This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The challenge in writing How NOT to Invest was organizing a large number of ideas, many of which were only loosely connected, into something coherent, understandable, and, most importantly, readable. That insight greatly simplified my task of making the book both fun to read and helpful for anyone interested in investing.

For instance, the financialadvice industry has seen many changes to regulations (for both advisors and their clients), advisor business models, and the advisor technology landscape. The changing patterns in how financialadvice is delivered can be compared to the similar trends seen in the evolution of medicine.

Answering it well requires a range of assumptions – from estimating average investment returns to understanding correlations across asset classes. Yet, even with the most accurate CMAs, financialadvice rarely aligns flawlessly with reality. "How much can I spend in retirement?"

They consider your current financial situation, risk tolerance, and future objectives to help develop a comprehensive plan. This personalized approach can help you make financial decisions that are well-informed and strategically sound. Contact us today to learn more about our unique approach to financialadvice.

There are many financial advisors who take issue with the financialadvice offered by popular personal finance personalities such as Dave Ramsey. Though many potentially valid criticisms of this process tend to concern technical details (e.g.,

Podcasts Barry Ritholtz talks with Meb Faber of Cambria Investments about deferring capital gains with ETFs. slate.com) Personal finance Financialplanning is all about tradeoffs. barrons.com) Financial stress is real. ritholtz.com) Jack Forehand and Matt Zeigler talk lessons learned from Ben Carlson.

Podcasts Michael Kitces talks financial wellness with Zack Hubbard. Zack is the Director of FinancialPlanning and Participant Engagement of Greenspring Advisors. youtube.com) Brendan Frazier talks with Michael Kitces about mastering the human side of financialadvice.

Which is surprising to some, given that a decade ago, the emergence of so-called "robo-advisors" was supposed to displace human financial advisors and compress advisory fees. In reality, though, the robos struggled to gain traction, and the human financialadvice business just continues to grow.

Unlike their predecessors, they are tech-savvy, investment-curious, and financially independent-inded. But they also have a mild addiction to online shopping, an over-reliance on BNPL schemes, and a tendency to take financialadvice from influencers who may or may not know what theyre talking about.

Podcasts Daniel Crosby talks with Michael Kitces about automation and the future of financialadvice. standarddeviationspod.com) Michael Kitces talks with Jason Wenk, CEO of Altruist, about how he is trying to build an all-in-one investment OS. smokestack.beehiiv.com) The first rule of financialadvice is 'do no harm.'

Consumers have a wide range of options when it comes to choosing a provider of financialadvice, from larger wirehouses and asset managers to smaller Registered Investment Advisers (RIAs).

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the shift in financialadvice from pure investment management to comprehensive financialplanning continues, with more individuals becoming CFP professionals than CFAs in the past few years as consumers increasing the diversity (..)

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-only financialplanning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet FinancialPlanning.

Traditionally, financialadvice and tax preparation have existed as 2 related, but separate, services. Besides the fact that many financial advisors don’t hold the necessary credentials (e.g., Read More.

For these situations where rules of thumb and back-of-the-napkin advice won't suffice, more comprehensive and detailed projections are still preferred, and traditional financialplanning software is often the advisor's most effective tool. So, which planning software should you use? Let's take a look!

What's unique about Andrew, though, is how he, as a financial advisor with autism, has built a firm with a specialized niche of autistic and other neurodivergent clients, helping them navigate their unique and complex financialplanning challenges.

Which would invariably result (after a considerable investment of both the firm owner's time and money) in a less-than-optimal experience for the new advisor and would likely do little to improve the industry's already dismal retention rate.

Notably, while the rule will create an additional compliance burden, the due diligence advisers offering comprehensive planning services (as well as their investment custodians) are likely already conducting on their clients to create an effective financialplan could be a 'defense mechanism' for these firms against criminals looking to take advantage (..)

There are many financialplanning considerations before, during, and after a divorce. A key part of the process from a financial standpoint is dividing the assets. Here are some key considerations when financialplanning for a divorce. What investments best suit your risk profile and goals?

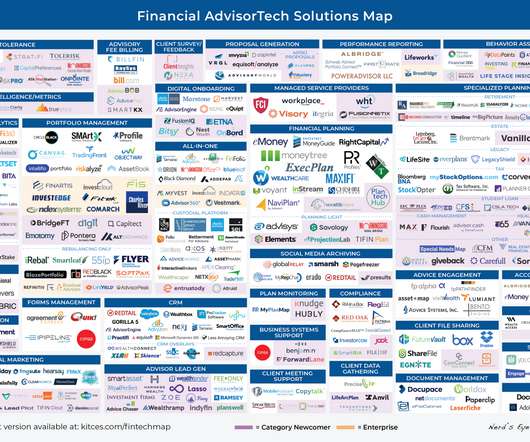

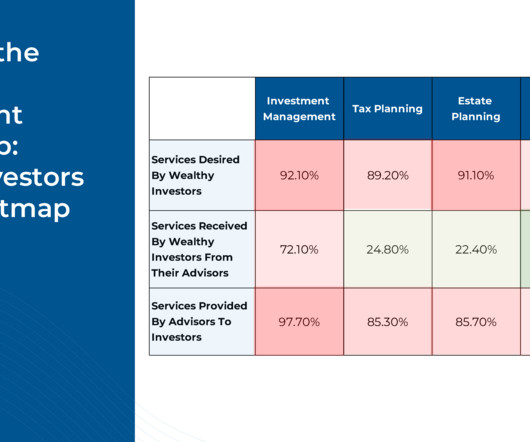

And be certain to read to the end, where we have provided an update to our popular “Financial AdvisorTech Solutions Map” (and also added the changes to our AdvisorTech Directory) as well!

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client.

Advisory agreements for Registered Investment Advisers (RIAs) contain many sections that are important both for the purposes of complying with SEC and state securities regulations, and for constituting a valid agreement between the RIA and the client.

Investing A bear market provides different opportunities for different generations. awealthofcommonsense.com) Why now is a great time to get started investing. theguardian.com) Personal finance Helpful personal financialadvice should not make you feel bad about yourself.

In contrast, a fee-only, flat-fee financial planner provides transparent pricing, unbiased advice, and comprehensive financial planningwithout taking a percentage of your investments. Unlike AUM-based advisors, they do not earn commissions or take a percentage of your investments.

If clients and advisors approach issues with a fundamentally different psychology, then an advisor's 'comprehensive' advice may not address the client's actual problems. Fortunately, financialadvicers can bridge these communication gaps in a few ways, starting with their discovery process.

Key Highlights Millennials can benefit a lot from getting financialadvice. You should change your marketing approach to meet the specific financial needs and interests of millennials. Listen to their concerns and adjust your financialadvice to align with their goals. Right now, few of them use advisors regularly.

Financialplanning is a vital aspect of life. Often, the financial lessons and advice passed down from generation to generation shape an individual’s approach to finances. In this blog, we’ll dive deep into some lessons they’ve learned and the role that financialplanning plays in supporting their goals.

Of an estimated 104 million households seeking some level of financialadvice, 88 million of those households want that advice from a financial professional. In this overview, we will explore the demographics of each stage, the financialplanning needs of people in each stage, and strategies for serving them.

Early in my career at a large broker-dealer in San Francisco, I noticed retirees were the ones getting all the attention, while the Millennials were craving financial knowledge and the attention of financial advisors. Tax and insurance advice was also somewhat constrained. Many advisors find that challenging.

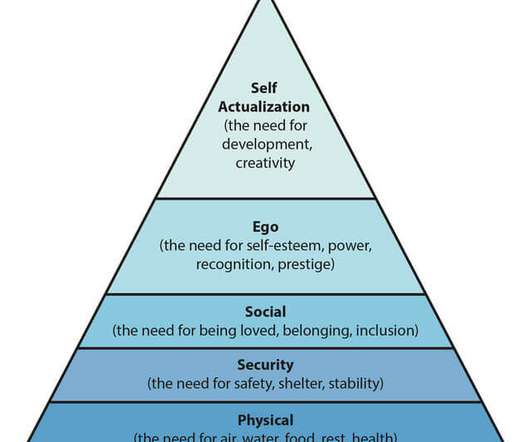

As client expectations continue to evolve, there is an opportunity for financial planners to broaden and deepen their service offerings by providing holistic financialplanning. One way to assess this is to look at the value of financialadvice as it stacks up to basic human needs. The Hierarchy of Financial Needs.

Podcasts Christine Benz and Jeff Ptak talk the evolution of financialadvice with Preston Cherry founder and President of Concurrent FinancialPlanning. morningstar.com) Douglas Blake, Managing Director of Investment Services at Kingswood U.S., talks with Joshua Brown about the future of the advisor conference.

About a decade or so ago, one of the most pressing issues facing the financialadvice industry was the threat of an imminent deluge of advisor retirements coupled with a paucity of succession plans to transition clients to the next generation.

Podcasts Peter Lazaroff talks with Michael Kitces about the evolution of financialadvice. peterlazaroff.com) Daniel Crosby talks with Brendan Frazier about his list of the 10 guiding principles of financial psychology. thinkadvisor.com) Fidelity Institutional’s alternative investments platform continues to garner assets.

Investing in an Individual Retirement Account (IRA) is an excellent way to save for retirement. However, selecting the right investments for your IRA can be challenging. In this article, we will explore some strategies to help you choose the best investments for your IRA.

youtube.com) Daniel Crosby talks with Amy Mullen about five steps for values-based financialplanning. etftrends.com) Robo-advice Why the SEC is scrutinizing robo advice. riabiz.com) Canadian private equity firm Altas Partners has agreed to invest in Mercer Global Advisors. kitces.com) M&A McKinsey & Co.

While financialplanning has become more popular, it’s still not center stage for most advisors. I’ve got Zack Hubbard , the director of financialplanning and participant engagement at Greenspring Advisors, a fee only RIA. I am an irreverent and fun marketing consultant for financial advisors. Repeatable?

Mark Berg of Timothy Financial has a great story about how he scaled his hourly financialplanning firm, grow it to a multiple-advisor company. I am a CFA charterholder and financial advisor marketing consultant. Not all hourly financialplanning firms are one person shops! Check it out!

This might have been their own doing or the result of poor financialadvice. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. FinancialPlanning is vital. Maybe they’re right.

Achieving the status of Certified Financial Planner® (CFP®) represents a significant professional milestone in financial services. Recognized in over 27 countries globally, the CFP® designation is one of the most respected and widely acknowledged credentials in financialplanning.

Women and investing is a topic that doesn’t get mentioned often enough, but it is extremely important. Women’s financialplans are unique, so their investing strategies should be, too. Find out more about women and investing, and discover ideas for creating your own investmentplan.

By Craig Lemoine, Director of Consumer Investment Research . We speak a secret language in financialplanning. So much of our world is filled with abbreviations surrounding insurance and investment products, processes, education and accomplishments. . Registration exams are required to talk to a customer or client.

Recognizing the need for a financialplan is a significant first step toward the goal of achieving personal financial security. Table of Contents What is a FinancialPlan? Table of Contents What is a FinancialPlan? Why is FinancialPlanning so Important?

As the move to transparency in financialplanning takes hold, regulations are changing in Colorado and other states. Here’s the triumph of virtue that financialplanning transparency will (FINALLY) bring to planners across the country and the benefits to clients that come along with it. What should financial advisors do?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content