microsoft, Google and Facebook. Maybe it’s a company like NVIDIA that supplies the chips and software.

From Black Knight: Black Knight: Past-Due Mortgages Approach Recent Record Lows as Serious Delinquencies Continue Improvement; Prepayments See Seasonal Rise • Reversing much of April’s calendar-driven spike, the national delinquency rate fell 11 basis points (bps) in May to hit 3.10% – the lowest it’s been other than March 2023’s record of 2.92% • The number of borrowers a single payment past due improved by 94K (-9.5%), erasing nearly half of the prior month’s increase • Serious delinquencies (

Based off SkyStem's popular e-Book, the book of secrets to the month-end close will be revealed in this one-hour webinar. Learn leading practices when it comes to building a strong and sustainable month-end close that has room to grow and evolve. Learn about the power of precise estimates, why reconciliations are critical to closing the books, how and when to automate, and how the chart of accounts play into your close process.

Ladies and gentlemen, this is the final post I will be publishing at The Reformed Broker. After today the site will be inactive, forever. I began this blog in November 2008 without any idea where it would take me. I had a negative net worth, was working at a dead-end brokerage firm job and absolutely no career prospects whatsoever – a washed up stock broker at 31 years old in the middle of a global financial crisis.

SoFi Securities, SogoTrade, M1 Finance and Open to the Public Investing will pay more than $1 million in restitution after clients were promised fees from lending securities they allegedly never received.

The DOL reported : In the week ending June 17, the advance figure for seasonally adjusted initial claims was 264,000 , unchanged from the previous week's revised level. The previous week's level was revised up by 2,000 from 262,000 to 264,000. The 4-week moving average was 255,750, an increase of 8,500 from the previous week's revised average. This is the highest level for this average since November 13, 2021 when it was 260,000.

Altos reports that active single-family inventory was up 1.5% week-over-week. Click on graph for larger image. This inventory graph is courtesy of Altos Research. As of June 9th, inventory was at 443 thousand (7-day average), compared to 436 thousand the prior week. Year-to-date, inventory is down 9.7%. And inventory is up 9.3% from the seasonal bottom eight weeks ago.

Like being inches from the end zone, many advisors are frustratingly close to their next level of success. You work hard. You put in the hours. But if your closing rate is stuck or your pipeline feels like a revolving door… something has to change. Most advisors are just one small shift away from dramatically increasing their revenue. The difference?

From CoreLogic: CoreLogic: US Home Borrowers See First Annual Home Equity Losses Since 2012 in Q1 2023, but Overall Mortgage Performance Remains Strong CoreLogic®. today released the Homeowner Equity Report (HER) for the first quarter of 2023. The report shows that U.S. homeowners with mortgages (which account for roughly 63% of all properties) saw home equity decrease by 0.7% year over year, representing a collective loss of $108.4 billion, and an average loss of $5,400 per borrower since the f

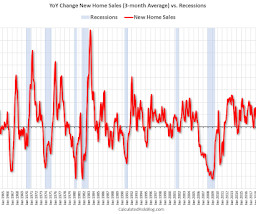

The Census Bureau reports New Home Sales in May were at a seasonally adjusted annual rate (SAAR) of 763 thousand. The previous three months were revised down slightly, combined. Sales of new single‐family houses in May 2023 were at a seasonally adjusted annual rate of 763,000 , according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

Way back in 2013, I wrote a post " Predicting the Next Recession. In that 2013 post, I wrote: The next recession will probably be caused by one of the following (from least likely to most likely): 3) An exogenous event such as a pandemic , significant military conflict, disruption of energy supplies for any reason, a major natural disaster (meteor strike, super volcano, etc), and a number of other low probability reasons.

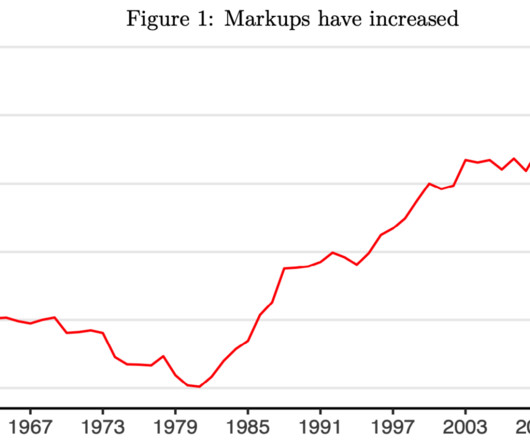

Over at Alphaville , Robin Wigglesworth looks at whether ‘Greedflation’ (aka price-gouging) meaningfully contributed to Eurozone inflation. Specifically, Bank of England research suggests that while they “find no evidence of a rise in overall profits in the UK” they did notice that “companies in the oil, gas and mining sectors have bucked the trend” with “some companies… much more profitable than others.”1 I was pretty skeptical about Greedflation initia

Managing spend is more than a cost cutting exercise – it's a pathway to smarter decisions that unlock efficiency and drive growth. By understanding and refining the spending process, financial leaders can empower their organizations to achieve more with less. Explore the art of balancing financial control with operational growth. From uncovering hidden inefficiencies to designing workflows that scale your business, we’ll share strategies to align your organization’s spending with its strategic g

Imagine you had a device that allowed you to peer into the future. You enter a subject matter into this machine, requesting a specific quantitative measure, and at a specific future time. In other words, Price and Date. The machine whirrs and spins, lights flash, bells ring, and out pops a chart showing a range of answers and their probabilities. You might imagine a machine like that would be worth a lot.

I have been writing about issues with the minimum wage for (it seems like) decades. During that time, consuming lots of academic research, I reached a few logically supported conclusions. The least contentious of which is that modest increases in minimum wages increase economic activity and create jobs. But there are other surprises around the minimum wage.

Here a few measures of inflation: The first graph is the one Fed Chair Powell has been mentioning. Click on graph for larger image. This graph shows the YoY price change for Services and Services less rent of shelter through March 2023. Services were up 6.8% YoY as of April 2023, down from 7.2% YoY in March. Services less rent of shelter was up 5.2% YoY in April, down from 6.1% YoY in March.

From the Federal Reserve: The April 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices The April 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months, which generally correspond to the first quarter of 2023.

Speaker: Duke Heninger, Partner and Fractional CFO at Ampleo & Creator of CFO System

Are you ready to elevate your accounting processes for 2025? 🚀 Join us for an exclusive webinar led by Duke Heninger, a seasoned fractional CFO and CPA passionate about transforming back-office operations for finance teams. This session will cover critical best practices and process improvements tailored specifically for accounting professionals.

The Census Bureau reports New Home Sales in March were at a seasonally adjusted annual rate (SAAR) of 683 thousand. The previous three months were revised down slightly, combined. Sales of new single‐family houses in March 2023 were at a seasonally adjusted annual rate of 683,000 , according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

Nine years ago, I wrote: Census Bureau: Largest 5-year Population Cohort is now the "20 to 24" Age Group. Earliler the Census Bureau released the population estimates for July 2022 by age, and I've updated the table from the previous post. The table below shows the top 10 cohorts by size for 2010, 2022 (released recently), and the most recent Census Bureau projections for 2030.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Sabrina Speianu: Weekly Housing Trends View — Data Week Ending Apr 1, 2023 • Active inventory growth continued to climb, but at a lower rate, with for-sale homes up 53% above one year ago. The inventory of for-sale homes rose compared to last year, but at a slower pace than the previous week for a third time in a row as a smaller number of hopeful homebuyers still outnumber new se

Here is another monthly update on framing lumber prices. This graph shows CME random length framing futures through March 3rd. Lumber is currently at $369 per 1000 board feet. This is down from the peak of $1,733, and down 72% from $1,441 a year ago. Prices are down 8% compared to the same week in 2019, and below the pre-pandemic levels of around $400.

Join this insightful webinar with industry expert Abdi Ali, who will discuss the challenges that can arise from managing lease accounting with spreadsheets! He will share real-world examples of errors, compliance issues, and risks that may be present within your spreadsheets. Learn how these tools, while useful, can sometimes lead to inefficiencies that affect your time, resources, and peace of mind.

Here is a graph of the year-over-year change in shelter from the CPI report and housing from the PCE report this morning, both through May 2023. CPI Shelter was up 8.0% year-over-year in May, down from 8.1% in April, and down from the cycle peak of 8.2% in March 2023. Housing (PCE) was up 8.3% YoY in May , down from 8.4% in April (April was the cycle peak).

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from chief economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Apr 15, 2023 • Active inventory growth continued to climb, with for-sale homes up 49% above one year ago. The number of homeowners shifting home listing timelines around spring holidays helped push active inventory growth up this week.

Just wanted to take a moment to recognize the incredible work my media and research teams have been doing to propel The Compound channel past 120,000 subscribers this month. And that 120k is just a fragment of the audience because almost everything we do on video is also on the audio podcast channels too. For those who are new to what we’re doing at the Compound YouTube channel each week, below is the schedule of w.

From the Census Bureau: Permits, Starts and Completions Housing Starts: Privately‐owned housing starts in February were at a seasonally adjusted annual rate of 1,450,000. This is 9.8 percent above the revised January estimate of 1,321,000, but is 18.4 percent below the February 2022 rate of 1,777,000. Single‐family housing starts in February were at a rate of 830,000; this is 1.1 percent above the revised January figure of 821,000.

As we step into 2024, the lending landscape evolves rapidly with technology, regulations, and market dynamics driving change. For banks and financial institutions to stay competitive and meet the evolving needs of their customers, these drivers must be understood and engaged with. Lenders can anticipate significant transformation fueled by technological advancements, regulatory shifts, and changing consumer behaviors.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content