This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

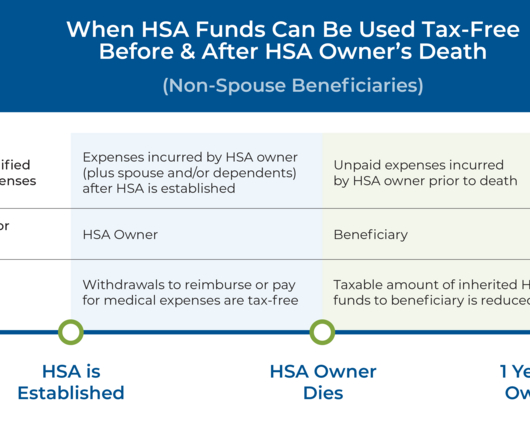

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. An HSA can serve as an additional retirement savings vehicle on top of your IRA or 401(k) to help cover healthcare and other retirement expenses. How the HSA works .

In this episode, we talk in-depth about how Travis originally developed his specialization of student loan planning through first correcting the misinformation given to his (now-)wife and her friends in the medical field (and realized that he could give high value to a chronically underserved population), how Travis first started his student loan consulting (..)

Retiring abroad can be a dream come true for many Americans, offering the opportunity to explore new cultures, enjoy different climates, and potentially stretch retirement savings. Taxes One of the biggest financial considerations for Americans retiring abroad is understanding how taxes will work. tax return every year.

Although numerous tax-advantaged vehicles are available for retirement savings, Health Savings Accounts (HSAs) have particular benefits for individuals saving for retirement. This can allow individuals to save a significant amount that can be withdrawn tax-free for medical expenses later in retirement. Read More.

One such strategy is to advise clients to keep track of any qualified medical expenses they incur after establishing the HSA – even those that are paid for from funds outside the HSA.

Maximize Your Retirement Contributions: Enhancing your retirement savings not only secures your future but also offers immediate tax benefits. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

District Court this week ruled that Missouri's rules that targeted investment advice based on factors other than return maximization was unconstitutional and preempted by Federal law, striking a blow against state efforts to regulate the activities of SEC-registered advisers From there, we have several articles on retirement: 7 factors that can help (..)

Also in industry news this week: Large asset managers offering hybrid digital-human advice services are eating into the market share of purely human advisors, signaling that a smaller firm's ability to offer a differentiated value proposition could be a key to success in the coming years A recent study indicates that tech-forward advisory firms not (..)

It goes by many different names: semi-retirement, partial or phased retirement, second career, and so on. But typically, it means the same thing: working in some capacity after retiring early. As more workers consider the growing appeal of semi-retirement, some ask — is working part-time in retirement a good idea?

An even tougher one, if you have medical issues, how expensive are they likely to be? I understand the difficulty of that one but if you're 50, overweight and taking a half dozen medications, you should plan on health stuff being very expensive. Everything going wrong would be really bad luck.

It’s chock full of great charts and analyses, covering everything from Income, Employment, Expenses, Banking and Credit, Housing, Student Loans, Retirement and Investments, and Overall Financial Well-Being. Curious that medical expenses are the biggest driver of bankruptcy in the United States but not in other wealthy Democracies.

We speak daily with clients who are contemplating where they might live in retirement. Now is the time to explore various retirement housing options and strategies for aging individuals. From aging in place to retirement communities, consider your individual preferences and needs when choosing the most suitable housing option.

Retirement planning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirement planning is even more important. That means you should plan for your retirement savings to last at least 18 years, if not more.

Unlike short-term medical treatments, long-term care focuses on helping people with activities of daily living (ADLs) such as bathing, dressing, eating, using the restroom and mobility. Nursing homes: For individuals who require ongoing medical care and assistance with most ADLs, nursing homes offer 24/7 skilled nursing care.

Many workers have been dreaming of retirement since they first entered the workforce. However, once this retirement date draws near, the prospect of giving up your primary source of income may be nerve-wracking, even if you’ve diligently saved and planned. Draft a Retirement Budget. Rolling Your Savings Over.

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Within this framework, the concept of the five pillars of retirement planning emerges as a valuable strategy. Without a solid plan, you risk drifting without direction.

Northwestern Mutual published a report about the state of retirement and of course all the numbers are grim. million to retire, up about 50% from 2020, while the average retirement account balance is $88,000. I've been pushing back on the idea of have a number, a retirement number, for a very long time.

When putting away for retirement, we often dream about all the things we’ll be able to do with that money – traveling, going out to eat, maybe trying new hobbies. . Of course, there are always the everyday household expenses to account for in your post-retirement budget. Ways to Start Planning Early for Retirement Health Care Costs.

theatlantic.com) Retirement communities are going solar. statnews.com) How GLP-1 drugs could affect medical technology companies. (semafor.com) Costs are rising for offshore wind power projects. ft.com) Solar China is building a lot of solar, but also a lot of new coal plants. nytimes.com) How to stop wasting cheap (solar) energy.

One way of thinking about retirement is that it happens in phases. Phase 1: Pre-retirement (Approximately Ages 50-62) This is around the age when you will start to have a sense of what you have saved and what your expenses might look like. When you are 20 years old, it can be hard to picture what retirement might look like for you.

If you are headed toward retirement soon, or you have just retired, you may find yourself wondering, “Is my nest egg enough?” As you know, medical expenses, long-term care, housing repairs, and other unpredictable costs are just a part of life, so how can you prepare for those kinds of things during your retirement?

Coverage: Health insurance plans typically cover a range of medical services, including doctor visits, hospitalizations, prescription medications, and preventive care. [2] 1-2, 4-6] [link] [3] [link] The post Healthcare in Retirement: The Basics appeared first on Integrity Financial Planning, Inc.

Retirement is an exciting milestone—a time to leave behind the hustle and bustle of work and embrace a new chapter filled with more freedom and opportunities to enjoy life. Planning well in advance ensures that your retirement years will be financially secure, fulfilling, and less stressful than your working years.

Your favorite tax expert Bill Sweet joined me on the show again this week to discuss questions about downshifting your risk as you approach retirement, the most tax-efficient way to pay for a medical procedure, when DIY investors should consider an advisor, the Rule of 55 and how to prepare for taxes in retirement.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirement plans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

However, it is a common goal for retirees to create and maintain generational wealth in retirement. Prior to your retirement years, diversifying your investment portfolio can be a good way to grow your wealth. In today’s fast-paced world, ensuring financial stability for future generations can be a daunting task.

However, choosing the right Medicare plan is crucial to ensure that you have the coverage you need as you move into retirement. Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services. Consider your medical history and any ongoing conditions.

In an earlier post, I summarized many of the housing options people can consider in retirement. This post takes a deeper dive into CCRCs (Continuing Care Retirement Communities also known as Life Plan Communities) CCRCs are an all-in-one solution to aging in place for people over 60. You can check out the article here.

Retirement planning can be a bit complex. Given the complexity and magnitude of things necessary for a comfortable retirement, starting planning from a young age is also essential. At the age of 30, your daily expenses can significantly differ from what you would need in retirement. Ten retirement expenses to keep in mind: 1.

1 With ever-increasing life expectancies, it’s no wonder 63% of American adults say they’re more afraid of running out of money in retirement than they are of death. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement. What Is Longevity Risk?

Yahoo wrote about the biggest regrets that people had about retiring. Sprinkled in there of course were some grim average and median retirement account balances. Maybe people should focus less on hitting their retirement number versus hitting a workable number. Retiring with too much debt was on the list.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Individual Retirement Accounts (IRAs): Contribute up to $7,000 for 2024 ($8,000 if aged 50+). For the majority of people, however, April 15th will remain the deadline. Available to taxpayers aged 70.5

On the other hand, Childfree clients often have an increased need for disability coverage, as they might not have a support system to carry them through their retirement. For instance, Childfree clients, especially those who are single, may have less need for life insurance than couples with dependent children.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! How do I start putting money away for retirement?

A Health Savings Account (HSA) is a special type of savings account that allows individuals with a high-deductible health plan (HDHP) to save money pre-tax for future medical expenses. The funds can be used for qualifying medical costs like doctor visits, prescription medications, dental care, and vision services.

Barron's has a bunch of articles on retirement in this week's issues. The article contends that people have talked themselves into "wanting" to work longer because of how low retirement balances are. The article contends that people have talked themselves into "wanting" to work longer because of how low retirement balances are.

Writing for Bloomberg, Allison Schrager suggests that in order to enjoy retirement, we should work a little longer. Ann Tergesen at the Wall Street Journal reports that while most people expect to retire at 65, 62 ends up being more like it. I haven't even mentioned coming up short in retirement savings. Summing up Schrager.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

A couple of interesting retirement planning items from my reading today. First are two articles about people's reluctance to start to spend down their retirement savings from Kitces and Morningstar , it is a difficult psychological pivot to go from accumulating to decumulating. Something like that probably won't be plan altering.

axios.com) A look at Scottish fund manager Baillie Gifford after the retirement of key manager James Anderson. newsletter.abnormalreturns.com) Mixed media RIP Medical Debt is wiping out billions of dollars of unpaid medical debt. (hollywoodreporter.com) Which is maybe why, streaming customer churn is on the rise.

Keeping up with Medicare changes and making sure that you are prepared for medical expenses is a key part of retirement planning. So, it’s important to keep that in mind as you set up your retirement budget and plan. Unfortunately, exact medical costs are hard to estimate.

Saving money is an important task at any age, but as you hit your 40s, the need to save for retirement grows. While savers in their 40s and 50s typically have a decade or two left to save for retirement given the traditional age of 65, emphasizing saving now can set you up for a dream-worthy retirement.

If you meet someone and tell them you’re a financial advisor who works with medical professionals to help them avoid taxes in retirement, you’re engaging in direct marketing. You’re talking about your brand to someone who doesn’t know it.

The Retirement Manifesto Blog had a post about the "5 Top Regrets of Retirees." Retiring with too much debt? If you have a lot of consumer debt, and assuming no sort of horrible medical event you're paying for, then sorry, you're living beyond your means. The first regret was not saving enough money.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content