This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What's unique about Pete, though, is how he has grown his firm by exploring with clients how they can align their portfolios with their own personal values, effectively allowing their investments to become an expression of the types of businesses they want their capital to support… while still ensuring their overall portfolio is still well-diversified, (..)

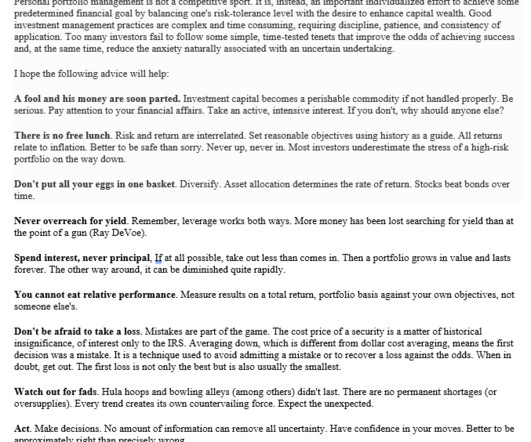

He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Zeikel famously shared his investing insights in a 1994 letter to his daughter: “Personal portfolio management is not a competitive sport. Most investors underestimate the stress of a high-riskportfolio on the way down.

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

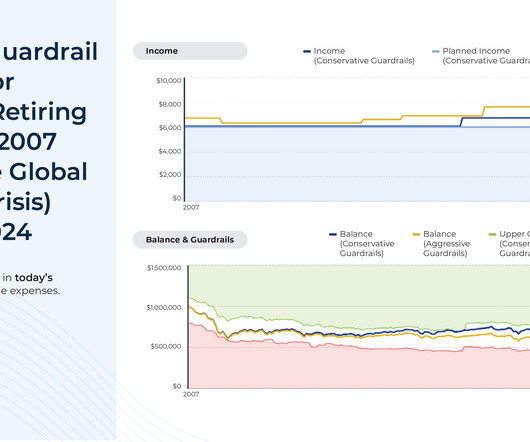

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

step when onboarding a new client, as making any sort of recommendation is impossible without first understanding how comfortable clients may be when their portfolios inevitably experience volatility. Read More.

Seeing your portfolio fluctuate can trigger an emotional response, and the instinct may be to make immediate changes. Rather than reacting to short-term volatility, now is a great time to take a step back and review your investment portfolio. Does it reflect your risktolerance and financial plan?

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. a client who really wanted to guard against downward-spending-adjustment-risk might forgo income increases entirely).

Which means that when an advisor recommends a certain investment strategy for a client, their standards of care should dictate that they first make sure that the strategy is within the client's tolerance for risk.

Our Portfolio Manager, Chad NeSmith, CFA, CFP was recently quoted in an Associated Press article discussing how retirees are reacting to the market volatility spurred by the latest tariff announcements. The overall theme that were really getting at is you really have to be aware of your risktolerance and your financial plan, Chad shared.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing.

Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. By dividing your investments into these three buckets, you help create a clear plan for how and when your money will be used. What Is Bucketing?

One study found that an advisor-managed portfolio could produce an additional 3% value add annually over a self-managed (DIY) portfolio. They consider your current financial situation, risktolerance, and future objectives to help develop a comprehensive plan. Lets explore a few of these.

Portfolio income is the money you make from an investment account, and there are several ways to earn it. We’ll also go over the benefits of growing the income for your portfolio and how to deal with taxes from investments! What is portfolio income? Portfolio income is income earned from investment accounts.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. Bond Basics: How Bonds Work and Reasons to Add Bonds to Your Portfolio Stock vs bond historical returns by calendar year Investors dont hold bonds to outperform stocks over the long run.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

When talking about retirement financial planning, we often take investment strategy at face value. But no matter if you’re considering wealth growth or income generation, your investment decisions will involve calculations around your risktolerance and unique goals as well. What is an Income-Generation Investment Strategy?

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

Your investing strategy is a personal approach based on your goals, life stage and risktolerance. Active investing involves a hands-on approach to managing your portfolio. The fees and time commitment are low, and your portfolio is diversified to weather the ups and downs of the market. What is active investing?

If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. You’ll receive the same $40,000 in dividend income and the value of your portfolio drops to $1.5M. Dividend paying stocks and funds can be a great addition to a portfolio.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. View all accounts as part of a total portfolio.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Clients should not get discouraged by their portfolio’s past performance.

As you work toward your financial goals, regularly reviewing your investment portfolio is essential. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

This is the time to review your portfolio allocation and rebalance if needed. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. Financial Planning is vital. Manage your portfolio with an eye towards downside risk.

It’s really important from a financial well-being point of view for people to have their own individual authentic goals hopefully baked into some form of a financial plan. Brian Portnoy : Investing outside of a well-defined financial plan is speculation. It was just more for the sake of more.

Category: Clients Risk. When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. That requires investing.

No one cares about your financial well-being more than you, so it's important to have a financial plan for yourself. Knowing how to make a financial plan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. What is a financial plan?

A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Since single stocks don’t move like the broader market, you’re exposed to much greater risk. Unfortunately, most executives and insiders have less flexibility to reduce risk on a concentrated position of company stock.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement.

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. But their support does not end there.

Historically, staying the course and following a financial plan has outperformed rash investment decisions when there are times of uncertainty in the financial market. But it takes a strong plan—and no small amount of willpower—to do this. People have strong reactions to any loss. Some clients are better at handling this than others.

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan.

1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. If you are younger, you may be able to take more risks because you have a longer time horizon to earn back potential gains and receive more income in the future.

Does your plan properly account for inflation, now and in the future? Let’s talk about the things you need to be thinking about right now in your financial plan. What is the inflation rate that Brian factors into financial plans? What is the inflation rate that Brian factors into financial plans?

No one cares more about your financial well-being than you, so having a personal financial plan is important. Knowing how to make a financial plan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financial plan?

One area that often gets overlooked in the midst of planning is reviewing your financial habits and goals, so I’ve put together a short list of 3 areas to review before January. If you are unsure if your portfolio aligns with your risktolerance, time horizon and goals, reach out to us at Mainstreet and we would be happy to help!

For one person, that might mean reassessing their risktolerance and portfolio holdings to make sure that they hold assets that will at least sustain their value or provide a safer return, such as an interest rate or a dividend yield. What Can We Expect from the Markets? Why Meet with a Financial Advisor?

There are many options, but your top priority should be choosing an investment that aligns well with your goals and risktolerance. Open a 529 College Savings Plan. Open a 529 College Savings Plan. Low minimum investment – $10 Diversified real estate portfolioPortfolio Transparency. Invest in ETFs.

This is where diversifying your investment portfolio comes into play. Diversifying your investment portfolio is a vital strategy for managing risk, optimizing returns, and achieving your financial goals. However, diversifying your investment portfolio can help reduce your overall investment risk.

Investment management companies – firms that provide individual portfolio management and may work with other investment companies. For example, do you want to make investment decisions or let the experts do it through a managed portfolio? Managed investment options through Charles Schwab Intelligent Portfolios.

When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term asset allocation strategy to manage its endowment assets. Step two is developing capital market assumptions against which to model portfolios with different mixes of asset classes. RISK AND RETURN.

When investing in a 401(k), one of the most important decisions you can make is how often to rebalance your portfolio. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. This article will explore how often to rebalance your 401(k). Need a financial advisor?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content