This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

(riabiz.com) The biz Goldman Sach's ($GS) future is in wealth management. ft.com) Creative Planning has closed on its purchase of Goldman Sachs' ($GS) PFM unit. citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end taxplanning guide.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

Podcasts Michael Kitces talks divorce planning with Michelle Klisanich who is a Wealth Advisor for Financially Wise Divorce. kitces.com) Matt Zeigler talks with Wade Pfau about managing sequence of returns risk in retirement. kitces.com) Taxes Following the RMD rules for inherited IRAs may not be optimal. forbes.com)

Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. Welcome back to the 297th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Andy Panko. Read More.

Managing the business’s finances is one of the most crucial aspects. Proper financial management can be the difference between a thriving business and one that struggles to stay afloat. Get Help with TaxPlanningTaxplanning is a critical component of financial management.

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

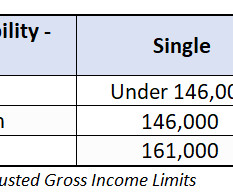

There are income limits for contributions to a traditional IRA that qualify for a tax deduction. The deductibility phase-out is based on filing status, income (MAGI), and whether or not the individual(s) are eligible to participate in a retirementplan at work. Yes and no.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Optimize retirementplan contributions The maximum allowable 401(k) contribution for 2023 is $22,500, with a $7,500 additional contribution, if the plan allows, for taxpayers who are 50 and over.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

Retirement is different for folks who are running a small business. Your retirement is something that isn’t set up by an employer, and you often must manage it on your own. And in some cases, business owners have to manage options on behalf of their employees too.

You cannot sell the securities within the retirementplan, then move cash to a brokerage account and purchase the same shares at that point. While within a taxable brokerage account, both dividends and capital gains generally receive favorable tax treatment. This would negate the NUA benefit.

Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision. Darrow Wealth Management doesn’t provide tax advice; consult your tax advisor to discuss your personal situation. . that could increase the tax due from the surtax.

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

How to Choose the Right Wealth Management Firm in Kansas City Managing your wealth is a crucial aspect of financial success and security. Let’s look at key factors to consider when selecting the ideal wealth management firm in the Kansas City metro area. But with many options available, how do you choose the right one?

Bunching strategies Bunching strategies are taxplanning techniques used to maximize deductions by combining multiple years’ worth of deductible expenses into a single tax year. Planning ahead : Carefully plan stock sales or gifts for dependents to avoid triggering higher tax rates.

Total 401(k) contribution limits: Including employer matches, after-tax contributions, and other contributions, the total limit is $69,000 (or $76,500 for individuals aged 50 and above). The key difference lies in the final destination of the after-tax contributions.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

appeared first on Yardley Wealth Management, LLC. A Guide for Financial Planning When it comes to managing your finances, it’s crucial to work with a professional who puts your interests first. As a result, this plan can help guide your financial decisions and ensure that you’re on track to achieve your goals.

Hiring a wealth manager is one of the biggest financial decisions you’ll make. Hiring a wealth manager is a long-term investment, so it’s important to find someone who will take the time to get to know your goals, values, and long-term goals. Factors to be considered before hiring a wealth manager. .

Wealth management is an important aspect of the financial world that focuses on managing wealth to help individuals and families achieve their financial goals. Wealth management involves a range of financial services as an investment, finance, real estate, tax, and risk management.

would permit employers to make matching contributions to an employee’s 401(k) and 403(b) retirementplan, even if the worker isn’t saving themselves. Keep in mind, matching contributions are often voluntary so it would be up to the plan as to whether to adopt this provision. The Secure Act 2.0 Other Roth changes.

The IRS has released the 2023 contribution limits for retirementplans and other cost-of-living adjustments. The agency also released tax brackets for ordinary income and long-term capital gains. Income Limits for Tax-Deductible IRA Contributions & Roth IRA Contribution Eligibility. Income Tax Rates in 2023.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. No wonder people get nervous when there’s lots of talk about higher taxes, but little certainty on what may come of it, and who it might affect. .

This infographic has more on how a brokerage account is taxed. Taxplanning opportunities in retirement If you only have assets in tax-deferred accounts, you may have fewer taxplanning options in retirement. See 2024 limits to determine whether you’re eligible.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog. appeared first on Darrow Wealth Management.

Once you have your goals set, you can build your plan with any combination of the following elements: Budgeting and expense management: Create a detailed budget outlining income, expenses, and savings targets. Debt management: Develop a strategy to pay off existing debts efficiently, minimizing interest costs.

Roth 401(k)s can only bypass annual distributions if 100% of the retirementplan was in a Roth account. If there’s a mix of pre-tax and Roth funds, RMDs will apply. As a result, taxplanning is critical, particularly if you’ve inherited a large 401(k) or IRA.

Fortune Financial’s specialized approach to managing NUA is an indispensable tool for informed investors. With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirementplanning.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirement accounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. You retire.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . Tax-Planning Possibilities.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. But there are other ways to go about taxplanning. appeared first on Darrow Wealth Management.

Some states also offer tax exemptions for Social Security benefits and other retirement income sources. Assessing the tax structure of your state and constructing your retirementplan and financial strategy around your state’s tax system can help you stay a step ahead in retirement.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

Financial Risk Manager (FRM) – If you love solving problems and wish to help your clients mitigate risks you can turn your attention to a career as a Financial Risk Manager. You can also undertake the globally recognized course in risk management from GARP (Global Association of Risk Professionals).

Freelancers and contractors may enjoy greater flexibility and independence than full-time employees, however, this autonomy brings increased tax responsibility. Unlike W-2 employees, freelancers and independent contractors are responsible for managing their own tax obligations, which can be a complex process.

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Wealth managers and financial advisors offer a wide range of wealth management services designed to help clients achieve their financial goals.

In retirement, how you distribute that company stock will play a key role in determining your tax liability for its value. In the realm of investment and retirementplanning, the concept of Net Unrealized Appreciation (NUA) holds significant importance. The remaining assets may be rolled over.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content