This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Economic Innumeracy : Some individuals experience math anxiety, but it only takes a bit of insight to navigate the many ways numbers can mislead us. We evolved in an arithmetic world, so we are unprepared for the exponential math of finance. Cognitive Deficits : You’re human unfortunately, that hurts your portfolio.

Would you like to diversify but also defer paying big capital gains taxes? But suddenly they find themselves sitting on an uncomfortably large percentage of their portfolio in a single name. And the way math works, you end up with a stock that goes up a bunch. It gets to be a bigger, bigger percentage of your portfolio.

Home ownership How to make the math behind home ownership work (or not). awealthofcommonsense.com) How Morgan Housel invests his portfolio. etf.com) Taxes It's time, once again, to start thinking about how to shrink an estate. humbledollar.com) How to calculated the real, after-tax returns on cash.

Podcasts Barry Ritholtz talks with Liz Ann Sonders about how to rebalance your portfolio. awealthofcommonsense.com) On the math of a 0% line of credit. wsj.com) How do estimated taxes work? ritholtz.com) Jesse Cramer talks with Peter Lazaroff about how to hang in there for the long run. abnormalreturns.com) FOMO is real.

“I need the US Dollar to be a store of value between the time I make it until I spend it, invest it, pay my taxes with it, or give it away. To be more precise, I want to discuss the type of chart that reflects a fundamental misunderstanding of the nature of money, currency, spending, investing, and taxes. and paying taxes.

At the same time, they also overwhelmingly recognize the value of financial advisors , not only for increasing their wealth beyond what they could have achieved on their own , but also for helping them feel more prepared and less stressed about their finances!

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. 24, 2023 _ 1: In particular, why average outperforms over the long run; Sommers credits not making errors (via Charlie Ellis’ “Winning the Loser’s Game”) but the nuance and math are fascinating.

First, is the math right based on my numbers? I think it can be a productive portfolio addition betting on the asymmetry which of course argues for starting very small. The above two portfolios are pretty consistent with a lot of the work we do here. How can it solve anyone's problem?

A portfolio that goes narrower than an S&P 500 500 or total market fund probably has some exposure to low vol, dividends and the others. And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out.

First up was a webinar about model portfolios at ETF.com. Outsourcing the work related to actually being an advisor would not feel right to me and I enjoy what I get to do including portfolio construction. I think that when investors hear about model portfolios they sort of think in terms of set and forget.

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. In a 60/40 portfolio, a 30% weighting to SSO would in theory equal a 60% weight to equities, opening the door to some sort of of capital efficient portfolio even if that just meant sitting in cash.

CR: Tariffs are taxes. Anon: But tariffs can replace the income tax. from the income tax and the US imports $3T of goods. We’d have to tax ~85% of imports to cover that, but that would also reduce imports so it’s unrealistic and the basic math doesn’t come close to working. CR: The govt makes $2.5T

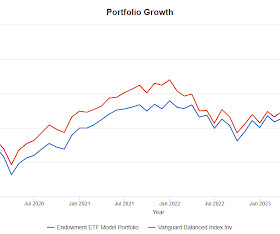

If any of us had constructed this portfolio and implemented it for ourselves, it would have been a very acceptable result. The portfolio did just fine, it captured most of the upside and avoided the full brunt in 2022's large decline. One thing lacking from the "Endowment ETF Model Portfolio" is any hint of endowment-like results.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

So how do you then go from tax and audit practice to finance and investing? So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. Very different fields.

Avoiding long duration bonds was a big theme to my writing (and portfolio construction) for a long time, still is, but then the thought evolved to where I started saying that long duration fixed income has a source of unreliable volatility that makes it very difficult to model it in to a portfolio with any confidence.

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. That’s exactly right.

When a portfolio is down significantly, you’ll need to cash out more shares to arrive at the same amount of income, and it can be tough to recover from the loss of those assets. Cleaning up your balance sheet and erasing high-interest debt is essential to avoid putting excess strain on your portfolio.

Part of the equation is that he is convinced that tax rates have to go up to pay for out debt and so converting to a Roth now before tax rates do go up will result in people ending up with more after tax dollars versus just going the RMD route at what is now 73 on its way to 75. How much can you take from your portfolio?

I've been saying meaningful yield without too much volatility is what investors hope the bond portion of their portfolio will give. The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. Taking volatility out of a fixed income portfolio is fairly simple.

. $6300 in today's dollars goes a long way for us, that's quite a bit more than our fixed monthly expenses but might be about equal to regular monthly expenses plus once or twice a year type expenses like property tax, home owners insurance and so on. If you will pull an income from an investment portfolio, what could go wrong?

On the flip side, not having a mortgage in retirement can be beneficial if it reduces overall lifestyle costs and how much you’ll need to draw from your portfolio in retirement. However, if the goal is to pay off a mortgage before retirement to spend would-be mortgage payments on other things during retirement, the math may not work out.

This blog has pretty much evolved into 100 ways to build a portfolio without bonds. The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. If the Fed itself can’t forecast rates, why would your financial advisers think they can?"

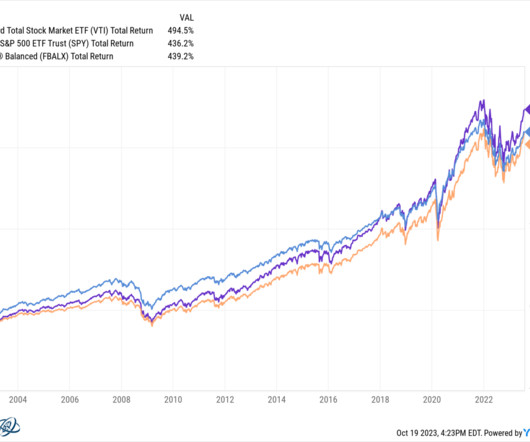

S&P returns (including dividends) since 2019, graph by the excellent portfolio visualizer website. Which makes the landlord business a lot less profitable, and we should expect exactly the same thing as stock investor: lower future profits as a percentage of our portfolio value. Its just basic math.

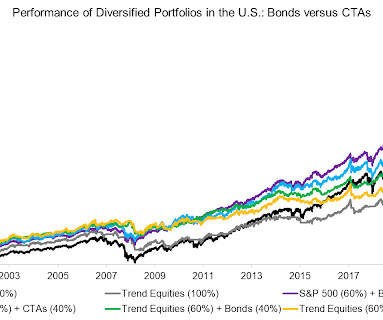

Simple math, it looks like the carry index has compounded at less than 3%. If you use the fund in the manner that I think they intend, a blow up for the stocks and managed futures ETF would be a setback for a portfolio but not a catastrophe. The red line for T-bills is price only. And why do you think you need the leverage?

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. Initially I joined to help them manage their equity portfolio. It was the exact same trade.

We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. In the period available to study SPXE, there has been no difference in returns, volatility or portfolio stats.

I don't see the diversification benefit which as an ongoing theme forces us to think differently about how to build a 60/40 portfolio. It is important to understand the math though. No portfolio concept can always be best. Any valid idea you come up with for your portfolio will lag at times. That's a year to date chart.

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. there’s a big focus on how do we optimize for tax efficiency, too. It’s different wealth regimes, it’s different tax regimes. RITHOLTZ: Applied Mathematics, Quants, those guys, yeah.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing. ADMATI: Yes.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

We regularly look at capital efficiency and its potential uses in portfolio construction. Consider the following two portfolios. In terms of risk weighting or volatility weighting, a smaller allocation to semiconductors could deliver the same benefit to a portfolio as a larger weighting to broad tech.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics.

These items for us include things like propane delivery (we could pay monthly), property tax and so on. Simple math is that this person needs to save $23/yr to come up with that additional $350,000. But simple math tells you that adding $5000/yr likely won't cut it. BTW, I mean that literally, it is all on a spreadsheet.

That is correct, technically but whatever you're looking for from REITs, or private equity or any of the others, you're not going to see it impact the portfolio as part of an index fund. Mistakes during those types of events are what managing portfolios is all about.

You wouldn’t be surprised to learn the tax consequences of owning a mutual fund is a part of it. If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Really fascinating guy.

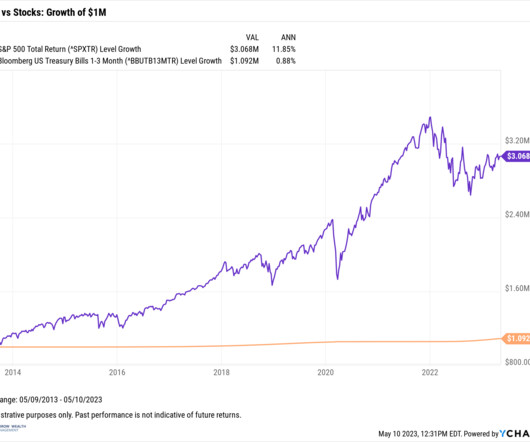

Again just using simple math, this presumes the par value will roll over each month and reinvest at the same rate to get to the annual yield. Cash vs stocks: growth of $1M With an average annualized return under 1%, the cash portfolio only gains $92,000 over a decade. Compare that to the stated yield of 5.6% 467% a month.

If you dig even deeper, you may also think about tax implications, including the alternative minimum tax and qualified holding periods. But the basics of equity compensation and tax aside, theres something else you might want to be mindful of something that is a bit more difficult to define or quantify.

We try to remind them that rising rates, despite their inevitable short-term effect on fixed-rate bond prices, do not necessarily mean long-term declines for bond portfolios generally or for municipal bond portfolios specifically. MUNICIPALS AND RISING RATES Simple math dictates that when yields rise, fixed-rate bond prices fall.

We try to remind them that rising rates, despite their inevitable short-term effect on fixed-rate bond prices, do not necessarily mean long-term declines for bond portfolios generally or for municipal bond portfolios specifically. Simple math dictates that when yields rise, fixed-rate bond prices fall.

Your assets include everything from the cash in your bank accounts to the value of your stock portfolios and the market value of anything tangible that you own such as a house or a car. Any medical debt, personal loans, or back taxes are also considered liabilities. Subtract your liabilities from your assets to get your net worth.

Indeed, a Roth conversion has the potential to generate greater wealth than a traditional IRA during an individual’s or couple’s lifetime, and it can play a meaningful role in providing tax advantages to heirs throughout their lifetime as well. RMDs from a traditional IRA are taxed as ordinary income.

Indeed, a Roth conversion has the potential to generate greater wealth than a traditional IRA during an individual’s or couple’s lifetime, and it can play a meaningful role in providing tax advantages to heirs throughout their lifetime as well. RMDs from a traditional IRA are taxed as ordinary income.

If at the start of the year, someone put 100% into the Vanguard Balanced Index Fund (VBAIX) as a proxy for a 60/40 portfolio, then to employ a portable alpha strategy, they could use leverage to add something to hopefully make it additive to returns. So adding a potential alpha source on top of beta (the basic building blocks).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content