This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Taxes are a central component of financial planning. Almost every financial planning issue – whether it is retirement, investments, cash flow, insurance, or estate planning – has tax considerations, and advisors provide a great deal of value in helping clients minimize their overall tax burden.

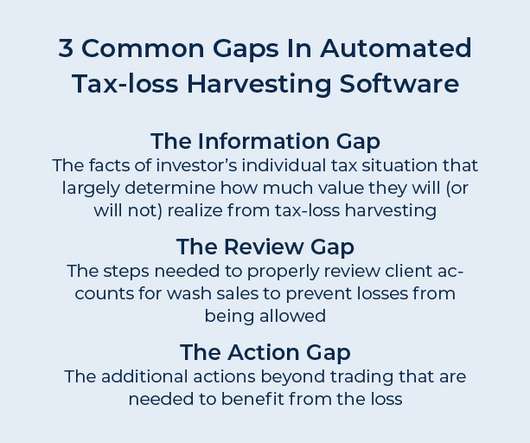

In recent years, numerous software solutions have sprung up that aim to automate the process of tax-loss harvesting. But what the providers of automated tax-loss harvesting often don’t mention is that the actual value of tax-loss harvesting depends highly on an individual’s own tax circumstances.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

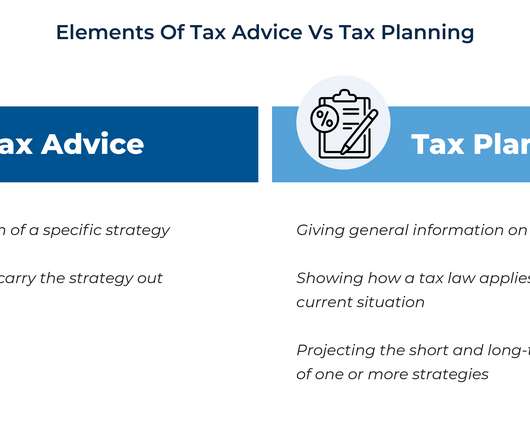

Traditionally, financial advice and tax preparation have existed as 2 related, but separate, services. CPA, EA, or JD) to prepare tax returns and represent clients before the IRS, there has also been the impression that there is simply not enough time for one person to do both.

Tax-loss harvesting – i.e., selling investments at a loss to capture a tax deduction while re-investing the proceeds to maintain market exposure – is a popular strategy for financial advisors to increase their clients’ after-tax investment returns. With these three tools (i.e.,

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

For many small tax firms, the process of collecting client tax documents can be a time-consuming and a prolonged process. The good news is that technology solutions, like Harness, can streamline document collection and transform the way tax professionals work. Client experience is another area where manual processes fall short.

As is traditional, the 2025 IRS tax filing deadline is April 15th. In this guide, well explore the 2025 tax extension process, the reasons for requesting an extension, and how a tax advisor from Harness can help you. Table of Contents What is a tax extension? Why do I need a tax extension? This is not the case.

Freelancers and contractors may enjoy greater flexibility and independence than full-time employees, however, this autonomy brings increased tax responsibility. Unlike W-2 employees, freelancers and independent contractors are responsible for managing their own tax obligations, which can be a complex process.

Financial planning and taxplanning go hand in hand. Including taxplanning as part of your service provides clients a comprehensive view of their finances and helps them achieve their financial goals. Start with Document Sharing The first step is to ask your clients to share their tax documents with you.

Tax advice is a common topic on social media platforms like TikTok. Influencers promise easy ways to secure tax deductions, simplifying complex ideas into bite-sized claims that gloss over important details in the process. Can Hiring Your Children Help You Save on Taxes? Can You Claim Your Pet as a Tax Write-Off?

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. For married couples, this means more of your income will be taxed at lower rates.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

However, unlike stocks and bonds, alternative investments, or alts as theyre commonly known, have unique tax treatments and complex reporting requirements that investors should carefully consider before investing. Well also go into some potential strategies to optimize tax efficiency. How Are Alternative Investments Taxed?

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

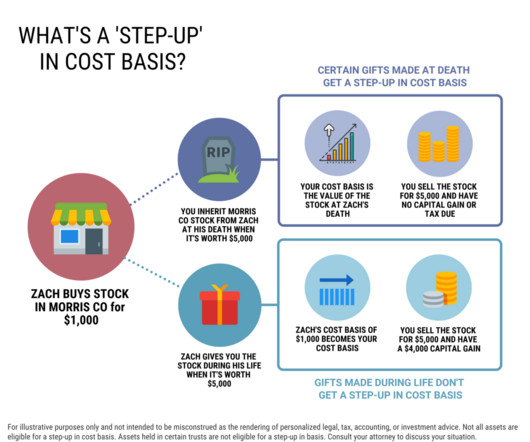

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets. This increases the tax basis, which determines capital gains or losses when the asset is sold.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. In tax lingo, this is known as substantial risk of forfeiture.

This flexibility allows EDBs to extend the tax-deferred growth of the inherited funds over a longer period, which is a huge advantage in strategic taxplanning. By having the option to stretch distributions, EDBs can mitigate the tax impact in any given year and potentially stay in a lower tax bracket.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

When you transfer most assets to a taxable account, there will be income tax, but with company stock, you can take advantage of net unrealized appreciation (NUA). . However, the tax deferral benefit comes at a cost tradeoff. Almost every dollar distributed from a pretax retirement account will be taxed at ordinary income tax rates.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. The first three options are pass-through entities, so profits and losses are distributed to the owners who are taxed on them.

In this episode, we talk in-depth about how, after years of working in an environment where she saw first-hand how ultra-high-net-worth clients keep and grow their wealth (and the lack of diversity among those clients), Kamila decided to build a practice that focused on providing holistic financial planning to communities of color with emerging wealth, (..)

By Mike Valenti, CPA, CFP ® , Director of TaxPlanning It’s that time of year again! W-2s, 1099s and mortgage statements have been to hit your mailbox: a daily reminder that it is, once again, Tax Season. Overall, it was a relatively quiet year on the tax front. Although Congress isn’t done yet! More on that later.)

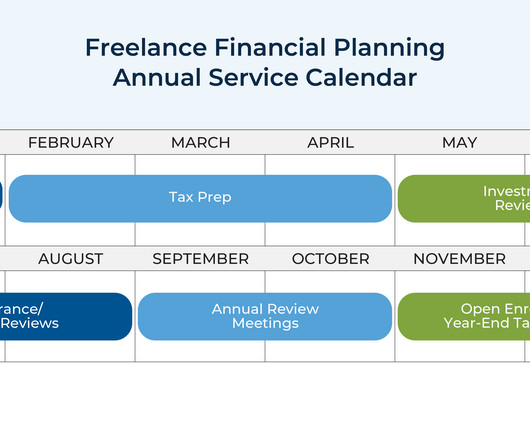

Some advisors implement client service calendars that dedicate certain times of the year to taxplanning, insurance reviews, or quarterly meetings, and fill the gaps with newsletters, client appreciation events, and regular firm updates.

Also in industry news this week: 2 House committees this week advanced legislation that would halt implementation of the Department of Labor's new Retirement Security Rule, which, combined with ongoing lawsuits, threaten to derail the regulation either before or soon after it becomes effective in late September A Federal judge has put the future of (..)

Below are some insights from Richard Morris, Executive Vice President and Director of Tax Services, and Alex Seleznev, Senior Investment Advisor and Chief Operating Officer of MBI, LLC. And depending on your specific tax situation, you may be paying between 15% and 20% or even more in capital gain taxes.

Mike Valenti, CPA, CFP ® , Director of TaxPlanning Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner It’s January, so it’s officially tax season! One of the most common client questions heard by tax preparers is, “So, what do you need from me?” This can result in additional tax owed, plus penalties and interest.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

By Mike Valenti, CPA, CFP ® , Director, TaxPlanning Corporate executives often receive the brunt of the U.S. tax system. Typically, most or all of their income is W-2 income and subject to the higher ordinary tax rates as well as FICA taxes. However, stock compensation, large bonuses, commissions, etc.,

They consider your current financial situation, risk tolerance, and future objectives to help develop a comprehensive plan. This personalized approach can help you make financial decisions that are well-informed and strategically sound. link] Mike Gruidel is a non-producing affiliate of Cetera Advisor Networks, LLC.

Key Takeaways: T ax Season Start: The IRS will likely begin accepting 2024 tax returns between January 15 and 31, 2025. Key Deadlines: The federal tax filing deadline (Tax Day) is April 15, 2025, with an extension deadline of October 15, 2025. Document Deadlines: Most key tax forms (W-2, 1099, etc.)

Tax season is fast approaching, so you may find yourself with some important tax questions. This article will cover some of the pitfalls of this process to make sure that you get the most out of your taxes this year. It’s best to be patient and ensure that you have all the documents that you need for submitting your taxes. [1]

Not only was the stock market fairly volatile, but there were also atypical tax regulation changes. Tax-loss harvesting. Paying taxes on investment gains can be a financial burden, but tax loss harvesting can reduce your bill. You can claim as much capital loss as your realized capital gain plus $3,000.

Using a strategy called tax-loss harvesting, you can earn capital gains tax credits on your investment losses. What is Tax-Loss Harvesting? It’s crucial to know that tax-loss harvesting only defers your capital gains taxes; it does not eliminate them. When is the Right Time for Tax-Loss Harvesting?

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation.

Finally, the annual T3/Inside Information Software Survey, which assesses the software programs used by financial advisors, found that taxplanning tools are on the rise – with adoption rates jumping from 30% to 43%.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

With the new year in full swing, tax season is just around the corner. Filing federal income taxes can be a long and complicated process, and mistakes are bound to happen here and there. As many of us know, these small mistakes can cost you big in tax returns and penalties. Is the Standard Deduction Right for You?

Qualified withdrawals from a 529 plan are tax-free at the federal level, and some states also offer tax breaks to their residents. It’s important to evaluate the federal and state tax consequences of plan withdrawals and contributions before you invest in a 529 plan.

Income shifting (also known as income splitting) may be defined as dividing income in a way that lowers overall taxes. When using these methods to shift income to a child, it’s always important to bear in mind the kiddie tax. Timing the receipt of your income can also help you lower your taxes.

To attract new clients and foster long-term relationships, tax advisors could consider adopting digital marketing strategies. It’s also an important touchpoint to introduce your tax practice’s staff to potential clients, giving you to potential build a personal relationship from the start.

Beneficial Ownership Information (BOI) reporting is part of the Corporate Transparency Act (CTA) and requires millions of business entities to report beneficial ownership information, including data about the individuals who ultimately control a company. Table of Contents What is a BOI Report?

Pass-Through Entity Tax (PTET) is a state-level tax mechanism designed to sidestep the federal State and Local Tax (SALT) deduction limit. Allowing a pass-through entity to pay state income taxes directly, PTET effectively shifts the tax burden from individual owners to the business itself.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content