This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

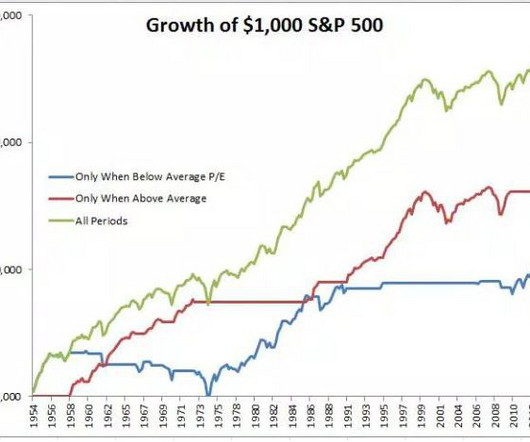

Last week I asked the question "what if you only invested in stocks when they were cheap?" The chart below got a lot of scrutiny, understandably so. It's hard to believe that stocks did better when they were above their average valuation versus when they were below. I'm happy to chow on some crow here, the chart below is indeed greatly flawed. I think the message I was trying to convey got lost in translation, so I wanted to take the opportunity to address this.

TEDxWilmington | Sustainable Investing: What you didn't know could make you money. ajackson. Sat, 12/05/2015 - 08:00. This talk was given at a TEDx event using the TED conference format but independently organized by a local community. Learn more at [link].

Nobody likes to overpay, whether it's for food, clothing, a house, or stocks. The problem is people don't treat stocks the way they do a car, groceries, or jeans. If a cucumber goes from $2 to $10, you wouldn't say "wow, I need to buy some before it goes to $20." You would simply substitute it for another vegetable. However, if a stock rose 400% there are plenty of people who would pile on, anticipating a greater fool will come along after them.

Wow, this year went really fast. It feels like just yesterday that the Fed finally decided to raise rates. I wanted to share some of my favorite things from 2015. Podcast: I am lucky to be able to help Barry prepare for Master's in Business. Some guests I'm more excited about than others. I would put Ken Feinberg in the "others" category. I was wrong.

As businesses increasingly adopt automation, finance leaders must navigate the delicate balance between technology and human expertise. This webinar explores the critical role of human oversight in accounts payable (AP) automation and how a people-centric approach can drive better financial performance. Join us for an insightful discussion on how integrating human expertise into automated workflows enhances decision-making, reduces fraud risks, strengthens vendor relationships, and accelerates R

"There is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again" - Jesse Livermore Long before Cliff Asness wrote his dissertation on momentum, Alfred Cowles and Herbert Jones discovered that stocks tended to move in the direction in which they came from.

As we await for the inevitable(?) first rate hike since 2006, let's take a moment to review what type of year it's been for U.S. Stocks. The S&P 500 has done a whole lot of nothing this year and currently is up just 0.04%. Looking at this minuscule number helps clarify what we already know, that so much of the day-to-day stuff on the screen and on TV is just noise.

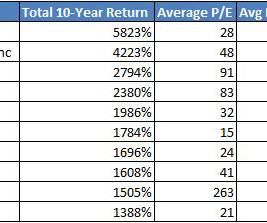

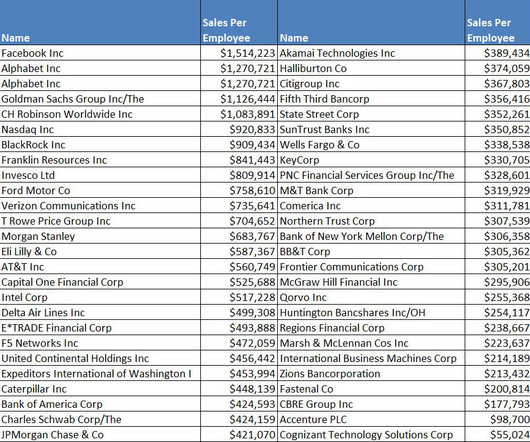

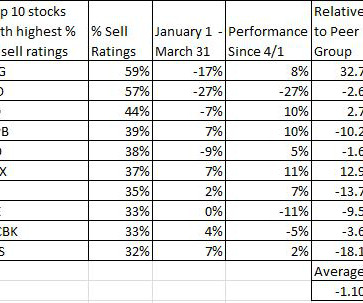

The other day I looked at a common theme among the decade's biggest winners; they tended to be very expensive relative to their peers based on traditional valuation metrics. Today I want to look at another trait these winners share, volatility and big drawdowns. A few things really stand out in this table. Nine of the ten biggest winners were all cut in half.

The other day I looked at a common theme among the decade's biggest winners; they tended to be very expensive relative to their peers based on traditional valuation metrics. Today I want to look at another trait these winners share, volatility and big drawdowns. A few things really stand out in this table. Nine of the ten biggest winners were all cut in half.

One of the common themes among the very best performing stocks is that they are attached to a high price-to-earnings ratio. It makes sense that the fastest growing companies deserve a higher multiple than the average stock. You'll notice in the table below that nine out of ten of the strongest stocks over the past decade traded at a higher average multiple than the S&P 500.

It's one thing to call a trade, it's another thing entirely to profit off that call. First, there's the issue of timing. Then you have to be able to execute; when to get in, press your bet, take profits, etc. The excerpt below is from Gregory Zuckerman's The Greatest Trade Ever (emphasis mine). Investment advisor Peter Schiff seemed in an ideal position to benefit from real estate troubles.

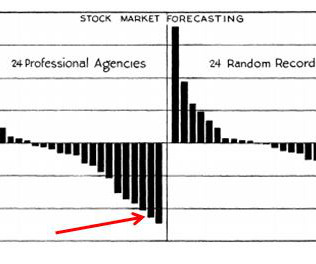

Long before Jim Cramer's record was being dissected, Alfred Cowles was skeptical of the claims made by stock market pundits. Cowles, who later founded the Cowles Foundation for Research and Economics , spent years working on a paper published in 1933, "Can Stock Market Forecasters Forecast? His mission: "It seemed a plausible assumption that if we could demonstrate the existence in individuals or organizations of the ability to foretell the elusive fluctuations, either of particular stocks, or

Ensuring Legacies Last. achen. Wed, 12/02/2015 - 10:29. Heirs who are unprepared for an inheritance may find that a big windfall can quickly become a mixed blessing. An essential step in estate planning is making sure beneficiaries know all the responsibilities and challenges that accompany the management of increasing wealth. When an aging parent with an air-tight estate plan fails to prepare heirs for an inheritance, an act of kindness runs a high risk of backfire.

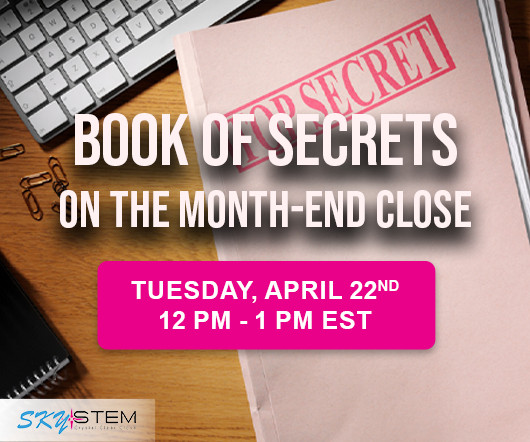

Based off SkyStem's popular e-Book, the book of secrets to the month-end close will be revealed in this one-hour webinar. Learn leading practices when it comes to building a strong and sustainable month-end close that has room to grow and evolve. Learn about the power of precise estimates, why reconciliations are critical to closing the books, how and when to automate, and how the chart of accounts play into your close process.

Anchoring Expectations. achen. Wed, 12/02/2015 - 12:50. Stock market corrections can prompt investors to impulse selling or other moves that are often harmful to their long-term financial well-being. By walking through four steps with a client, we can refocus his or her mindset on the fundamental issues that help safeguard financial stability and achieve steady outperformance.

Diamonds In The Rough. achen. Wed, 12/02/2015 - 12:58. Weak commodity prices and flagging emerging market economies have dimmed the outlook for energy and metals companies, and are shaking up the high-yield bond market. Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn.

There has been a lot of talk lately about the lack of participation; how only a few stocks are actually rewarding shareholders while so many have been burning them. Winners have been few and far between but it's not as if the index is exactly on fire. While it's true that without Amazon and Google the market would be down, even with them, the S&P 500 is only up 1.5% for the year.

I tend to be on the skeptical side when it comes to investing based on seasonal trends. I'm almost always of the mind that less is more and seasonality encourages more decision making, not less. Making changes to your portfolio based on this type of study would probably not be in your best interest when taking into consideration taxes, transaction costs, and most importantly, the cost of being wrong.

Like being inches from the end zone, many advisors are frustratingly close to their next level of success. You work hard. You put in the hours. But if your closing rate is stuck or your pipeline feels like a revolving door… something has to change. Most advisors are just one small shift away from dramatically increasing their revenue. The difference?

John Bogle, Cliff Asness, and Ray Dalio are just a few of the juggernauts that have recently been vocal about expecting lower returns. What is an advisor supposed to do when people like this are all on the same side of a very important issue? Here are a few ideas: Lower your expectations, literally. In the financial plan, you can lower expected returns and or adjust inflation upward.

Cliff Asness is out with a new interesting paper, "Market Timing Is Back In The Hunt For Investors." In it, he discusses the efficacy of using valuations, specifically the CAPE ratio, to help time the market. One thing Asness addresses is the valuation drift upward which U.S. stocks have experienced over the last century. Here's Cliff: "As alluded to earlier when discussing the long-term upward drift in CAPE, another related but distinct headwind for contrarian stock market timing in the second

Strategic Advisory Letter | 2015 Year-End Planning Checklist. achen. Thu, 11/12/2015 - 11:10. As 2015 comes to a close, we remind our clients and friends of how important it is take time to review new tax rules, consider tax-saving opportunities and review investment and asset-protection plans before year’s end. As autumn rolls on and the holiday season approaches, it is once again time to consider a thorough review of your overall financial picture and your progress toward your long-term object

"Magicians are the most honest people in the world. They tell you they're gonna fool you, and then they do it." -James Randi I recently watched "An Honest Liar" on Netflix, which is the story of The Amazing Randi, a magician and escape artist who dedicated his life to unveiling the charlatans. He went on a crusade, targeting the psychics and faith healers and exposed them for the con artists that they were.

Managing spend is more than a cost cutting exercise – it's a pathway to smarter decisions that unlock efficiency and drive growth. By understanding and refining the spending process, financial leaders can empower their organizations to achieve more with less. Explore the art of balancing financial control with operational growth. From uncovering hidden inefficiencies to designing workflows that scale your business, we’ll share strategies to align your organization’s spending with its strategic g

The largest gains are enjoyed by investors with the longest time horizons. Let's take Amazon, obviously an extreme example. From the time of its IPO through the end of 2014, Amazon gained 12,600%. Even after such a remarkable run, Amazon is up over 100% through the first ten months of this year! However, the reality is having any sort of risk management would make it all but impossible to enjoy these outsized returns as even the best performing stocks have experienced massive drawdowns.

The Great Crash 1929 by John Kenneth Galbraith was poetically published in 1954, the first year that stocks would eclipse their 1929 highs. One of the most enjoyable aspects of reading about events that shaped history is getting a better sense of what actually happened. Ninety years later, the stories tend to morph into something a few steps farther than reality.

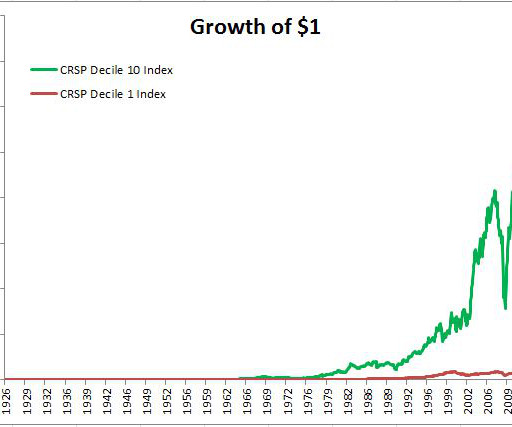

This is the small cap secret no one ever told you; You've probably heard about the small stock premium, the idea that over long periods of time, small stocks outperform large stocks. There are a bunch of different theories as to why this is the case. Some believe the additional returns are compensation for decreased liquidity, additional volatility, or both.

From 1929 through 1932, the Dow Jones Industrial Average would lose nearly ninety percent of its value. In this four year period, there were several nasty bear market rallies, lifting the hopes of the hopeful, only to be met with tidal waves of selling. Corporations were collapsing and individuals didn't fare much better. Unemployment in the United States was 25% and U.S.

Speaker: Duke Heninger, Partner and Fractional CFO at Ampleo & Creator of CFO System

Are you ready to elevate your accounting processes for 2025? 🚀 Join us for an exclusive webinar led by Duke Heninger, a seasoned fractional CFO and CPA passionate about transforming back-office operations for finance teams. This session will cover critical best practices and process improvements tailored specifically for accounting professionals.

Are the owners of great track records incredibly skilled, or incredibly lucky? This is one of the oldest questions in finance. To explore this further, I'm going to borrow from Scott Patterson and Jack Schwager, the authors of two fantastic books, The Quants and Market Wizards. Here is Gene Fama, Nobel Laureate, the father of modern finance and longtime professor at the University of Chicago, talking to a classroom of students (The Quants, pages 77-79).

Brattle St Capital is one of my favorite follows on Twitter. He's constantly sharing interesting data, quotes and other valuable investing insights. The fact that he's doing so anonymously, in which he receives no personal recognition, makes it that much more awesome. Yesterday, he offered some lousy investment theses, learned through experience, which I wanted to share.

Fama and French wrote "The Cross-Section of Expected Stock Returns" in 1992, unveiling their three-factor model. They expanded on CAPM, which boils down stock returns to just one factor, beta. Fama and French took this a step further, finding that the vast majority of a stocks returns can be explained not just by beta, but by size and book-t0-market as well.

At sub two percent on the ten-year treasury, many investors are questioning why bother owning bonds at all. As ninety percent of the returns are derived from the starting interest rate, it's fair to assume that bonds will indeed offer measly returns going forward. While it's not realistic to expect the returns of the last thirty years to continue, I still see great merit to holding bonds in a diversified portfolio.

Join this insightful webinar with industry expert Abdi Ali, who will discuss the challenges that can arise from managing lease accounting with spreadsheets! He will share real-world examples of errors, compliance issues, and risks that may be present within your spreadsheets. Learn how these tools, while useful, can sometimes lead to inefficiencies that affect your time, resources, and peace of mind.

The last few days and weeks are a great reminder of how difficult it is to successfully trade stocks. There's a reason why there aren't many traders that are household names. Even people in the business would likely find it difficult to rattle off ten legendary traders. One of those legends, Paul Tudor Jones had this to say about trading: "My metric for everything I look at is the 200-day moving average of closing prices.

When the average person tries their hand at stock picking, they'll go on the internet and check the price-to-earnings ratio. Maybe they'll dig a little deeper and look at the some other statistics. They'll check the institutional ownership, look at the competition, look at its historical valuation, growth rates, debt levels, etc. If you've played this game before, you know how this usually turns out.

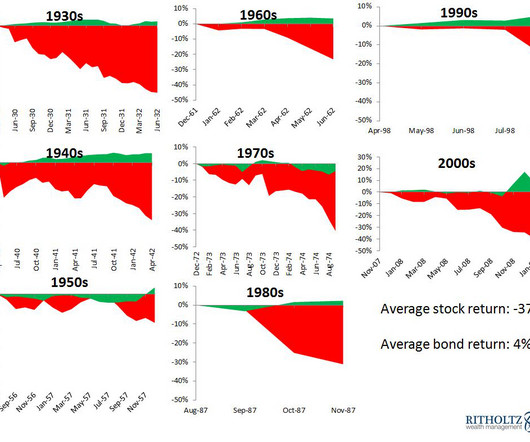

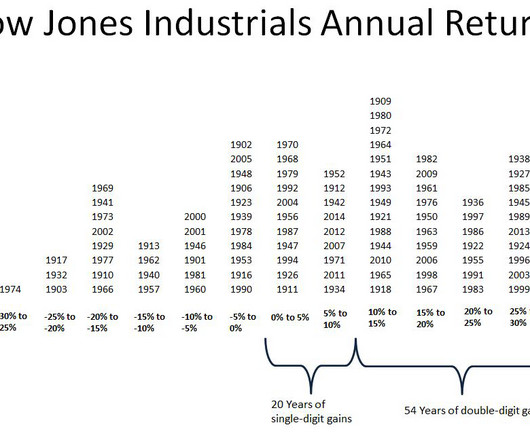

Good defense is more important than good offense not just on the football field, but on the investing field as well. Stocks experienced double-digit drawdowns in each of the last eleven decades, with the pain averaging -38%. Let's take a look at some of the gains and losses to get a better feel of how debilitating these declines can be. From November 1903 through January 1906, the Dow Jones Industrial Average gained 127%.

After a strong year for stocks, does it make sense for investors to dampen their expectations? That’s what many investors, professional or otherwise, were saying heading into 2014, following a year when stocks made new all-time highs and gained ~30 percent. Looking at the data shows that stocks have actually performed better than average following an exceptionally strong year.

As we step into 2024, the lending landscape evolves rapidly with technology, regulations, and market dynamics driving change. For banks and financial institutions to stay competitive and meet the evolving needs of their customers, these drivers must be understood and engaged with. Lenders can anticipate significant transformation fueled by technological advancements, regulatory shifts, and changing consumer behaviors.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content