This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

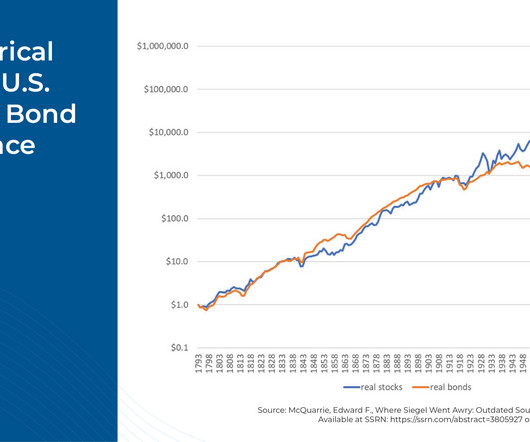

Accordingly, McQuarrie found that, while stocks did indeed far outperform bonds between 1942–1981, not only did stocks and bonds produce about the same wealthaccumulation during the 150-year period before 1942, but the same held true from 1982–2019 as well.

Despite the positive statistics, disparities in income, workplace discrimination, and lower inheritance rates persist, impacting long-term wealthaccumulation. Additionally, financial habits such as lower contributions to retirement plans and reliance on tangible assets pose unique challenges.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirement planning emerges as a valuable strategy. It also minimizes errors and oversights.

[CDATA[ When it comes to managing your finances, it's not just about saving and investing wisely. Tax planning is a crucial aspect of personal finance that often gets overlooked and plays a pivotal role in your overall financial health and wealthaccumulation.

Whether you’re aiming for long-term wealthaccumulation or exploring short-term opportunities, the courses guide you through proper financial planning. Also, you will learn about the factors that influence mutual funds, key elements to know before investing and how investing in mutual funds differs from the stock market.

Consider consulting with a professional financial advisor who can help you understand and employ suitable retirement investment strategies based on your income, age, and retirement expectations. This article explores different ways in which financial advisors can help you with wealthaccumulation for retirement.

2020 Year-End Planning Letter. Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for consideration with their other advisors. There are issues and uncertainties to consider every year when revisiting one’s plans, but 2020 has been a uniquely challenging year on many fronts.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content