This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. That emotional connection supports confidence and increases the likelihood that the client will stick with their plan and stay committed through both good markets and bad.

(wiredplanning.com) Christine Benz and Jeff Ptak talk retirement income with Kelli Hueler, CEO and founder of Hueler Companies. citywire.com) Creative Planning is getting creative to retain former United Capital advisers. riaintel.com) Selling a service, like financial planning, is different than selling a product.

riabiz.com) Creative Planning is exploring its custody options. investmentnews.com) Research The problematic math of passing down generational wealth. blogs.cfainstitute.org) How life events affect retirementplanning. investmentecosystem.com) Reflections on eight years of running a financial planning practice.

(nytimes.com) Retirement The sweet spot in retirement: working because you want to. contessacapitaladvisors.com) How to navigate retirement child-free. vox.com) Retirement savings The math behind tcontributing to your 401(k) plan. rationalwalk.com) How to fix 401(k) plans for the modern workforce.

When planning for retirement, it’s effectively impossible to precisely forecast the performance and timing of future investment returns, which in turn makes it challenging to accurately predict a plan’s success or failure.

humbledollar.com) Why planning in retirement is so challenging. humbledollar.com) Doing the math on a hybrid vs. conventional ICE. (downtownjoshbrown.com) What's driving stock market returns? awealthofcommonsense.com) 11 financial mistakes to avoid including 'Not carrying umbrella coverage.'

(youtube.com) Christine Benz and Amy Arnott talk with Peter Mallouk, President and CEO of Creative Planning, about the 'messy' business of financial advice. podcasts.apple.com) Jordan Haynes talks with Justin Castelli about the important role of life planning. thinkadvisor.com) Not everyone is happier in retirement.

whitecoatinvestor.com) RetirementRetirement is filled with all sort of irreversible decisions. nytimes.com) How time feels more precious in retirement. advisorpedia.com) Retirement accounts Just because you can contribute to an IRA doesn't mean you should. humbledollar.com) Don't be ashamed to take senior discounts.

apexmoney.com) Retirement Lessons from a 'faux retirement' including 'Balance is hard!' morningstar.com) On the math of early Social Security claiming. Why you need a plan. (humbledollar.com) An appreciation of Jonathan Clements' work. bestinterest.blog) Cognitive decline is coming for us all.

awealthofcommonsense.com) Home buying math is bad right now, but will it be any better a year from now? bloomberg.com) Personal finance Things to do before pulling the plug on your job and retiring. humbledollar.com) Financial planning means always adjusting your plan. finance.yahoo.com) The case for semi-retirement.

financialducksinarow.com) Retirement The math behind savings rates and retiring early. ofdollarsanddata.com) Make sure you know what you are retiring to. obliviousinvestor.com) How to effectively withdraw money from a 529 plan. wsj.com) When building an estate plan, hire an attorney who specializes in it.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

I understand the difficulty of that one but if you're 50, overweight and taking a half dozen medications, you should plan on health stuff being very expensive. I've said many times that I plan to wait until 70 and that I think my wife should take hers at the same time which would be 64 and 2 months. number for her.

(theirrelevantinvestor.com) Peter Lazaroff talks with Jesse Cramer about the math behind car ownership. peterlazaroff.com) Retirement How retirement can open you up to new possibilities. humbledollar.com) Some tips on how to boost your spending in retirement. barrons.com) When it doesn't make sense to move in retirement.

When taking out your retirement income, it’s important to consider the source. New statements may make it easier to see what you have, but what should you focus on when making a retirement income plan? Having an income plan is key for your retirementplanning. Look at the math to understand and believe it.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

Scott Brennan The difficult part of retirement for a lot of successful people isn’t about the money; it’s about the perceived loss of importance. Some of these relationships are with people who want to retire or who are already retired. Math has no emotion, but people do. It’s a blow to their ego.

Morgan Housel Finance types tend to focus on attributes like intelligence, math skills and computer programming. You can know everything about math and data and markets, but if you don’t control your sense of greed and fear and you’re managing uncertainty in your behavior, none of it matters. None of it matters.

Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner We’ve all asked ourselves whether it’s too early to retire (usually after a particularly challenging commute or dealing with a difficult client). But even if you feel confident today, would it be reasonable to retire early? How Early Is Early?

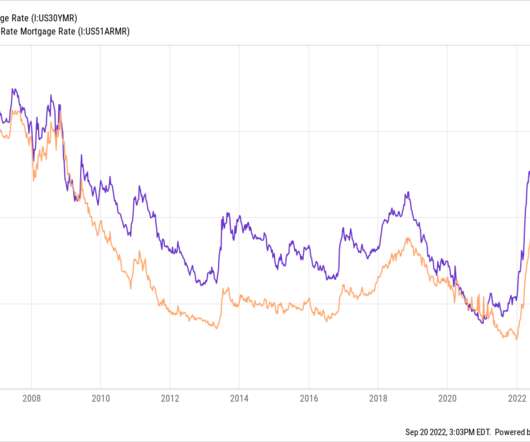

Is retiring with a mortgage a good idea? Retiring with a mortgage doesn’t typically pose a financial risk, and at times it’s the best financial decision. But paying off a mortgage before retirement has upsides also. Here’s when it may – and may not – make sense to pay off a mortgage before retiring.

By Pouring Billions Into Public Housing : One quarter of residents in the French capital live in government-owned housing, part of an aggressive plan to keep lower-income Parisians — and their businesses — in the city. [link] • How Does Paris Stay Paris? Hope came cheap enough, but I was also realistic. Here’s a gentle primer.

Yahoo warned of potential problems retirees may face if their plan is to rely solely on Social Security. change at retirement. Hopefully a mortgage is paid off, hopefully there are no car payments to make and health insurance at 65, if retired, should go down quite a bit on Medicare, especially if income goes way down.

Yahoo Finance had kind of a long read recapping an update from Morningstar about safe retirement withdrawal rates. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal. Part of the math that determines options premiums is the risk free rate of return from T-bills.

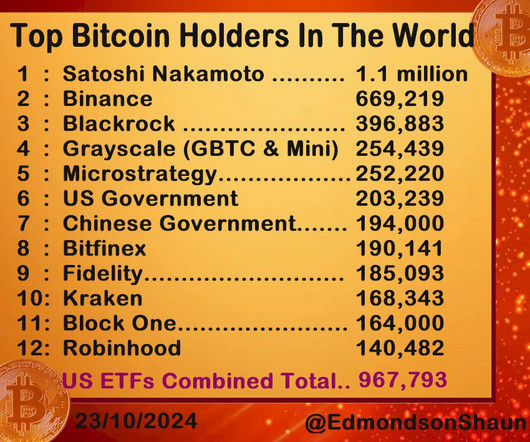

First, is the math right based on my numbers? I think I can stick to my plan of not selling until it grows into a life changing piece of money but we'll see. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

The importance of getting women into financial planning feels like it should go without saying. Alicia’s Experience One of my earliest experiences when I first decided to get into financial planning was participating in the Financial Planning Association’s Externship Program in the summer of 2020.

It has further been estimated that as we approach retirement, this ratio increases to a factor of five times more pain for a loss as opposed to the joy we experience for a gain. There’s no shame in admitting that factor – for a lot of us, math can be very tough.

Maybe it’s due to employee stock option plans. And the way math works, you end up with a stock that goes up a bunch. And you’re going to see a big sea change in the next three to five years of asset managers and RIAs optimizing taxable tax, and then non-taxable retirement accounts for various type of investments.

Yesterday Ben and I did a show on retirement. How to think about it, how to plan for it, and everything in-between. Saving for college We put all of our kids through college with a fairly simple, but rigorous plan. We should have a sense of urgency about retirement because it's coming, and there are no do overs.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers.

And I think you will also, if you are at all curious about estate planning or investing or personal finance, this is not the usual discussion and I think it’s very worthwhile for you to hear this and share it with friends and family. What was your original career plan? So I made a plan to get out of there.

For most, Social Security provides a solid foundation for retirement income. As you grow older and retirement looms on the horizon, the decisions you make start to have a more crucial impact on the amount of money you receive, so it’s important that you know what to expect.

Next, let’s face it, not all of us are exceptional when it comes to math. Taxpayers should always confirm that their math is correct, as this is one of the most common mistakes made when filing. [1] 5] Avoid Early Retirement Account Withdrawals if You Can! 6] Double-Check!

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. How much are you likely to end up with in your retirement accounts?

We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. I looked at the Vanguard Target Retirement 2025 (VTTVX) and the Vanguard Target Retirement 2030 (VTHRX).

The latest retirement disaster article from Yahoo focuses on 55 year olds who have a "median savings of less than $50,000." Yahoo says it's "bleak" because this cohort is "only about a decade from retiring." A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund.

Do the math of your raise. Some quick math will reveal exactly how much extra income you’ll be working with in your monthly budget. The trap of short-term gratification in the form of luxury convenience can delay your plans to get out of debt, save for a down payment, or retire. Is it an essential item?

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. You will likely want to retire in the next decade, so it's important to save and invest as much as possible while also not being too risky. Rowe Price.

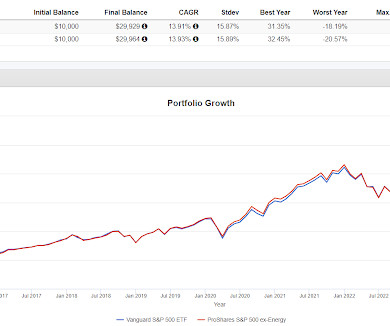

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. YSPY sells put spreads on a 3x fund. Oddly, the fund page no longer mentioned targeting a 2x outcome, it appears to now say 3x.

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. About 40 years ago employers started to pivot away from pensions to 401k, they started to pivot away from defined benefit plans to defined contribution plans. Problems have been long in the making and seem to have gotten worse.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

We all know we should save more of our money to prepare for coming events, so learning how to make a savings plan is essential. That said, a weekly or bi-weekly savings plan can help you reach goals. A weekly savings plan or bi-weekly savings plan (saving every two weeks) helps you break down your goals. every two weeks.

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. From a legacy planning standpoint, two distinctions are especially important: Roth IRAs do not require their owners or spouses to take mandatory distributions.

The Long Game: Roth Conversions & Legacy Planning. Legacy planning is all about transferring wealth to descendants as efficiently as possible. So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Background.

The term personal finance ratios might be giving you flashbacks to math class. You can use ratios to keep track of many different aspects of your financial situation—from cash flow to savings to retirement and more. Money stored in retirement accounts also is illiquid, since withdrawals are subject to lots of rules and take time.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content