This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

Theyre established to benefit charitable organizations, including educational or cultural institutions, community organizations, service organizations such as hospitals, and other nonprofits. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan.

While most of us think of making donations to nonprofits in cash, there are other advantageous ways to support an organization. While it’s always a good time to be generous, there are some years you might find it even more beneficial to achieve a tax deduction. Donate valuable assets that aren’t cash.

If you want to donate a certain amount to charity over a period of time, a donor-advised fund allows you to take the entire donation as a tax deduction in the first year, but then contribute to the charity over time. The charity just needs to be a registered nonprofit. Additionally, the funds in the account can grow tax-free.

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation. Governance risk.

This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. Under the new law, non-spouse beneficiaries (with few exceptions) must now withdraw the entirety of an inherited IRA within 10 years of the account owner's passing rather than over their own lifetimes.

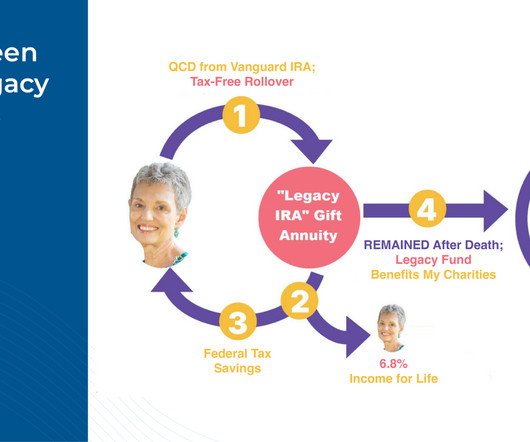

In this guest post, Kathleen Rehl, a semi-retired financial advisor and educator now focusing on her own estate planning considerations, shares her experience with creating her "Legacy IRA" rollover to a Charitable Gift Annuity to support her chosen nonprofits after Congress passed the SECURE 2.0 legislation at the end of 2022.

And it got to the point where there was the potential to do this nonprofit, like charitable bet. It’s part of their own taxplanning. RITHOLTZ: By the way, I just picture this as a sort of a civil war soldier writing home, dearest Martha, I am considering, like in the 2000s, you guys were sending letters back and forth.

Higher Capital Gains Tax Rate: Long-term gains from collectibles are taxed at 28%, higher than the maximum 20% rate for stocks and real estate. Charitable Donations: Donating collectibles to a qualified nonprofit can provide tax deductions based on fair market value. This article is a product of Harness Tax LLC.

Once you have a sturdy foundation, you can more confidently build a plan for retirement and a legacy for your loved ones that aligns with your goals. Be Stubborn about Finding Additional Opportunities Financial planning doesnt need to rely entirely on income. Income taxplanning strategies can play an important role.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content