This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As Paul Krugman recently wrote on his excellent Substack , using a chart identical to the one immediately above (Paul used FRED ): “People may imagine that government is a bigger part of the economy than it is because of all the money we spend supporting retired Americans, covering their health bills, and so on [Chart 1].

open.spotify.com) Retirement Nine things to consider in retirement. humbledollar.com) Tony Isola, "Withdrawal rates are more than numbers on a spreadsheet." tonyisola.com) Retirement is, in part, about saying no to obligations you don't like. marketwatch.com) The retirement savings system is still way too complex.

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

financialducksinarow.com) Retirement The math behind savings rates and retiring early. ofdollarsanddata.com) Make sure you know what you are retiring to. dariusforoux.com) Society New car prices are out of the reach of an increasing number of Americans. (techcrunch.com) Medicare Nothing about Medicare is simple.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

My 64 and 2 month number is $3049 which is where I get the $1524.50 number for her. If that money is in an IRA, that is going to change your math considerably due to having to withdraw all of that inherited IRA within 10 years. This whole exercise was bottom up and based on very simple questions.

When taking out your retirement income, it’s important to consider the source. New statements may make it easier to see what you have, but what should you focus on when making a retirement income plan? Quarterly statements will be required to include numbers on lifetime income. Look at the math to understand and believe it.

Some problems are easily solved with a bit of reasoning, logic, or by using a bit of math. The most thought-provoking issues aren’t numbers-based. These issues require much deeper consideration and often cause … Continued The post Wild Retirement Problems, Ep #221 appeared first on Financial Symmetry, Inc.

Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner We’ve all asked ourselves whether it’s too early to retire (usually after a particularly challenging commute or dealing with a difficult client). But even if you feel confident today, would it be reasonable to retire early? How Early Is Early?

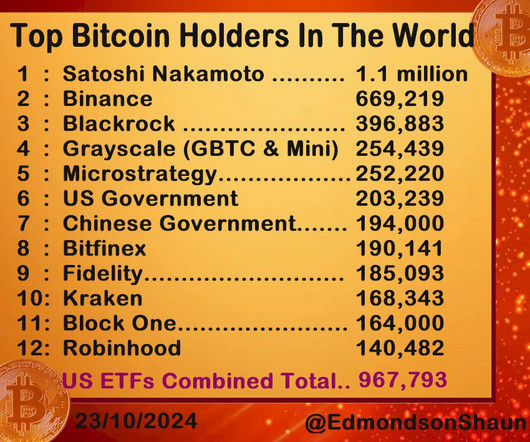

That number is from a Bankrate article I found on a Google search. I'd be curious to hear if anyone else does the same search and finds a different number of lost coins. First, is the math right based on my numbers? That roughly two million Bitcoin is actually more than 10% because approximately 3.8

It has further been estimated that as we approach retirement, this ratio increases to a factor of five times more pain for a loss as opposed to the joy we experience for a gain. There’s no shame in admitting that factor – for a lot of us, math can be very tough.

change at retirement. Hopefully a mortgage is paid off, hopefully there are no car payments to make and health insurance at 65, if retired, should go down quite a bit on Medicare, especially if income goes way down. Once someone is retired, saving for retirement is one less expense too.

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. With more normal scenarios, really crunch the numbers with your accountant.

Yesterday Ben and I did a show on retirement. We basically partnered with them and were fully transparent with the numbers. While the math of the former is easy, and the implementation of the latter takes a stick, even my two smart ass millennial offspring will now admit it created a solid foundation. Don't delay.

If you adjust it for only the working age and retired population then inventory is even higher. Of course, this data is highly localized and we generally measure “inventory” by the number of units that are actually for sale. And that’s where the math on renting comes into play.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers.

Confirm Your Numbers Make sure that your filing status, name, and the names and Social Security numbers of your dependents are accurate. It’s also not a bad idea to review the bank account numbers you included (some of those digits can be lengthy!). 5] Avoid Early Retirement Account Withdrawals if You Can!

This article obviously favors more stocks but an interesting thing not said was at what number would it make sense to just flip from individual holdings to mutual funds and ETFs. In my opinion the diversification benefit hits diminishing returns pretty close to 40 individual holdings based on math if nothing else.

The term personal finance ratios might be giving you flashbacks to math class. In mathematical terms, a ratio is essentially a way to compare two numbers to each other. Since personal finance is all about numbers, that can come in handy in many ways! However, their value tends to fluctuate more so it’s not a stable number).

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. If you’re depending on income to fund your retirement, 5% rates are a blessing. With the 10 year at 4.2%

For most, Social Security provides a solid foundation for retirement income. As you grow older and retirement looms on the horizon, the decisions you make start to have a more crucial impact on the amount of money you receive, so it’s important that you know what to expect.

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. Staying away from debt is also encouraged so you can keep your net worth number positive. The information here is just to guide you, not to set any rules. Rowe Price.

The latest retirement disaster article from Yahoo focuses on 55 year olds who have a "median savings of less than $50,000." Yahoo says it's "bleak" because this cohort is "only about a decade from retiring." A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund.

The term personal finance ratios might give you flashbacks to math class, learning various formulas, equations, and ratios. In mathematical terms, a ratio is essentially a way to compare two numbers. Since finance is all about numbers, that can come in handy in many ways especially when making financial calculations!

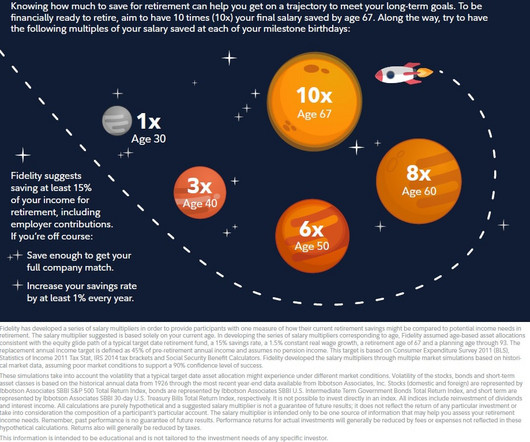

The internet was triggered by these numbers from Fidelity. Ben and I spoke about this concept on a podcast we did about retirement. I thought these numbers were completely ridiculous. I understand all the reasons why it's hard to save money, but in this post I only want to look at the math. 3x your income by 40?

My process here for the notional values was that the multiplier is 100 so a put struck at 4100 would hedge $410,000 worth of stock, so then I just multiplied the dollar amount by the number of puts. Why wouldn't the fund have already blown up earlier this year when the S&P 500 was up more?

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? Its just basic math.

He co-chairs a number of the asset management investment committees. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998. I ended up being hired onto the high yield desk as a research analyst and did that for a number of years, a couple of years.

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. The only pension I am remotely close to is the Arizona Public Safety Personnel Retirement System. The concept of pensions is that they provide a security net to retired workers. Is he right? Is he wrong?

The numbers in the 60/30/10 each represent a percentage of your financial plan. With this system, you will use 60% of your take-home pay to build your savings or even an early retirement account , invest, save up for a down payment, or repay debt. As an example, one of my major savings goals is retirement.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. And so there was a number of less liquid markets that made for quite wide spreads. And you know, I think ultimately there was a number of opportunities that came out.

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. That just isn't the reality. The diversification benefits of intermediate and longer term bonds is not what it used to be. Taking volatility out of a fixed income portfolio is fairly simple.

This meant that there was very little demand for debt and so increasing the supply of potential loans was like an apple cart salesman increasing the number of apples he sells with the hope that more supply would create its own demand. This is the basic math behind what’s happened to every consumer who owns these bonds.

Bloomberg had an article titled As Gen-X Nears Retirement, Many Fear They Can't Afford It-Now or Ever. There was an odd and I believe inaccurate emphasis on workplace retirement plans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Then $27,750 is the magic number. Let’s do math again! What Does $30 an Hour Translate to in Terms of Paycheck?

My experience is that the typical retired person/couple expects growth in exchange for some volatility from the equity portion of their portfolio, they don't want it from their fixed income sleeve. I'm not sure how much fixed income that has equity beta should be in a portfolio but I don't think it's a high number.

She has a really fascinating background, very eclectic, a combination of math and law. She has run a number of firms and a number of divisions at large firms and traced a career arc that’s just very unusual compared to the typical person in finance. It is something, math has always come easy to me since a child.

A quick excerpt from a post a couple of weeks ago about retirement misconceptions. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal. Part of the math that determines options premiums is the risk free rate of return from T-bills.

CFP Board certificant data makes one thing clear: “the issue of the low number of women CFP® professionals is primarily a problem of attraction, and not one of retention. women tend to live longer, making it much more important to plan for a longer retirement) or a subjective one (e.g. Whether it’s an objective topic (e.g.,

And don't worry if math isn't your thing because we've included 50 30 20 budget spreadsheet ideas to help you stay on top of your budgeting strategies. It can include investing in the stock market, purchasing real estate, or also setting up your retirement accounts. Beyond that, focus on your retirement savings.

There was a lot of content from various places over the weekend about whether it is time to go back into bonds, what retired investors should do for yield and even whether retirees are better off going 100% into equities. As a matter of math, it cannot repeat the run from 8.5% Barron's also noted that 60/40 was up 9.6% in November.

Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. We all need an emergency fund, and to save more long-term (think: retirement). Don’t put it into a retirement account where you won’t be able to get the money out for years.) Consider some of these ways to save.

That is difficult to pull off but if you do the math on that it shows long term outperformance. He makes a good point about not relying solely on math to assess markets and portfolio construction, that the psychology of markets is important too. 75/50 seeks to capture 75% of the upside with only 50% of the downside.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content