This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Over the past decade, a growing number of advisors have expanded into offering comprehensive financialplanning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

While many people approach their financialplanning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. Lets explore several potentially effective financialplanning tools that may help you maximize your impact and meet your philanthropic goals.

In particular, financial advisors who offer ongoing services to clients can focus on 3 key areas that are unique to service-based sales as part of a successful sales strategy.

Amid estimates that nearly 40% of all financial advisors are likely to retire in the next 10 years, the need for a new generation of advisor talent is clear.

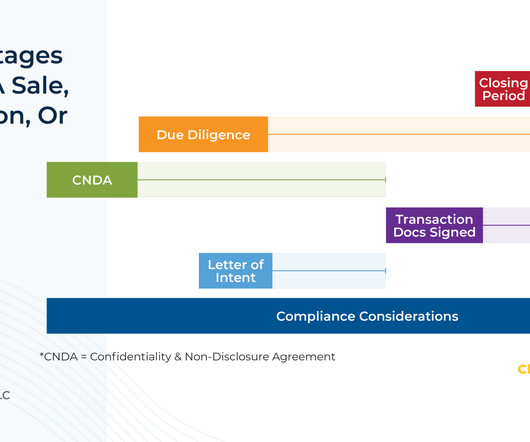

In this guest post, Chris Stanley, investment management attorney and Founding Principal of Beach Street Legal, discusses in depth the various stages of buying, selling, and merging an investment advisory and financialplanning business. Read More.

Welcome back to the 346th episode of the Financial Advisor Success Podcast ! Jim is the founder of MainStreet FinancialPlanning, an hourly, fee-only financialplanning firm, and also created Procrastination Junction, a coaching program for fee-only financial advisors looking to improve their sales skills.

Consulting a financial advisor can help you optimize your retirement plan based on your financial goals. Create Succession and Exit Plans Having a clear succession or exit plan ensures the continuity of your business in the event of retirement, sale, or unforeseen circumstances.

One common sales tactic for financial advisors is to offer prospective clients a free (or low-cost) financialplan to demonstrate the advisor’s expertise and to let the prospect ‘test drive’ the advisor’s services.

There are many financialplanning considerations before, during, and after a divorce. A key part of the process from a financial standpoint is dividing the assets. Here are some key considerations when financialplanning for a divorce. Here’s a checklist of post-divorce financialplanning moves.

What's unique about Brad, though, is how he built a multi-billion-dollar advisory firm not by moving 'upmarket' to gather multi-millionaire clients, but instead leveraged his 401(k) retirement plan advisory firm to begin offering comprehensive financialplanning to the employees of large companies as an added employee benefit, and in the process scaled (..)

Historically, the career path for newer financial advisors has followed a commission-based model that was focused on sales and business development first and learning the technical aspects of financialplanning along the way.

Historically, the career path for newer financial advisors has followed a commission-based model that was focused on sales and business development first and learning the technical aspects of financialplanning along the way.

Many employee advisors gravitate toward service-oriented roles; this preference often stems from their initial motivation for entering the profession – wanting to help clients or perform the more analytical aspects of investing and financialplanning. Rarely do they enter the field to be in a sales or marketing role.

kindnessfp.com) DPL Financial Partners saw a big boost in annuity sales in 2023. financial-planning.com) Why diversity is an advantage for wealth management firms. msn.com) Why follow-up questions are crucial in financialplanning. thinkadvisor.com) Five steps to create a paycheck in retirement.

Income Lab and MoneyTree both launch new ‘One-Page FinancialPlan’ summary reports as advisors continue to demand more tools to demonstrate the ongoing value of financialplanning after the upfront planning process is complete!

For many financial advisors, choosing their profession was based on a genuine desire to help others achieve their financial goals. Yet, while these advisors recognize the importance of business development to grow their firms, they are also very often intimidated by the process of adopting sales techniques to convert leads to clients.

riaintel.com) How to prep an RIA for sale. (fa-mag.com) papers.ssrn.com) Taxes A 2023 year-end tax planning guide. kitces.com) Advisers How the profession of financialplanning has changed over time. (investmentnews.com) M&A The RIA model continues to take share. fa-mag.com) Research into how RIAs grow.

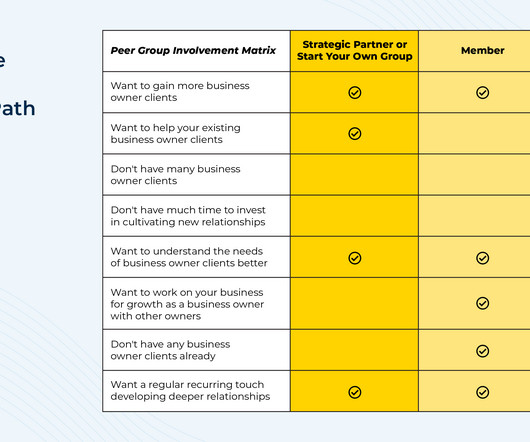

When it comes to focusing on a niche for financial advisors, business owner clients can be an appealing target as they can have complex financialplanning problems ranging from cash flow management to tax planning to acquisition strategies.

What's unique about Bridget, though, is how, as a solo advisor, she found herself overwhelmed with the pressures of having to manage different aspects of her business while also providing great service to her clients as she quickly grew to $77M of AUM in 7 years, and has decided to not to "scale" her firm by hiring more advisors but instead leverage (..)

What's unique about Liz, though, is how she and her brother have taken ownership of what was originally their father’s broad commission-based practice with more than 1,500 clients, and have managed the balance of transitioning the business into a fee-based financialplanning practice while still doing right by the smaller or more transactional (..)

Cold calls, country club memberships, Chamber of Commerce networking, and referrals (from clients or centers of influence) were staples for growth, and determining how successful those sales-centric efforts were was rather straightforward.

As a financial advisor or insurance agent, you must do the work and close the sale. You have learned all about features and benefits during sales training at your firm. Yet, is the best way to close sales to overexplain or list details clients are not interested in or don’t understand?

Deciding how to allocate and invest the proceeds after the sale of your company is a big decision that requires careful planning. If you are expecting a sudden windfall , develop a plan to allocate the proceeds and reinvest in your future. As you weigh what to do with money from the sale of a business, consider these key points.

As Halloween night approaches with its haunted houses, creepy costumes, and ghoulish tales, you might be tempted to join in on the spirit of giving away financialplanning for free. However, before you embrace the idea of giving away your expertise like candy on Halloween night, it's crucial to consider the potential consequences.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the Department of Labor released the final version of its Retirement Security Rule (a.k.a.

Consult with a tax professional to navigate the complexities and avoid wash-sale rules. The post Save on Taxes with These 5 Year-End Financial Tips appeared first on MainStreet FinancialPlanning. You can use up to $3,000 of net capital losses to offset ordinary income, with any excess carried forward to future years.

While focusing on promoting the industry more positively may be a helpful (and much-needed) shift, individual advisors and firms can also work collectively to sell financialplanning by promoting the value of their firms as a whole and not just by showcasing the talent of individual advisors.

Welcome back to the 363rd episode of the Financial Advisor Success Podcast! Christa is the Managing Director of FinancialPlanning and Business Development at Sebold Capital, a fee-only RIA based in Chicago, Illinois, which manages $300M across more than 100 client households. My guest on today's podcast is Christa Madison.

And to complicate things further, when it is decided to go ahead with tax-loss harvesting, there are numerous considerations involved to ensure the strategy is carried out correctly and avoids running afoul of the IRS’s wash sale rules (which could disallow losses and negate the value of the strategy altogether).

Here are six questions to ask when choosing a financial advisor: How do you get paid? Fee-only advisors receive no compensation from the sale of investment or insurance products. Make sure to find someone who offers the types of services and advice that you are seeking. What are your conflicts of interest?

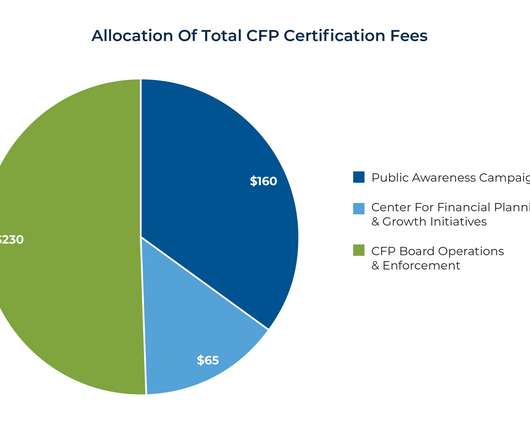

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent survey sponsored by CFP Board demonstrates the upsides of a career in financialplanning, from a median salary of nearly $200,000 to flexible work schedules and a strong sense of purpose among advisors.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that the FPA is planning to leave the FinancialPlanning Coalition (which also includes the CFP Board and NAPFA) at the end of the year.

Also in industry news this week: Large asset managers offering hybrid digital-human advice services are eating into the market share of purely human advisors, signaling that a smaller firm's ability to offer a differentiated value proposition could be a key to success in the coming years A recent study indicates that tech-forward advisory firms not (..)

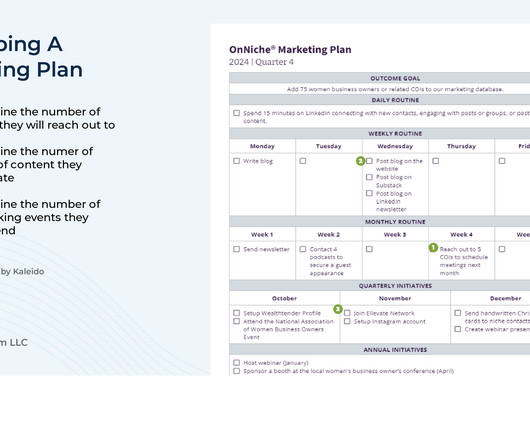

In this article, youll get 10 proven marketing strategies that financial planners should take to grow your business in 2025. Your overall branding, marketing, and salesplan should include website buildouts, product launches, social media calendars, email marketing campaigns , copywriting, SEO, and Meta Ads management.

Historically, staying the course and following a financialplan has outperformed rash investment decisions when there are times of uncertainty in the financial market. But it takes a strong plan—and no small amount of willpower—to do this. When the market is down, Roth conversions are essentially on sale.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that the FinancialPlanning Association and Money.com are planning to publish a “Best Financial Advisors” list based on advisors’ education, credentials, and experience, as well as harder-to-quantify (..)

Assuming that you have a financialplan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risk tolerance. Nobody can predict how long this will last. Do nothing.

However, as the industry evolved from being primarily transaction-based to relationship-based, it has become increasingly important for advicers to become less sales-oriented and more focused on how they can better develop deep, long-term connections with their clients.

There are large parts of the Sell-side that figured out It’s a much cleaner business model to charge a reasonable fee for straight-up asset management and financialplanning, rather than playing the game of stock picking sector rotation market timing and the like. This isn’t really a fair accusation.

In the early days of wealth management, a financial advisor's value proposition was relatively explicit, typically focusing on a limited range of portfolio management activities (e.g., selling and trading) or on sales-oriented advice that centered on implementing insurance products.

At least, if you are a smart investor who does the right things: Set up a financialplan, manage your own behavior, engage in long-term thinking, and avoid reacting to the endless daily noise that markets + media generate. My obvious bias is that my advisory firm charges clients to create financialplans and manage their assets.

From there, the latest highlights also feature a number of other interesting advisor technology announcements, including: Holistiplan, after achieving success with its tax planning and analysis software, has announced an investment from Lead Edge Capital, signaling that it may be ready to expand into other financialplanning areas beyond tax – (..)

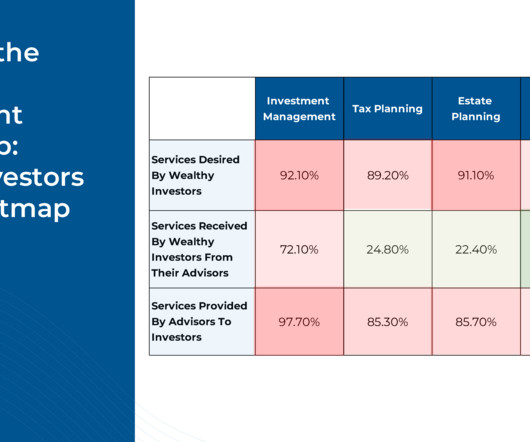

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. Combined with growing advisor (and consumer) interest in comprehensive financialplanning services, the number of ways advisors can add value for their clients has expanded greatly.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content