This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Beyond insurance, advisors and their clients can also consider options such as the use of corporate entities such as Limited Liability Companies (LLCs) for business interests, and estate taxplanning tools such as Spousal Lifetime Access Trusts (SLATs) that can offer both estate planning and asset protection benefits for married couples.

50fires.com) Steve Chen talks financial education with Tim Ranzetta, founder of Next Generation Personal Finance. newretirement.com) Jess Bost and Mark Newfield talk with Dave Nadig about planning for big professional transitions. podcasts.apple.com) Taxes The 0% capital gains bracket is an opportunity.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

Financial planning and taxplanning go hand in hand. Including taxplanning as part of your service provides clients a comprehensive view of their finances and helps them achieve their financial goals. Start with Document Sharing The first step is to ask your clients to share their tax documents with you.

Going beyond FPA’s existing PlannerSearch tool, the narrowed-down list is meant to help consumers identify a focused subset of the most reputable planners.

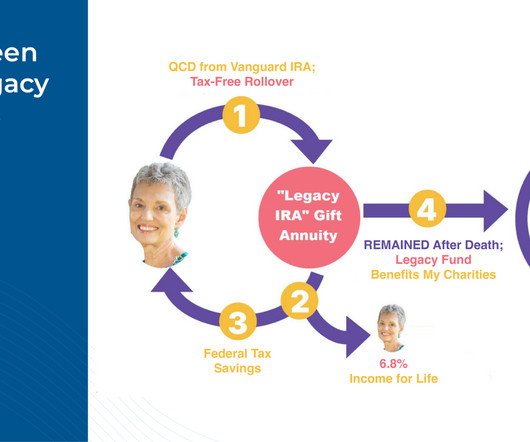

In this guest post, Kathleen Rehl, a semi-retired financial advisor and educator now focusing on her own estate planning considerations, shares her experience with creating her "Legacy IRA" rollover to a Charitable Gift Annuity to support her chosen nonprofits after Congress passed the SECURE 2.0 But the SECURE 2.0

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Knowledge and Personalized Planning Financial advisors can bring a wealth of knowledge from extensive education and experience, helping enable them to craft tailored strategies that align with your unique financial goals. 1 But working with a financial advisor has many additional benefits that can go beyond returns.

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

The hours spent managing administrative tasks , following up on missing paperwork, and ensuring compliance take away from time that could be spent on higher-value taxplanning services. From a business perspective, automation enables tax firms to grow without adding more staff.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning.

Your contributions accumulate tax deferred, which means that you don’t pay income taxes on the earnings each year. Then, if you withdraw funds to pay the beneficiary’s qualified education expenses, the earnings portion of your withdrawal is free from federal income tax. States may not follow the federal tax treatment.

These accounts can be used to pay qualifying educational expenses, including K-12 expenses and costs associated with college. Many states provide tax benefits for 529 contributions, and earnings from a 529 aren’t subject to federal tax when used to pay for eligible schooling-related costs. at the federal level.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The federal estate tax exemption has grown to $13,990,000 per person, giving you more flexibility in legacy planning. This creates more options for helping children with education, supporting aging parents, or passing on family wealth in tax-smart ways.

This is the time to do comprehensive financial planning: retirement planning, investment planning, taxplanning and estate planning. Help her find her independence through education, motivation and collaboration. Discuss more advanced estate planning, charitable planning and special family issues.

Here are some examples of one-time and ongoing services you can offer clients under the fee-for-service model: One-Time Services Ongoing Services Comprehensive Financial Plan Ongoing Financial Planning Second Opinion Engagement Advising on Held-Away Accounts Student Loan Analysis TaxPlanning Portfolio Tax Efficiency Review Estate Planning Housing (..)

Both sessions aim to educate about the value and benefits of financial and taxplanning, but no selling occurs. During the seminar with professionals, I ask attendees to exchange business cards and talk about what they do so they become more comfortable with each other. I don’t want attendees to feel pushed to buy.

The truth is, saving for your retirement and your child’s education at the same time can be a challenge. If the numbers say that you can’t afford to educate your child or retire with the lifestyle you expected, you’ll probably have to make some sacrifices. You want to retire comfortably when the time comes.

Bunching strategies Bunching strategies are taxplanning techniques used to maximize deductions by combining multiple years’ worth of deductible expenses into a single tax year. The Residential Clean Energy Credit offers up to 30% back on installation costs, helping reduce both your tax liability and energy expenses.

Consider early retirement taxplanning. Retirement accounts like 401(k)s and IRAs provide the advantage of tax-deferred growth, saving you significant amounts of money in taxes over the long term. This will allow you to plan for retirement and ensure you have enough funds to meet your needs.

Join Vida Jatulis , CFP®, and Anna Sergunina , CFP®, as they guide you through key strategies for funding your child’s education and developing a comprehensive timeline of actions to take. Key topics include saving strategies, estimating costs, taxplanning, and financial aid.

If you are having trouble with financial wellness, look for tools and education to help you develop a healthier relationship with your finances. The information provided is not intended to be a substitute for specific individualized taxplanning or legal advice. We suggest that you consult with a qualified tax or legal advisor.

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Since they may not have a lot of experience, it will be important to provide education and instill positive financial habits. You can build trust and credibility by educating them with content applicable to them and their situation such as podcasts, videos, seminars, and blogs, but be sure to make yourself available when they have questions.

Quick tips: If you feel like you are paying too much for a piece of tech, chances are, you are not using it to its full potential—research ways to become better educated on the tech and its solutions. Do you offer taxplanning as a service but manage client tax data in Microsoft Excel? You catch my drift.

Despite social media claims suggesting its illegal or akin to tax evasion, hiring your children offers distinct financial and educational benefits, assuming you adhere to labor laws and tax regulations. Hiring your children within a family business is a legitimate and potentially advantageous strategy when approached correctly.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

To attract new clients and foster long-term relationships, tax advisors could consider adopting digital marketing strategies. For example, “comprehensive taxplanning” or “long-term tax strategies for small businesses” can, over time, help you attract the right visitors.

Strategizing around how to pay yourself, your taxes, and other expenses. While there is a lot we could cover on the topic of business planning, for today we are going to focus on 3 important financial elements. TaxPlanning. Calculating tax rates can be tricky for small business owners. Expense Planning.

Theyre established to benefit charitable organizations, including educational or cultural institutions, community organizations, service organizations such as hospitals, and other nonprofits. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

TaxPlanning in Real Time Gone are the days when taxplanning was an annual event. With financial planning tools available in real-time, CFP s can assist clients with efficient taxplanning strategies throughout the year. It adds value to their services and sets them apart in a competitive market.

When selecting a tax professional, there are four main types to consider: Certified Public Accountant (CPA) Enrolled Agent (EA) Tax Attorney Non-credential Tax Professional Each type requires its own education and training, allowing them to provide specific services, which we’ll explore below.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

In today’s increasingly complex financial landscape, professional financial planningeducation has become more crucial than ever. The CFP certification stands as the gold standard in financial planning, offering professionals a comprehensive pathway to excellence in this dynamic field.

At its core, the CFP® Fast Track equips you with the expertise to offer sound financial advice, specializing in areas such as retirement planning, risk management, taxplanning, and wealth management. By pursuing this course, you become proficient in helping individuals and companies achieve their financial goals.

These two examples result in separate taxation rules based on their dates of sale and highlight the need to incorporate taxplanning in NUA decisions. We offer a full spectrum of financial planning and wealth management services that are tailored to your personal, business or retirement plan goals. Important Note.

Forget about stressing over missed opportunities and complex dates, by proper planning with a professional, you can have peace of mind knowing your money is working for you. A financial advisor can assist you in managing all the details that you must account for.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirement planning, wealth preservation and estate planning.

This certification is recognized globally and showcases a deep, systematic understanding of personal financial management, including investment planning, risk management, taxplanning, and retirement planning. What Is a Certified Financial Planner®? Compared to investment advisors, CFP® offer a more comprehensive service.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content