This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The challenge in writing How NOT to Invest was organizing a large number of ideas, many of which were only loosely connected, into something coherent, understandable, and, most importantly, readable. Bad Numbers : 4. We evolved in an arithmetic world, so we are unprepared for the exponential math of finance. It is March 18th!

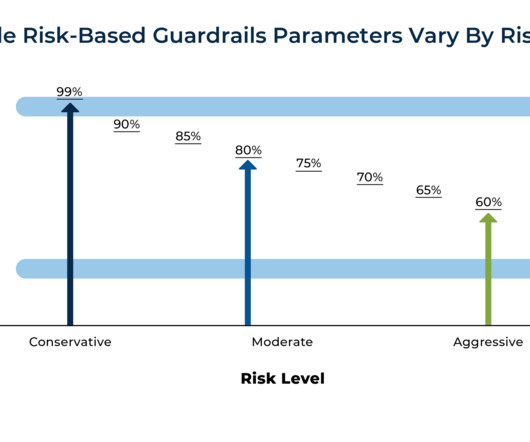

Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives. a guardrails-based strategy that adjusts spending levels if the client's portfolio either exceeds or drops below specified thresholds) that clients can understand, trust, and follow consistently.

At the same time, they also overwhelmingly recognize the value of financial advisors , not only for increasing their wealth beyond what they could have achieved on their own , but also for helping them feel more prepared and less stressed about their finances!

Sherman oversees and administers DoubleLine’s investment management subcommittee; serves as lead portfolio manager for multisector and derivative-based strategies; and is a member of the firm’s executive management and fixed-income asset allocation committees. He is host of the podcast The Sherman Show and a CFA charter holder.

This piece was inspired by this fantastic Josh Brown rant on CNBC about how the 60/40 stock/bond portfolio isn’t dead. The 60/40 stock/bond portfolio is the gold standard of portfolios. Let’s put some numbers to this to explain why. The math on the 40% slice is much cleaner. Give it a watch.

That number is from a Bankrate article I found on a Google search. I'd be curious to hear if anyone else does the same search and finds a different number of lost coins. First, is the math right based on my numbers? The above two portfolios are pretty consistent with a lot of the work we do here.

He co-chairs a number of the asset management investment committees. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998. I ended up being hired onto the high yield desk as a research analyst and did that for a number of years, a couple of years.

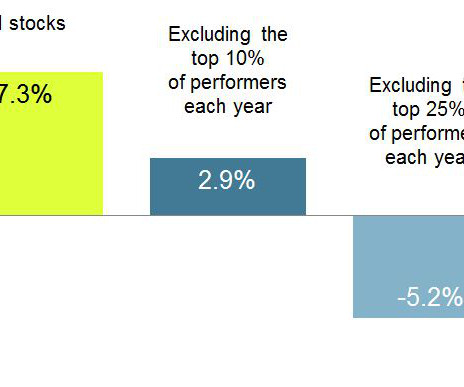

The title tells you the author's conclusion, Why Your Portfolio Should Hold Way More Than 30 Stocks. This article obviously favors more stocks but an interesting thing not said was at what number would it make sense to just flip from individual holdings to mutual funds and ETFs. Not too many I'd say. I've been lucky.

First up was a webinar about model portfolios at ETF.com. The way my new firm is set up, I could outsource everything, for a fee, and the way this was positioned, I think there might be a decent number of advisors who do just that. I think that when investors hear about model portfolios they sort of think in terms of set and forget.

These studies show that, given a choice between an annuity with a monthly income and an investment portfolio structured to provide the same sort of returns over time, if we’re near retirement we choose the annuity seven times out of ten. There’s no shame in admitting that factor – for a lot of us, math can be very tough.

Quarterly statements will be required to include numbers on lifetime income. Make sure your income is coming from a secure source, not the best performing portfolio. Look at the math to understand and believe it. Your 401(k) statements might look a bit different starting next month.

My process here for the notional values was that the multiplier is 100 so a put struck at 4100 would hedge $410,000 worth of stock, so then I just multiplied the dollar amount by the number of puts. Why wouldn't the fund have already blown up earlier this year when the S&P 500 was up more?

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. Businessweek ) but see With cash earning 5%, why risk money on the stock market? With the 10 year at 4.2%

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. That’s exactly right.

But today, data is widely available and it’s a key tool you can use to enhance your portfolio returns. Portfolio management was a lot less evidence-based than it is today. As it turns out, there are ways you can use data to your advantage, even if you’re not a math wizard. market volatility. What’s two plus two.

S&P returns (including dividends) since 2019, graph by the excellent portfolio visualizer website. Which makes the landlord business a lot less profitable, and we should expect exactly the same thing as stock investor: lower future profits as a percentage of our portfolio value. Its just basic math. 4.3% – 5.3%

Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. With more normal scenarios, really crunch the numbers with your accountant. Some goal, your number, is fine to shoot for but whatever you end up with is your reality. They want you to know.

WENGER: No, we’ve definitely always been disciplined on valuation, and we’ve let a number of things go. We have a separate vehicle called the Opportunity Fund, where we sometimes write bigger checks into late-stage rounds in some of our portfolio companies, but not always. And sometimes you’re very happy at that.

I've been saying meaningful yield without too much volatility is what investors hope the bond portion of their portfolio will give. The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. Taking volatility out of a fixed income portfolio is fairly simple.

My 64 and 2 month number is $3049 which is where I get the $1524.50 number for her. If you will pull an income from an investment portfolio, what could go wrong? If that money is in an IRA, that is going to change your math considerably due to having to withdraw all of that inherited IRA within 10 years.

You might have a generic 60/40 portfolio that you expected to cover the rest of your income needs but that possibly needs updating after recent market activity. 3] So, it’s easy math: the less you work, the less you’ll earn. Regardless, Social Security can provide a helping hand with your income.

She has a really fascinating background, very eclectic, a combination of math and law. She has run a number of firms and a number of divisions at large firms and traced a career arc that’s just very unusual compared to the typical person in finance. It is something, math has always come easy to me since a child.

Barron's had a fun article that looked at some ideas from William Bernstein titled The Trick To A Bullet Proof Portfolio? Based on the title, it would seem to be in the neighborhood of creating an all-weather portfolio which we've looked at in several different forms over the course of my full 19 years of blogging.

Here's a quote I saw attributed to Barry Ritholtz: “The Best Portfolio is probably the one which sacrifices a bit of performance, but helps you sleep at night.” Barry's quote reminded me of another influence on how I try to manage client portfolio volatility and why I use alts (yes, that conversation continues). Cannot be done?

The Wall Street Journal had an article about the standard 60/40 portfolio , that is 60% allocated to stocks and 40% allocated to fixed income. My experience is that the typical retired person/couple expects growth in exchange for some volatility from the equity portion of their portfolio, they don't want it from their fixed income sleeve.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics.

Nigl’s bracket finally went bust on game 50 (the third game on the second weekend) when three seed Purdue defeated number two Tennessee, 99-94, in overtime. And about 60 percent of national champions are one of the four number one seeds. A roulette wheel hitting the same number seven times in a row ( one in three billion ).

The Math Behind the Growth Let’s take a step back and think about what it would take for a company like Apple to reach a $10 trillion market cap. A well-diversified portfolio can help protect against the unpredictable nature of the stock market. With a current market cap of $2.8 times its current value.

I wasn’t that typical person that did a number of, you know, internships during the summer, had that …. I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. So derivatives were a part where I was very intimidated. I love statistics.

Your assets include everything from the cash in your bank accounts to the value of your stock portfolios and the market value of anything tangible that you own such as a house or a car. Staying away from debt is also encouraged so you can keep your net worth number positive. It also includes valuables like art or jewelry. Rowe Price.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. Initially I joined to help them manage their equity portfolio. It was the exact same trade. I buy everything.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. And so there was a number of less liquid markets that made for quite wide spreads. And you know, I think ultimately there was a number of opportunities that came out.

As a quick reminder, a 67% allocation to 90/60 generally equates to a 100% allocation to a 60/40 portfolio like you might get from Vanguard Balanced Index Fund (VBAIX). For this post I assembled a less dramatic portfolio more in line with Krom's thinking. and that is the number I will assume. or 110 basis points more than VBAIX.

And it worked out and had multiple job offers coming out of school from a number of different insurance companies. I had a number of relationships that I built up and had another job lined up in New York City. And I had an opportunity to be an underwriter for a few years before I decided to go back to school to get the MBA.

A little more specifically the need for diversified portfolios persists with the implication that bonds are the way to get this done. This chart contributes to the logic supporting a 60/40 portfolio. As a matter of math, it cannot repeat the run from 8.5% Portfolio 2 above has 65% in growth. in November.

Do the bottom up work, it won't take long, to figure out some real numbers. Simple math is that this person needs to save $23/yr to come up with that additional $350,000. That's not a real number of course as you'd expect new contributions to also grow. But simple math tells you that adding $5000/yr likely won't cut it.

Heather comes from with a fascinating background, having previously been in a number of other places, most notably Morningstar, and, and she has a very specific approach to investment management and thinking about stock selection. They do a number of things at Diamond Hill that many other investment shops don’t.

She has had a number of different positions within PIM, including managing their flagship core real estate fund. She has lived and invested through not just the great financial crisis, but the SNL crisis and a number of other fascinating experiences in real estate. If there was an error in a report or a number, I went ballistic.

Hendrik Bessembinder An excellent piece from Bloomberg came out over the weekend, The Math Behind Futility , which looks beyond the usual explanations as to why the majority of professional stock pickers fail to keep up with an index. "Even if there weren’t fees and expenses, the odds are you’ll underperform."

Charles Schwab just released their 2022 RIA Benchmarking Study and I decided to crunch the numbers and see what the data shows. Crunch the Numbers. With a traditional 60/40 allocation, this portfolio would have grown about 75.5% For comparison, a passive 60/40 bond portfolio, as mentioned above, grew at a CAGR of 11.9%.

Run Your Numbers You need to get a handle on your various sources of income and where they are housed — as in, how easily you can access them when you need them. Cleaning up your balance sheet and erasing high-interest debt is essential to avoid putting excess strain on your portfolio. Contact us today.

Maintains a large number of readily-available, interested buyers. Figuring out how to calculate liquid net worth is as simple as doing a quick math equation: Liquid assets - liabilities = liquid net worth. Don't worry—there is an answer to the question, "What is my liquid net worth" that doesn't involve solving math equations.

For the 5 year bull market you could simplistically add 10% per year or 50% total in dividends and for this year 7 or 8% (six months worth) back in which changes the numbers considerably. The nucleus of non-gameover portfolios will always be equities. Yahoo doesn't show total return. Is QYLD any sort of proxy for the NASDAQ 100?

And like I say, that’s part of why it’s translated to a number of people coming to BlackRock and be with me today. RIEDER: So I had known Larry Fink and Rob Caputo, our CEO and president, for a number of years. But you know exactly how they’re going to interplay within a portfolio, hugely powerful.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content