This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

Podcasts Christine Benz and Amy Arnott talk the state of retirement with Anne Tergensen of the WSJ. podcasts.apple.com) Taxes A year-end taxplanning checklist. kindnessfp.com) How to think about taxes in early retirement. humbledollar.com) How to retire without regrets. Quit playing.

riabiz.com) A round-up of recent financial advisortech news including Holistiplan's estateplanning module. kitces.com) What it means to be a great adviser to retired clients. thinkadvisor.com) A year-end taxplanning checklist. (standarddeviationspod.com) The biz Fidelity is crushing it.

(ritholtz.com) Rick Ferri talks with Christine Benz about her new book "How to Retire, 20 Lessons for a Happy, Successful, and Wealthy Retirement." morningstar.com) Sam Dogen talks in ins and outs of early retirement with Khe Hy. sites.libsyn.com) Retirement Why spending decisions in retirement are challenging.

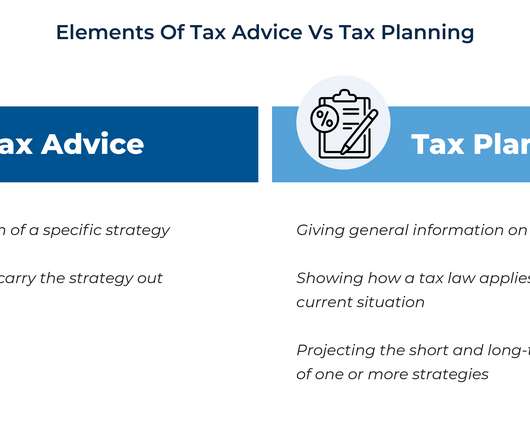

Taxes are a central component of financial planning. Almost every financial planning issue – whether it is retirement, investments, cash flow, insurance, or estateplanning – has tax considerations, and advisors provide a great deal of value in helping clients minimize their overall tax burden.

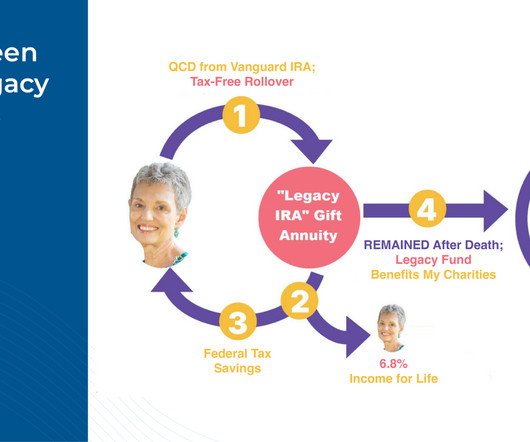

In this guest post, Kathleen Rehl, a semi-retired financial advisor and educator now focusing on her own estateplanning considerations, shares her experience with creating her "Legacy IRA" rollover to a Charitable Gift Annuity to support her chosen nonprofits after Congress passed the SECURE 2.0 But the SECURE 2.0 Read More.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirementplanning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent survey indicates that clients of financial advisors are more confident than others about their financial preparedness for retirement and are more likely to have a financial plan in place that can weather the ups (..)

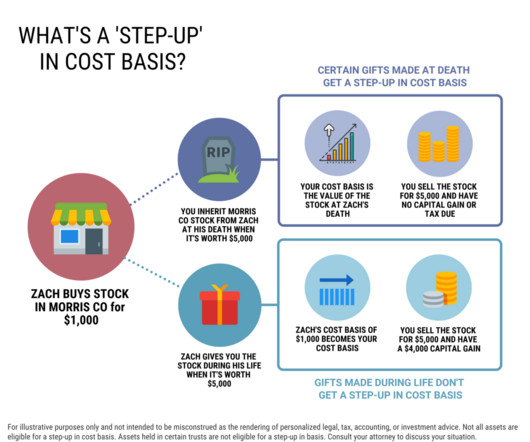

Example of a step-up in tax basis on stocks inherited at death What types of assets are eligible for a step-up? Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis. Can stocks get stepped up twice?

Podcasts Michael Kitces talks divorce planning with Michelle Klisanich who is a Wealth Advisor for Financially Wise Divorce. kitces.com) Matt Zeigler talks with Wade Pfau about managing sequence of returns risk in retirement. kitces.com) Taxes Following the RMD rules for inherited IRAs may not be optimal. forbes.com)

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estateplan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

For instance, qualified plan assets (e.g., 401(k) and 403(b) plans) offer purportedly unlimited creditor protection for plan participants, meaning that if an individual were to be sued or file for Federal bankruptcy protection, balances in these accounts would not be at risk. tenancy by the entireties and community property).

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

Financial advisors play a crucial role in assisting you before your retire. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Here are 5 benefits of hiring a financial advisor after you retire: 1.

Retirementplanning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estateplanning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Optimize retirementplan contributions The maximum allowable 401(k) contribution for 2023 is $22,500, with a $7,500 additional contribution, if the plan allows, for taxpayers who are 50 and over.

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estateplanning trends that tax advisors should be tracking during the second half of 2024. contained a number of changes relevant to estateplanning. citizens and residents. The SECURE Act 2.0

This is the time to do comprehensive financial planning: retirementplanning, investment planning, taxplanning and estateplanning. Discuss more advanced estateplanning, charitable planning and special family issues.

While there are certainly ways to do estateplanning without a lawyer, for most people hiring an estateplanning attorney makes the most sense. Estateplans can get complex fast, and even fairly straightforward estates can feel overwhelming if you’re not trained in the area. Do your research.

A financial or tax adviser can help you identify ways to capture that loss so you can offset gains from your liquidity event. Max out your retirement contributions. Related article: Tax Benefits of a Donor-Advised Fund. Estateplanning. at the federal level. Get started here.

Have you thought about taxes or estateplanning or when to withdraw and from where? From retirement income to tax strategies on an investment property, Brian shares what options you might have. Here’s what you’ll learn on today’s show: Why shouldn’t you planretirement by yourself? (0:12)

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

Common types of assets that will pass via beneficiary designation include retirement accounts, life insurance, and some pensions and annuities. This article is a high-level overview of the various estateplanning techniques and considerations when using revocable living trusts from the perspective of a wealth advisor (e.g.

Navigating the complexities of estateplanning can often feel like charting through uncharted waters, especially when it comes to handling assets, taxes, and ensuring one’s legacy is preserved according to their wishes. does not provide investment, tax, legal, or retirement advice or recommendations.

Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts. TaxPlanning: Optimize tax efficiency through strategies such as retirement contributions, tax-deferred accounts, and deductions and credits. Let’s break each one down. Outliving their money.

Choosing whether to fund a trust with your assets is an important decision in the estateplanning process. A will and a trust are two different estateplanning tools. A retirement account won’t go through probate unless you didn’t name any (living) beneficiaries.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. Distributions only qualify for NUA treatment if completed after the triggering event (separation from service, reaching retirement, death or disability). Cost Tradeoff.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

We’re coming up on the end of the year, and while it’s a time to take a break and enjoy the holiday season, it’s also a good time to consider tax strategies that may benefit you. Gift Tax Exemptions Each year, you can give up to $17,000 to any number of people tax-free.

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

The following areas are among the most vital to discuss with high-net-worth clients: EstatePlanning. To ensure your wealth benefits loved ones, you should prepare your estate and determine how to distribute your assets. Estateplanning for high-net-worth individuals is also significant because recent developments in U.S.

Starting Out clients are likely to be digitally-fluent, so putting this type of responsibility on them isn’t overly burdensome and can create major efficiencies in your planning processes. Holistic planning will be a valuable way for you to address this broad range of needs.

Whether planning for retirement, saving for your children’s education or simply looking to grow your investments, finding the right wealth management services in Kansas City can make all the difference. Long-term goals typically encompass retirementplanning, wealth preservation and estateplanning.

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools. Tax breaks come and go, and are beyond our control. Remember, your goal is to minimize lifetime taxes paid.

Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. These include tax-sheltered accounts for saving toward retirement, healthcare, and education, as well as tax-efficient tools for charitable giving, emergency spending, and estateplanning. .

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content