This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Although there are some basic guidelines, your financial life is as unique as your fingerprint. Looking for personalized retirementplanning advice?

30 years ago, when financialplans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

30 years ago, when financialplans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

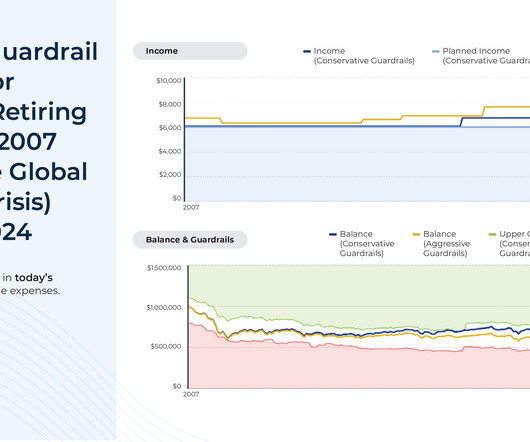

Monte Carlo simulations have become a central method of conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs. the Great Depression or the Global Financial Crisis), showing clients when and to what degree spending cuts would have been necessary.

Assuming that you have a financialplan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing.

There are some things in life you just can’t plan for: an unexpected illness, job loss, death of spouse, disability. And while experiencing one of these major events can drastically impact your life, having an effective financialplan can help ensure that it doesn’t ruin your financial well-being.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. A well-structured approach ensures that every aspect is carefully considered. It also minimizes errors and oversights.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. Consider working with a fiduciary financial advisor to help manage your investments and provide financialplanning guidance before and during retirement.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

No one cares about your financial well-being more than you, so it's important to have a financialplan for yourself. Knowing how to make a financialplan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement.

FinancialPlanning is vital. If you don’t have a financialplan in place, or if the last one you’ve done is old and outdated, this is a great time to review your situation and to get an up-to-date plan in place. Do it yourself if you’re comfortable or hire a fee-only financial advisor to help you.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financialplan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Take stock of where you are. Photo credit: Flickr.

No one cares more about your financial well-being than you, so having a personal financialplan is important. Knowing how to make a financialplan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. What is a full financialplan?

For one person, that might mean reassessing their risktolerance and portfolio holdings to make sure that they hold assets that will at least sustain their value or provide a safer return, such as an interest rate or a dividend yield. Why Meet with a Financial Advisor? What Can We Expect from the Markets?

Depending on your income goals and risktolerance, this bucket can provide you with dividend or interest income that can supplement other forms of retirement income. During working years, this bucket is less of a concern, but come retirement, planning your income sources to fund this bucket is crucial.

You may consult with a professional financial advisor to better understand your financial history and the ensuing impact your past choices may have on your future financialplanning. By reflecting on past experiences, individuals can glean insights that help in shaping clear and actionable financial objectives.

First, do you have the necessary financial acumen and knowledge to make financial decisions? Are you good with numbers, accounting, and financialplanning? If yes, then DIY financialplanning might be a good option for you. What is DIY financialplanning? Chalk out a financialplan.

That said, entrepreneurship can sometimes be cumbersome in spirit, especially in terms of financialplanning. Long working hours, lack of financial security, irregular income, managing investors, liquidity issues, insufficient equity, and more, while juggling personal finances, can be a daunting task.

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. Your goals may be different depending on your age, retirement timeline, and lifestyle.

Generally, investors don’t increase their risk profile as they move through retirement. Allocation choices also shouldn’t be based on the notion that dipping into principal derails a financialplan. As of 1/31/2025, the 10-year annualized total return for the S&P 500 (SPY) was 13.6% versus 1.1%

Track income, expenses and build in budgeted items for future financial goals. Meeting with a qualified financialplanning professional can help you begin building positive and lasting behaviors.?? . Take Advantage of RetirementPlans and Matching Contributions. Consider the following example below:?? .

A Guide for FinancialPlanning When it comes to managing your finances, it’s crucial to work with a professional who puts your interests first. As a result, this plan can help guide your financial decisions and ensure that you’re on track to achieve your goals. appeared first on Yardley Wealth Management, LLC.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-Term vs. Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals.

When we are busy working to earn a living and spending time with our family, first thing needs to think about is RetirementPlanning. Generally, people think about Retirementplanning after retirement. To plan for retired life important thing is financialplan.

To succeed as a financial advisor your focus should be more than just finance, investing, and a retirementplan. With the competition becoming fierce in the growing financial industry, you need an edge to set yourself apart from your competitors. Building a relationship requires effort from the initial interaction.

Without a proper retirement nest egg, those 10 years could be met with a personal financial crisis. Set a Budget (and Stick to It) While seemingly a basic concept in the financialplanning toolbox, a budget can uncover bad spending habits unbeknownst to people. The focus becomes more about preservation than growth.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-Term vs. Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals.

This increase can provide greater financial security during your later years, when healthcare costs might rise. Plan for Healthcare Healthcare is one of the biggest uncertainties in retirementplanning. Consider researching retirement-friendly states that offer tax advantages or lower living costs.

Working with a financial advisor during this process can provide a wide range of benefits, such as: A holistic view of your finances: A financial advisor can analyze your current financial situation, assess your financial goals, and develop a personalized financialplan that fits your unique needs.

This strategy aligns with your financial goals, risktolerance, and timeline, ultimately leading to a more stable and profitable investment journey. Just as a diverse garden thrives, a well-allocated portfolio grows robustly, securing your financial future.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. This may lead to a higher or lower risk profile than initially intended. With a higher income, your risktolerance can increase, and you may be more open to investing in equities.

Then you can choose the options that are best for you when you create your investment portfolio and financialplan. Here's a list of some of the types of investments you'll encounter as you make financial choices: ETFs. Leverage tax-advantaged retirement savings accounts from your employer first.

Saving monthly for retirement can create meaningful assets to help boost any shortfalls. What Is FinancialPlanning? Financialplanning is a process. The process continues in monitoring your progress and adjusting your plan as your goals adjust or the economic fabric they are woven into changes.

Table of contents Why saving for retirement early matters 1. The 401(k) Plan 2. The SEP-IRA (AKA Simplified Employee Pension) Expert tip: Understand your risktolerance How to save for retirement in your 20s when you’re just starting out How much should I contribute to my 401(k) in my 20s? Traditional IRA 3.

What’s tricky about financialplanning is that not every strategy is designed for every person. As an individual or business owner, you have a unique set of circumstances, goals, and risktolerance that are each necessary to consider when creating a successful financialplan. Need a financial advisor?

When you think about financialplanning or wealth management, you may think those services are only needed and meaningful for people who have accumulated monopoly-style buckets of money. What Do Financial Advisors Do? Credit planning. Retirementplanning. Estate planning. By Craig Lemoine, Ph.D.,

You can start small by investing through a Robo-advisor, which automates your investments into a portfolio of exchange-traded funds that are chosen based on factors like your risktolerance, age, and financial goals. It will help you accomplish many things.

Fiduciary vs. Non-Fiduciary Not every financial professional is required to hold a fiduciary standard of care. Financial advisors who charge asset management fees, direct financialplanning fees, hourly fees or retainer fees to a client are structurally investment advisor representatives.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content