This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

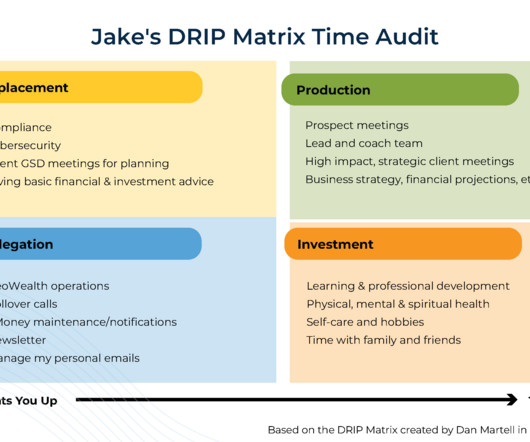

In Jake's case, after deciding that he was overservicing clients during the earlier years of his practice, he started scheduling fewer standard meetings and limited the number of after-meeting action items, freeing up his time and mental bandwidth for other activities to grow and run his firm.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that NAPFA has announced that it will no longer exclude advisors who receive up to $2,500 in annual trailing commissions from previous product sales, if they agree to donate that money to a non-profit organization (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the SEC this week fined 4 RIAs for violations of its marketing rule related to their claims that they offered 'conflict-free' financial advice.

While it remains to be seen whether the measures will actually be enacted, proposed measures include raising income and capital gains tax rates, instituting wealth taxes, and reducing the state estate tax exemption, potentially creating future planning opportunities for advisors with clients in those states. Read More.

Which suggests that while advisors might be hesitant to publish their fees on their website before being able to meet face-to-face with prospects, doing so (and linking the fees to the value proposition they offer their ideal clients) could help certain consumers overcome their reluctance and start the process to becoming clients!

Also in industry news this week: A recent study finds that having a defined marketing strategy is a linchpin of marketing success, as advisors with a defined strategy were more likely to have seen an increase in inbound leads during the past 12 months and have more confidence in meeting their practice goals during the coming year than those without (..)

Also in industry news this week: The SEC has penalized 2 firms for false and misleading claims related to their use of Artificial Intelligence (AI), signaling the regulator's interest in advisers' "AI-washing" practices A research report suggests that fee-only RIAs with strong organic growth and enhanced service offerings for their clients are likely (..)

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management.

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management.

In this episode, we talk in-depth about why Mindy attributes the success of her practice’s structure to the realization that she does not enjoy selling products or investment management (or dealing with compliance that goes with them) and could more efficiently scale with an advice-only approach to one-year financial planning engagements that (..)

In this episode, we talk in-depth about how Jessica leveraged her investment banking experience in wealth management mergers and acquisitions to build her own business where she could provide more independent M&A advice, why and how Jessica developed her flat-fee advice model for mergers and acquisitions to, similar to the evolution of fee-only (..)

Sarah-Catherine is the founder of Aptus Financial, a fee-only financial planning firm based in Little Rock, Arkansas, that is approaching $2M in revenue and works with over 480 client households. Welcome to the 356th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Sarah-Catherine Gutierrez.

The good news is that number has come down over the past couple of years, falling to its lowest number since 2017. About Your Richest Life At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning.

About Your Richest Life At Your Richest Life, Katie Brewer, CFP, believes you too should have access to financial resources and fee-only financial planning. Protect Your Identity Tax season is a particularly vulnerable time for tax and identity theft. Should You File an Extension?

Your Richest Life by the Numbers. As a fee-only financial planner, I am committed to helping my clients achieve overall financial well-being. At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. Expanding the Your Richest Life team.

billion in feeonly asset flows for the full year 2013; 37% of Morgan Stanley wealth management’s total client assets are now in fee based accounts a record high. I’ve lost count of the number of times that 30 seconds into an interview, I’ve gotten a side-eyed glance from him that says “ Loser. It’s uncanny.

These numbers show that retirement is becoming a more fluid concept, with many people opting for a “second act” career, side gig or part time work. Money tips for your 40s About Your Richest Life At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning.

Seeing their situation spelled out in numbers can feel scary, so they end up avoiding it altogether. The truth is, no matter how disappointing the numbers might be, they’re still much better than a vague guess. The actual numbers might not be as bad as you thought, or you’ll have a much clearer idea about what you have to do next.

The crisis in Ukraine has also played a key factor in these rising energy costs, particularly in fuel, an impact that can be seen in the CPI number. We’ll receive July’s inflation numbers on Aug. He is a fee-only, fiduciary financial advisor who works with clients locally in Madison and around the country.

That number will decrease to 26 percent for 2033, 22 percent for 2034, and it will expire in 2035 unless Congress renews it. As far as roofing goes, only solar roofing tiles or solar roofing shingles apply. This credit was recently extended through 2034. For 2022-2032, Congress set the credit at 30 percent the cost of installation.

It's not just about recording numbers; there are rules, regulations, and standards to follow. While taking on this task yourself can be tempting, the consequence of any mistakes could be costly. First, let's address the complexity of bookkeeping. Missing even a minor detail could lead to significant issues down the line.

Your Richest Life by the Numbers Here are some of the highlights of my eight years in business: -Worked with over 170 families to date -Working with over 45 families on an ongoing basis -Writing more than 200 blog posts for my own website -Listed as a D Magazine Best Financial Planner for the eighth year in a row As a fee-only financial planner, (..)

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in.

The best way to solve this problem is by increasing the number of fee-only SEBI Registered Investment Advisors (RIAs) who by design think in the interest of clients. This results in not just declining purchasing power with time but also reduces their chances of meeting important life goals.

But again, that number can vary based on when you started saving for retirement, and how much you’re able to save. You can also get to that number by asking yourself some fundamental questions: What age do you plan to retire? The answers to these questions will get you closer to your number, but there’s still more to consider.

Core CPI is an attempt to strip out the most variable drivers of inflation (namely food and energy) from the base (or “headline”) CPI number, but the costs of food and energy can infiltrate into core CPI items such as apparel and household goods. Let’s all hope that the inflation we are experiencing won’t be so sticky after all. .

If you’re selling a business and can’t close before the end of the year, consider the pros and cons of an installment sale, to spread out the taxable capital gain over a number of years (potentially staying under the surtax limit). About Darrow Wealth Management.

Some people start to feel like they’re behind on their goals anyway, so what’s the point of looking at the numbers to face the reality? The truth is, only good things can come from looking at all your accounts, your spending, your savings, etc., Checking in with your financial goals: Where are you now?

The number varies, but $1,000-$2,000 in cash is about the ballpark for covering travel costs, gas, food, etc. At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. That’s why some cash on hand can be crucial during a disaster.

Below are the different types of financial advisors you can choose from based on their fee model: 1. Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products.

How a company sets up its stock plans and each employee’s situation can vastly impact these numbers and introduce other considerations that might make an 83(b) more or less appealing. As financial professionals, it’s our job to help guide you through the options and determine the best course of action for you and your unique situation.

There are generally restrictions on the number of transactions you can have in this type of account. While it’s technically a checking account, you are generally restricted by the number of transactions you can have without fees and it doesn’t function like a normal checking account. Current Yield: 0.12% – 3.1%

The sheer volume of documents (with weird combinations of letters and numbers) is enough to make anyone stress! Today we want to put some of those anxieties to rest, for both you as an individual taxpayer, and for your clients. We can help you and your clients understand what to keep (and perhaps more importantly, why), and for how long.

The advisors can be differentiated based on the fee structure they use to charge fees such as fee-only, commission-only, hourly-fee, monthly fee, etc. Also, pick a fee-only advisor over a commission-based one as the former is legally bound to place your best interests before their own.

In 2022, I founded New Lantern Advisors, an independent, fiduciary, fee-only, longevity-focused financial planning and investment management firm, so that I could more directly serve a select group of clients, as well as help fellow advisors, serve their own clients.

As you are researching your wealth management options, you will see a number of names for those who can help you invest, including brokers and advisors. Fiduciary advisors are generally fee-only. Let’s break it down. Brokers are paid by a commission on the investment products they sell.

Buyers are competing for a smaller number of homes, so the less time you waste looking at properties that won’t work for you, the better. At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. This is also going to help you put in an offer faster.

.” Only 4 percent of Certified Financial Planner™ professionals identify as Asian American or Pacific Islander (AAPI), though they make up 6.2 1,2 Despite the small numbers, AAPI professionals remain the largest ethnic minority within the financial planning profession. percent of the American population.

With these come a number of different dates to keep track of, which as a small business owner or a solopreneur can get overwhelming, fast. 8 MIN READ There are a million things to keep track of when running a business. There are customers and employees, marketing and keeping an eye on industry trends, cash flow and compliance. to address!

While not everyone avoids taxes, there are a significant number of people who do. Clients are often slow to respond, don’t provide the requested documents, completely ghost… well, you get the idea.

Soft Skills – The role of a financial advisor goes beyond reading numbers, interpreting them, and offering advice to clients. There are two types of Financial Advisors in India – Fee-Only Advisors and Commission Only Advisors. The fact is irrespective of degree and qualification there is no substitute for experience.

Listings increased by 12 percent in February, and that number is expected to grow throughout the spring and summer months. About Your Richest Life At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. The post Buying a House in 2024?

It’s so much more than just numbers, and it can be bogged down with shame, fear and frustration. At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. Commit to Talking About Your Money. Money is hard for so many of us to talk about.

There are a number of changes in place for borrowers on an income-driven repayment (IDR) plan, or who have Public Service Loan Forgiveness (PSLF.). At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. About Your Richest Life.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content