This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

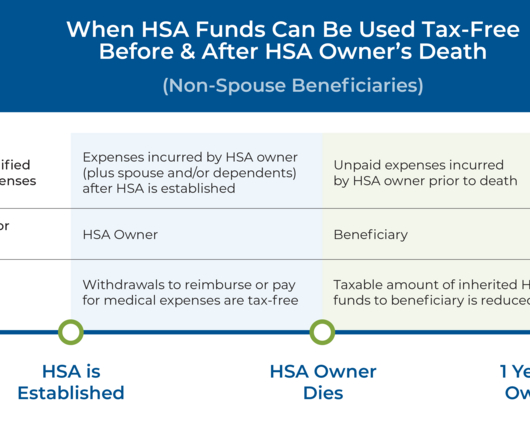

Health Savings Accounts (HSAs) feature useful tax advantages that make them a popular savings vehicle. One possible outcome of ‘superfunding’ an HSA, however, is that the account owner may not actually use up all of their HSA funds over their lifetime, which can have significant tax consequences. Read More.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

By Brady Marlow, CFP, AEP, CAP, CPWA, CExP , Director, Carson Private Client Wealth Strategy Although most people focus first on loved ones in developing their estateplan, you may also want your legacy to include continuing support of issues and organizations youre passionate about. million per individual for 2024.

Basic estateplanning is something that everyone should do, regardless of your age, marital status, the value of your assets, and if you’re a parent or not. This statistic illustrates that more Americans should consider estateplanning to help ensure their assets transfer quickly to their heirs. Gallop, May 2021.

An estateplan is a legal document that outlines a person’s wishes for the distribution of their assets and property after their death. It is essential to create an estateplan to ensure that your family and loved ones are taken care of in the event of your passing. Contact us today to get started!

is the projected future direction of medical care, where, instead of taking a reactive approach to disease and illness, healthcare practitioners instead invest more energy focusing on preventing illness and maintaining good health in the first place through more personalized plans for patients. Specifically, Financial Advice 3.0

Types of Powers of Attorney When appointing a POA, you have three basic options: medical power of attorney, financial power of attorney, and general power of attorney. A medical POA can help ensure that healthcare decisions are based on your choices and preferences, even if you cant communicate them yourself. File taxes on your behalf.

One of the most important aspects of developing a thorough estateplan is taxplanning, as this has the potential to diminish the impact of your gifts and your loved ones’ inheritances. Let’s take a look at the tax impact and other considerations of each. million before triggering federal estatetaxes).

And if they’re unprepared—or worse, if the family estateplanning strategies are less than buttoned up—how will that affect your practice down the line? To start the conversation with clients preparing to transfer wealth, you can simply say: “Tell me about who in the family was involved in the development of your estateplan.”

Investment planning also plays a crucial role in tax optimization, enabling you to minimize tax liabilities and maximize after-tax returns. Additionally, tax-loss harvesting, and other tax-optimization strategies can further improve the tax efficiency of your investment portfolio, thereby enhancing overall returns.

Estateplanning is a critical component of a comprehensive financial plan. Furthermore, estateplanning includes aspects such as tax minimization strategies, asset protection, and charitable giving. There are many different types of trusts, each designed to address specific estateplanning needs.

ESTATES Family EstatePlanning: The 6 Essentials Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. According to one survey, 67% of Americans have no estateplan, which may reflect an aversion to thinking about dying or getting gravely ill. Navigate Family EstatePlanning with Park Place Financial .

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount.

While a financial plan focuses on managing your finances during your lifetime, an estateplan is essential for determining the fate of your assets after you pass away. Estateplanning involves the transfer of your assets to your heirs in the event of your passing.

Like the other POAs, the Healthcare POA specifically addresses the decisions the attorney-in-fact can make for the principal—usually the decisions are related to medical treatment, medication, discharge, blood transfusions, etc. Use an estate-planning attorney to draft a POA. Who needs it? How much should it cost?

In addition to making funeral arrangements and notifying family and friends, another priority is alerting your estateplanning attorney and financial advisor. Asset Titling, Beneficiary Elections, and Probate The estateplanning attorney is going to be critical here. But not everything needs to get done today.

However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. Estateplanning is one of the key components of financial planning these individuals need to focus on. Business succession: Many high-net-worth individuals are business owners.

And I think you will also, if you are at all curious about estateplanning or investing or personal finance, this is not the usual discussion and I think it’s very worthwhile for you to hear this and share it with friends and family. And I, I found it to be an absolutely fascinating conversation. Right, right.

By staying healthy, retirees can reduce medical expenses, enjoy a higher quality of life, and preserve their wealth for future generations in doing so. 4] Leaving a Legacy for Future Generations To ensure the preservation of generational wealth, retirees must plan for the distribution of their assets after their passing.

Medical emergency. Data from the Kaiser Family Foundation (KFF) highlights that around 41% of American adults have debt from medical or dental bills. When a medical emergency strikes, however, the cost is probably the last thing on your mind. I recently experienced a medical emergency (and the resulting financial emergency).

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

But with the right planning, you can confidently figure out how much to save for a baby and still stay on track with your financial goals! Create or revise your estateplan 9. Plan for emergency expenses 11. If you already have an estateplan, make sure to update it to include your new baby.

Contributions to your 401(k) are pre-tax, meaning that for every dollar you contribute, you actively lower your taxable income. If you’re covered by a workplace retirement plan, you likely won’t be eligible to make deductible (pre-tax) contributions to your traditional IRA, but investing in it still provides valuable benefits in retirement.

You should also get a good health insurance policy for you and your family to protect you against the financial hardship of medical bills. Have a will and estateplan. While it’s not a fun topic, having a will and estateplan can help your family navigate during a difficult time once you’re gone.

Skilled Nursing: Medical facilities that offer a higher level of care, particularly for individuals with complex health needs, providing specialized medical services and round-the-clock support. It’s Never too Late to Start Planning There is a saying, “If you don’t make a plan, a plan will be made for you”.

10 steps to manage a financial windfall Expert tip: Keep living your life normally Factoring in taxes How do you deal with sudden financial windfall? Tax refunds that are more than you expected. Update or create your estateplan If you don’t already have an estateplan , now would be a great time to create one.

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estateplanning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

As a couple aged 65 in 2023, you may need approximately $315,000 saved (after tax) to cover your healthcare expenses. This underscores the necessity of integrating healthcare costs into your broader retirement planning strategy. It is easy to focus on accumulating a nest egg for a comfortable future.

However, this thought can be unrealistic if you are still paying on a mortgage, or if any unexpected medical expenses arise. One major financial factor to consider is that longer lifespans tend to increase medical-related expenses during retirement years. Calculating After-Tax Rate of Investment Returns.

Prepare Your EstatePlanning Documents. People have a laundry list of reasons to avoid estateplanning. Let’s look at some key estateplanning documents: Will. A will outlines your wishes for your estate. Medical Directive. A 401(k) is a tax-efficient way to save for retirement.

Be sure to make a plan to pay off credit cards, loans , and medical bills as quickly as you can so you can start creating more wealth for future generations. How to pass on generational wealth Now you know how to build wealth and the generational wealth meaning, but you’ll also need to create a plan to pass it along.

Contributions to your 401(k) are pre-tax, meaning that for every dollar you contribute, you actively lower your taxable income. If you’re covered by a workplace retirement plan, you likely won’t be eligible to make deductible (pre-tax) contributions to your traditional IRA, but investing in it still provides valuable benefits in retirement.

If you wish to have a firm grip on your finances and want to learn about different strategies related to investing, tax-saving, or retirement planning, consult with a professional financial advisor who can advise you on the same. You need to review your financial plan at regular intervals. When you’re planning your legacy.

In addition to this, you can save more and plan for more significant purchases with greater ease. The tax liabilities for married couples filing their taxes jointly will differ from single individuals and those filing individually. Married couples can file their taxes jointly under the filing status of married filing jointly.

Understand your condition, prepare for all the questions that the doctor would ask, ensure all your test reports and medical history documents are in order and so on. Consider the needs of your family A sound financial plan always has room for the needs of the family members. your tax records and so on. Need a financial advisor?

However, as your children grow older, it can work to your advantage—and that of your entire family— to share with them key financial, medical, and estateplanning information. This document specifies an individual’s preferences regarding the administering or withholding of life-sustaining medical treatment. Living Will.

As we approach the end of the year, you may want to review areas that may impact your wealth and estateplanning next year. Completed an inventory of assets- Periodically update inventory assets listed in your trust documents, such as real estate, collectibles, vehicles, etc.,

Look for: car repairs and maintenance, medical expenses, home maintenance, membership renewal, seasonal utility increases, vehicle registration renewal, back to school supplies and field trips, tax preparation fees. Housing This category covers your mortgage or rent payments, property taxes, insurance, and home maintenance expenses.

Do beneficiaries pay taxes on 401k inheritance? Making funeral and burial arrangements After taking care of the immediate needs after the death of a loved one, you can start planning the burial or funeral arrangements and going through the checklist when someone dies. What happens to a person’s credit cards when they die?

Conversely, if you are generally healthy and don’t anticipate significant medical needs, a high-deductible health plan could be more cost-effective. If your employer offers you the option to purchase additional coverage, remember that paying the premium yourself means your disability income will be tax-free.

Tax efficient selling strategies. Gifting and tax-efficient trusts. a high demand medical device business) trades at a high multiple. Be tax efficient when you sell: Identify the most tax efficient order for selling options/shares. Things you can do including: Prepare for the worst. Exercising options.

Financial advisors for medical professionals can offer a tailored approach to managing unique financial landscapes. However, physicians are often consumed by the demands of a rigorous medical career, and as a result, they can easily overlook this essential step. It also puts physicians in the upper slabs of federal tax brackets.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content